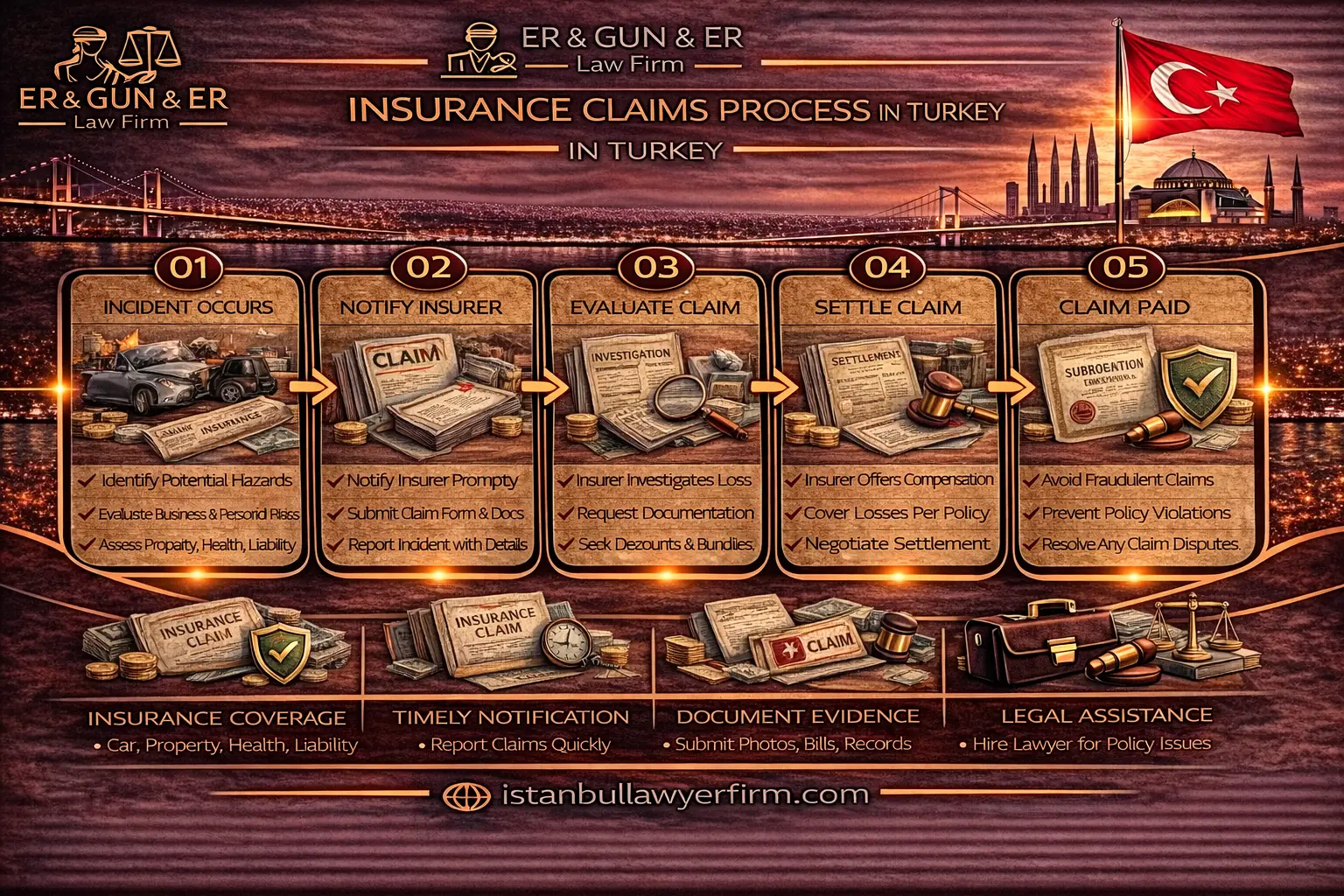

A lawyer in Turkey who advises on insurance claims understands that the insurance claims process in Turkey is a structured sequence where outcomes depend less on dramatic arguments and more on whether the file shows timely steps, consistent facts, and the correct policy wording—and that most claim disputes arise not from legal complexity but from documentation gaps whose consequences only become clear when the insurer issues its decision. An Istanbul Law Firm that advises on insurance claims process Turkey management provides the integrated guidance covering every stage of this process: identifying the applicable policy and conducting coverage analysis against the issued wording rather than broker summaries; giving timely and documented notice in the format specified by the policy; preserving evidence before repairs begin and establishing chain-of-custody for all collected materials; assembling the document bundle as an indexed evidence pack rather than scattered attachments; managing the adjuster inspection and any expert involvement as formal evidentiary events; satisfying cooperation obligations while avoiding avoidable admissions; responding to reservation of rights letters with indexed document bundles; building defenses against denial reasons through element-by-element analysis; negotiating settlement on documented terms whose payment mechanics are clearly specified; and managing escalation through complaints, interim measures, and litigation where necessary. A Turkish Law Firm that advises on claims handling Turkey insurance matters understands that the most important strategic insight in insurance claims is treating each communication as a potential exhibit—because the adjuster's report, the insurer's decision memo, and the insured's notice letter will all be read and compared in any later dispute, and inconsistencies between them are often more damaging than the underlying loss. An English speaking lawyer in Turkey who advises on insurance claims for cross-border policyholders provides the bilingual coordination that keeps the notice narrative, evidence pack, and correspondence consistent across languages and time zones. Practice may vary by authority and year — verify current Turkish insurance procedural requirements, current cooperation obligations, and current dispute resolution mechanisms with qualified counsel before taking any action in a Turkish insurance claim, since insurance claim procedures and timelines are applied through regulatory and judicial practice whose current applicable versions determine the specific requirements for each line of insurance and each insurer.

Insurance Claims Process Turkey: Overview, Policy Identification and Coverage Mapping

A lawyer in Turkey who advises on the insurance claims process overview explains that a claim file in Turkey starts the moment the insured reports a loss—and that the first internal record whose creation date, content, and delivery channel will later be examined by adjusters and courts should capture the policy identifier, the loss date, the notice channel, and the person making the report with enough specificity to anchor every later step in the claim chronology. An Istanbul Law Firm that advises on claims process management for corporate and individual policyholders helps clients implement the specific process approach most effective for each claim profile: creating a parallel personal claim file with copies of every communication sent and received—emails with full headers, portal screenshots with timestamps, courier receipts, and same-day call notes; appointing one internal spokesperson who controls the factual wording used in every channel so that the insurer does not receive inconsistent descriptions of the loss from different employees; and separating compassionate customer service language from factual legal statements about causation and extent so that informal reassurances do not create coverage admissions. Turkish lawyers advising on claims process governance help policyholders understand that the most persuasive claims files are those that show a verifiable chain from notice to decision—where every statement is tied to an exhibit and every delivery is evidenced by a traceable confirmation—and that the effort invested in building this chain at the beginning of the claim is consistently smaller than the effort required to reconstruct a coherent record under dispute conditions. Practice may vary by authority and year.

An Istanbul Law Firm that advises on policy identification and coverage mapping for insurance claims explains that coverage analysis begins with locating the final issued policy—not a broker summary, not a renewal email, and not a draft—and comparing the insuring clause, conditions, exclusions, and endorsements against the facts of the specific loss on the specific loss date. Turkish lawyers advising on policy coverage analysis Turkey help claimants implement the specific mapping approach most effective for each coverage situation: confirming that the schedule and wording delivered for the relevant policy period are the version being analyzed; confirming that the insured entity name matches trade registry records so entity mismatch cannot become a coverage defense; mapping each element of the insuring clause—the insured event, the insured interest, the insured asset—to the available evidence; and identifying any conditions precedent whose satisfaction must be proven through contemporaneous records rather than post-incident statements. An English speaking lawyer in Turkey who advises on coverage mapping for cross-border policyholders provides the bilingual analysis that ensures non-Turkish-speaking management understands which policy clauses are decisive, which documentary evidence must be preserved for each clause element, and what the practical consequences are of each coverage position before the first adjuster interaction takes place. Practice may vary by authority and year.

A Turkish Law Firm that advises on the integration between coverage analysis and claims strategy explains that understanding the coverage map before the first insurer meeting consistently produces better outcomes than discovering coverage issues during investigation—because a well-framed coverage analysis identifies what evidence to preserve, what documents to request, and what facts to present in the chronological order that matches the insuring clause rather than the narrative order that feels natural to the insured. An English speaking lawyer in Turkey who advises on coverage-led claims strategy for corporate and international policyholders implements the specific claims approach most effective for each line of insurance: treating every claim notification as a legal document rather than a customer service call; ensuring that all fact statements about the loss match the policy's defined trigger language; treating the document bundle as an evidence pack whose structure mirrors the coverage analysis; and coordinating coverage map updates as new facts emerge during the investigation so that the strategy reflects the current factual record rather than the original assumptions. Practice may vary by authority and year.

Notification, First Steps and Immediate Evidence Preservation

A lawyer in Turkey who advises on insurance claim notification Turkey requirements explains that the notification stage is where many claims are won or lost—because the first recorded version of events defines the factual baseline against which all later adjuster reports, expert opinions, and court pleadings will be measured, and because late or informal notice without written follow-up is one of the most common factual triggers behind coverage denials. An Istanbul Law Firm that advises on notice management for insurance claims helps policyholders implement the specific notification approach most effective for each claim type: giving written notice immediately after stabilizing safety and preventing further damage, identifying the date, location, type of loss, and policy number without speculative causation labels that may later prove inaccurate; requesting a written acknowledgment from the insurer that includes a claim reference number; and confirming the preferred channel for future document delivery so that every subsequent submission can be evidenced by a traceable delivery record. Turkish lawyers advising on insurance claim notification Turkey practice help policyholders understand that phone notice without written follow-up leaves the record incomplete—and that sending a written notice even after a phone call, attaching available photographs and noting who received the oral notification, converts an informal report into a traceable legal event whose date, content, and delivery can all be independently confirmed. Practice may vary by authority and year.

An Istanbul Law Firm that advises on immediate evidence preservation for insurance claims explains that the moment a loss occurs, the insured should treat the scene and all associated data sources as evidence that will be evaluated by adjusters and courts—and that evidence lost before preservation is requested cannot be reconstructed, making immediate action the most important single step in protecting both coverage entitlement and future recovery options. Turkish lawyers advising on evidence preservation insurance claim Turkey discipline help policyholders implement the specific preservation approach most effective for each loss type: photographing the scene before repairs begin with wide shots and close-ups that include visible timestamps and location references; exporting CCTV footage for the relevant time window promptly using the standard system export function and documenting who performed the export; preserving maintenance records, service logs, and ownership documents that will be requested in almost every insurance claim regardless of the line; and creating an evidence index from day one that lists each item, its date, and who collected it. An English speaking lawyer in Turkey who advises on evidence preservation for cross-border policyholders provides the systematic management that creates a chain-of-custody record for all collected materials—ensuring that later challenges to evidence integrity can be addressed by objective documentation rather than memory—and coordinates the evidence index with the notice narrative so that all factual assertions in the claim are tied to a specific preserved item. Practice may vary by authority and year.

A Turkish Law Firm that advises on first-week claim management explains that the first week after a loss is when the insured's internal teams create the documents that will later be examined as the most contemporaneous evidence of what happened—and that internal emails, incident reports, and vendor communications written before the facts are stable often become contradictions that the insurer cites in its decision memo. An English speaking lawyer in Turkey who advises on first-week claim governance for corporate policyholders implements the specific internal discipline most effective for each organization type: requiring all incident communications to separate observed facts from hypotheses; using a consistent factual template across every site report and vendor brief so that local descriptions do not diverge from the central notice narrative; and preserving financial records, operational logs, and contractor documentation from the first day so that quantum and causation evidence is established before the insurer's investigation begins. Practice may vary by authority and year — verify current notification requirements, current evidence standards, and current cooperation expectations applicable to the specific policy with qualified counsel before taking any action.

Document Strategy, Adjuster Workflow and Expert Evidence Management

A lawyer in Turkey who advises on insurance claim document strategy explains that a document strategy is the core of insurance claim documents Turkey discipline—and that the most effective approach is to begin building the evidence pack before the first document request arrives, because the structure of the pack demonstrates cooperation discipline and prevents the insurer from framing a simple evidential gap as non-cooperation. An Istanbul Law Firm that advises on document strategy for insurance claims helps policyholders implement the specific documentation approach most effective for each coverage line: delivering documents through one traceable channel with a cover letter that repeats the claim reference number and lists every attachment in order; using consistent file names across every delivery so the insurer's file matches the insured's index; requesting written acknowledgment of receipt from the insurer for each delivery; and maintaining a single evidence index throughout the claim whose tab structure mirrors the coverage elements—insured event, insured interest, causation, quantum, mitigation—so that later dispute proceedings can be prepared from the same index without rebuilding the document set. Turkish lawyers advising on document management help policyholders understand that indexed delivery discipline distinguishes routine payment files from contested files in claims handling Turkey insurance because clean files can be processed without iterative back-and-forth—and that the cover letter and exhibit index sent with each document bundle become primary evidence in any later cooperation dispute. Practice may vary by authority and year.

An Istanbul Law Firm that advises on adjuster and expert management for insurance claims explains that adjusters and experts translate the narrative loss into facts that can be matched to the policy wording—and that treating the adjuster inspection as a formal evidentiary event rather than an informal site visit is the approach that consistently produces better inspection records whose accuracy can be relied upon in later proceedings. Turkish lawyers advising on adjuster management help policyholders implement the specific approach most effective for each inspection situation: confirming the adjuster identity, mandate, and contact details in writing before the inspection; keeping a written log during the inspection of what was inspected, what samples were taken, and what documents were requested; requesting that factual errors in the adjuster's preliminary findings be corrected in writing and storing the correction request as a dated exhibit; and after the inspection, requesting a written list of outstanding documents and confirming the delivery method so that later allegations of incomplete cooperation have a specific answer. An English speaking lawyer in Turkey who advises on adjuster and expert coordination for cross-border claims provides the bilingual management that ensures non-Turkish-speaking corporate managers understand what the adjuster has inspected, what findings have been recorded, and what specific evidence gaps remain outstanding so that follow-up document delivery can be targeted precisely. Practice may vary by authority and year.

A Turkish Law Firm that advises on independent expert engagement for insurance claims explains that expert involvement becomes important when causation or quantum requires technical methodology that cannot be established through documentary evidence alone—and that commissioning an independent expert with a narrowly defined mandate whose questions are tied directly to the applicable policy conditions consistently produces more useful expert evidence than a broad mandate that invites a full re-investigation. An English speaking lawyer in Turkey who advises on expert evidence management for complex insurance claims implements the specific expert approach most effective for each technical dispute: defining the expert mandate in terms of specific policy elements; asking the expert to document inspection method, materials reviewed, and the limits of the conclusions to avoid overstatement; preserving the expert's raw data including photographs, measurements, and samples; and ensuring that expert conclusions address the specific coverage elements rather than addressing broader technical questions whose answers do not determine coverage outcomes. Practice may vary by authority and year.

Cooperation Duties, Reservation of Rights and Mitigation Obligations

A lawyer in Turkey who advises on cooperation duties in insurance claims explains that cooperation clauses require the insured to provide reasonable assistance—and that the practical management of cooperation obligations is about responding to every insurer request in writing, confirming delivery, and maintaining a request-and-response log whose completeness can later rebut allegations that the insured was non-cooperative. An Istanbul Law Firm that advises on cooperation clause management helps policyholders implement the specific cooperation approach most effective for each claim situation: requiring that each insurer request be tied to a concrete coverage question before committing to unlimited disclosure; providing requested documents through a controlled indexed channel rather than by informal means; requesting confirmation from the insurer when a document set is complete so that later allegations of incomplete production have a specific answer; and centralizing all cooperation responses through one contact person so that different employees do not create parallel narratives. Turkish lawyers advising on cooperation management help policyholders understand that over-cooperation—providing undirected masses of internal documents without indexing—can be as damaging as non-cooperation because it creates contradictions and allows the insurer to cite internal speculation as if it were established fact, and that scoping each delivery to the specific question the insurer has asked is more protective than volunteering documents whose relevance is not explained. Practice may vary by authority and year.

An Istanbul Law Firm that advises on reservation of rights letters for insurance claims explains that a reservation of rights letter is the insurer's formal notice that it will investigate while keeping coverage defenses open—and that the insured's response to this letter frequently determines whether the claim resolves by negotiation or progresses to formal dispute. Turkish lawyers advising on reservation letter responses help policyholders implement the specific response approach most effective for each coverage situation: responding in writing, confirming receipt, and asking the insurer to clarify any requests that are ambiguous; providing documents in indexed bundles rather than scattered attachments; correcting any factual errors in the letter's description of events promptly and requesting that the correction be appended to the claim file; and treating the letter as a trigger for litigation-readiness preparation—freezing internal emails and preserving all evidence in its current state. An English speaking lawyer in Turkey who advises on reservation letter responses for cross-border policyholders provides the bilingual document response management that ensures the insurer's specific coverage questions are answered with exhibits rather than with narrative explanations whose translation can introduce inconsistencies. Practice may vary by authority and year.

A Turkish Law Firm that advises on mitigation and salvage obligations for insurance claims explains that mitigation is the practical duty to take reasonable documented steps to prevent the loss from worsening—and that mitigation records become decisive when the insurer later questions whether costs were reasonable or whether the insured's actions impaired its ability to investigate. An English speaking lawyer in Turkey who advises on mitigation documentation for insurance claims implements the specific mitigation approach most effective for each loss type: taking before-and-after photographs of every mitigation step; keeping invoices and receipts for emergency work with records of who authorized the work and why authorization was urgent; retaining damaged parts and preserving a salvage log with condition photographs; and documenting any instance where the insurer's delayed inspection required the insured to proceed with mitigation before inspection was complete. Practice may vary by authority and year — verify current cooperation, reservation of rights, and mitigation standards applicable to the specific policy line with qualified counsel before taking any action.

Denial Reasons, Defense Strategy and Settlement Negotiation

A lawyer in Turkey who advises on claim denial defense explains that denials in Turkish insurance claims typically follow a predictable set of themes—late or defective notice, non-disclosure at underwriting, exclusion application, breach of cooperation or mitigation conditions, disputed causation through expert report, disputed quantum through valuation methodology objections, or fraud suspicion—and that structuring the defense as a checklist of elements whose satisfaction is proven by specific exhibits consistently produces more effective results than a broad argument about fairness or commercial expectation. An Istanbul Law Firm that advises on claim denial insurance Turkey defense helps policyholders implement the specific defense approach most effective for each denial ground: requesting the written denial letter that states the factual basis and the specific policy terms relied upon; if the insurer denies for late notice, producing the first notice record and the claim number acknowledgment to anchor timing; if the insurer relies on an exclusion, mapping the exclusion element by element and showing which element is not satisfied on the preserved facts; and if the insurer relies on a technical report about causation, obtaining the raw data basis and challenging methodology rather than motives. Turkish lawyers advising on denial defense help policyholders understand that the most common reason denials are not successfully challenged is that the insured has not preserved the evidence that rebuts the denial's specific factual premise—making evidence preservation the foundational preparation for every denial defense—and that building an indexed rebuttal pack whose structure mirrors the denial letter's own element-by-element presentation is consistently more effective than a general refutation. Practice may vary by authority and year.

An Istanbul Law Firm that advises on insurance settlement negotiation Turkey explains that settlement should be approached as a controlled valuation exercise rather than as a concession of weakness—and that the most effective settlement negotiations are those where the insured has frozen its factual chronology, organized its exhibit index, and quantified the claim with transparent calculations before exchanging numbers. Turkish lawyers advising on settlement negotiation help policyholders implement the specific negotiation approach most effective for each coverage dispute: identifying which claim elements are genuinely disputed and which are provable immediately; supporting any proposed settlement amount with invoices, quotations, and a transparent calculation worksheet; requesting that any insurer counter-proposal include the data basis whose documentation allows the gap between positions to be narrowed on evidence rather than on pressure; and ensuring that settlement documents specify payment channel, currency, invoice form, and what rights are released—with release language drafted narrowly so that unrelated claims against third parties are not accidentally extinguished. An English speaking lawyer in Turkey who advises on settlement documentation for cross-border insurance claims provides the bilingual drafting service that ensures foreign corporate decision-makers can review and approve settlement terms whose practical effect is clearly explained in a format accessible without translation specialist involvement—and confirms that the settlement documentation uses consistent asset and party descriptions throughout so that no ambiguity exists about what has been settled or what has been retained. Practice may vary by authority and year.

A Turkish Law Firm that advises on comprehensive denial and settlement file management explains that the settlement documentation should be drafted as if a court will read it—because enforcement depends on clarity and because a second dispute about what the settlement meant is as costly as the original coverage dispute. An English speaking lawyer in Turkey who advises on settlement drafting and enforcement for insurance claims implements the specific documentation approach most effective for each settlement situation: defining the insured event, the claim reference, and the payment amount in one clause; defining what documents are exchanged and listing them as named annexes in the settlement index; specifying that settlement authority was obtained before rights are released; and preserving the complete settlement negotiation record, the final settlement, and the payment proof in one bundle with a chronology so that enforcement can proceed immediately if the insurer fails to pay. The best lawyer in Turkey for insurance claims matters combines knowledge of Turkish insurance law, coverage analysis methodology, notice and cooperation obligations, adjuster and expert management, denial defense strategy, settlement documentation, and enforcement mechanics with the English-language communication that enables cross-border policyholders to manage their Turkish insurance claims effectively. Practice may vary by authority and year.

Complaints, Escalation and Litigation Strategy

A lawyer in Turkey who advises on insurance complaints and escalation explains that complaints should be treated as structured opportunities to correct file misunderstandings before positions harden into formal dispute—and that the most effective complaints are those framed around specific record defects such as documents that were delivered but not considered, factual errors about dates, or denial grounds that first appear in the decision letter without prior investigation. An Istanbul Law Firm that advises on insurance complaint management helps policyholders implement the specific complaint approach most effective for each denial situation: sending the complaint through a traceable channel with the delivery proof attached; including the claim chronology table and the exhibit index so the reviewer can verify the insured's points without searching independently; requesting that the insurer confirm it will not add new denial grounds without first requesting the relevant facts; and maintaining a professional tone throughout because complaint correspondence frequently becomes a court exhibit. Turkish lawyers advising on insurance complaints help policyholders understand that a complaint whose structure mirrors a court filing—with exhibit references for every factual assertion and a specific request tied to each record defect—is consistently more effective than a complaint that makes broad allegations of bad faith without specifying the documentary basis, and that a professional, evidence-led complaint tone is more persuasive to an internal reviewer who did not handle the original file than a tone that attributes motive. Practice may vary by authority and year.

An Istanbul Law Firm that advises on escalation and insurance litigation Turkey strategy explains that escalation should be planned as a sequence—complaint to written demand to mediation window to court filing—rather than as a single threat whose effectiveness diminishes if it is repeated without follow-through. Turkish lawyers advising on insurance litigation strategy help policyholders implement the specific approach most effective for each dispute profile: confirming before filing that the claim file contains the correct policy wording and schedule for the loss date with delivery proof; organizing the petition around a claim chronology that cites exhibits by stable labels; attaching the denial letter and cross-referencing it against the investigation file to show any shift in grounds; and keeping the claim amount calculation transparent and supported by invoices whose total matches the petition figure precisely. An English speaking lawyer in Turkey who advises on insurance litigation for cross-border corporate policyholders provides the court-ready bundle management that ensures foreign corporate decision-makers understand the litigation strategy, the evidence available at each stage, and the enforcement steps that follow judgment. Practice may vary by authority and year.

A Turkish Law Firm that advises on venue analysis for insurance litigation in Turkey explains that the classification of the policyholder as consumer or commercial party affects which court is competent and what procedural expectations apply—and that reading the dispute resolution clause in the issued policy wording rather than in marketing materials is the essential first step in any venue analysis. An English speaking lawyer in Turkey who advises on insurance litigation venue and procedure for cross-border disputes implements the specific venue approach most effective for each claim profile: confirming the defendant's legal entity with trade registry details to prevent service delays from naming errors; reviewing whether the policy includes arbitration or expert determination clauses whose application could affect venue strategy; and coordinating service requirements and translation standards for any cross-border elements early. Practice may vary by authority and year — verify current court jurisdiction rules, current procedural standards, and current enforcement mechanisms with qualified counsel before initiating any insurance litigation in Turkey.

A Turkish Law Firm that advises on expert evidence management in insurance litigation explains that expert mandates submitted to Turkish courts should be narrowly defined around the specific clause element whose factual basis is disputed—rather than requesting a broad investigation whose conclusions the court must then interpret—because a well-defined expert mandate produces answers to the specific legal questions that determine the case, while a broad mandate produces a technical report whose relevance to the coverage question must be separately argued. An English speaking lawyer in Turkey who advises on expert coordination for insurance litigation provides the mandate drafting and expert instruction management that keeps technical evidence focused on the coverage elements at issue—preventing the situation where expensive expert work does not advance the case because it addresses technical questions whose answers are not determinative. Practice may vary by authority and year.

Interim Measures, Subrogation Rights and Recovery Planning

A lawyer in Turkey who advises on interim measures for insurance disputes explains that interim injunction insurance dispute Turkey applications require demonstrating both urgency—ongoing harm that cannot wait for judgment—and a plausible substantive right whose existence would be lost if relief is not granted immediately. An Istanbul Law Firm that advises on interim relief for insurance disputes helps policyholders implement the specific interim application approach most effective for each urgency situation: proving urgency with documents showing ongoing non-payment that threatens business continuity rather than relying on assertions; ensuring that the interim petition's exhibit index is consistent with the main claim file so the judge can verify facts quickly; tailoring each interim measure request to the specific harm rather than seeking broad relief that courts often deny as disproportionate; and keeping settlement discussions separate from interim proceedings so negotiation language does not contaminate the procedural record. Turkish lawyers advising on interim measures help policyholders understand that interim applications whose factual record is thin—where evidence was not preserved and where the claim file is not organized—are consistently less successful than applications that demonstrate a coherent evidence base and a specific irreparable harm. Practice may vary by authority and year.

An Istanbul Law Firm that advises on subrogation rights Turkey insurance matters explains that recovery planning should begin before payment because the evidence created during the primary claim investigation—adjuster reports, expert findings, maintenance logs, and causation analysis—is also the evidence needed for subrogation claims against responsible third parties. Turkish lawyers advising on subrogation and recovery management help insurers and policyholders implement the specific recovery approach most effective for each third-party liability situation: sending early preservation notices to potential tortfeasors requesting that they retain their own records; preserving failed parts and documenting chain of custody even when repairs are urgent; confirming that contractual indemnity clauses and liability allocation provisions are included in the recovery file with signature pages; and keeping payment proof and settlement documents organized so defendants cannot later challenge whether the payment was voluntary or whether it was made under reservation. An English speaking lawyer in Turkey who advises on cross-border subrogation for international insurers provides the bilingual coordination that ensures recovery letters and primary claim letters use the same factual narrative—preventing the characterization inconsistencies that defendants exploit to challenge causation in recovery proceedings—and maintains the translation terminology sheet that keeps technical causation descriptions consistent across all recovery communications in all jurisdictions. Practice may vary by authority and year.

A Turkish Law Firm that advises on recovery file management explains that recovery files often fail because evidence was not preserved during the primary claim investigation and because the paying party waited too long before opening the recovery file—and that setting a recovery trigger date in the claim diary and opening a recovery folder as soon as liability indicators appear is the single most important recovery practice improvement available. An English speaking lawyer in Turkey who advises on recovery planning for corporate insurance claimants implements the specific recovery preparation approach most effective for each third-party liability configuration: capturing trade registry identifiers and bank details of potential defendants during the investigation phase; preserving witness contacts while employees and contractors are still accessible; coordinating technical expert mandates so that the same expert evidence supports both the primary claim and the recovery claim; maintaining a consistent factual narrative across the primary claim file and the recovery demand letters; and tracking the limitation period applicable to each potential recovery target so that rights are not lost through delay. Practice may vary by authority and year.

Practical Compliance Roadmap and Claims Governance

A lawyer in Turkey who advises on insurance claims governance explains that a practical claims roadmap should be built as a written playbook before any loss occurs—because teams that improvise under stress create the documentation inconsistencies that become disputes, while teams that follow pre-tested procedures produce consistent chronologies whose integrity withstands adjuster and judicial scrutiny. An Istanbul Law Firm that advises on claims governance for corporate policyholders helps clients implement the specific governance approach most effective for each organization profile: defining who is authorized to give notice and who is authorized to approve repairs; establishing an evidence preservation kit with standard camera instructions, CCTV export steps, and log preservation steps; creating a document index template that is reused for every insurer delivery; creating a standard notice email template that is factual and avoids speculative causation labels; and defining an escalation ladder from complaint to demand letter to court filing. Turkish lawyers advising on claims governance help corporate clients understand that periodic drills—testing portal submission procedures, CCTV export procedures, and incident report templates—convert theoretical playbooks into operational capability whose effectiveness is visible when a real loss occurs. Practice may vary by authority and year.

An Istanbul Law Firm that advises on dispute-ready file management for insurance claims explains that when a dispute appears likely, the most effective response is to centralize all communications through one channel, stop informal discussions, and build a dispute bundle whose completeness and consistency can withstand court examination. Turkish lawyers advising on dispute file preparation help policyholders implement the specific bundle approach most effective for each dispute profile: including the policy schedule and issued wording with delivery proof; adding the complete claim chronology and the master document index; including the adjuster appointment letter, inspection minutes, and all signed expert reports in their final form; adding the complaint correspondence and demand letters with delivery proof; and reviewing the bundle for internal consistency before it is used in any proceeding—correcting any factual drift with a dated clarification note. An English speaking lawyer in Turkey who advises on dispute file coordination for cross-border policyholders provides the bundle management that ensures all translations are consistent with the original documents and that every claim element is supported by at least one exhibit whose delivery to the insurer is evidenced. Practice may vary by authority and year.

A Turkish Law Firm that advises on long-term claims governance improvement explains that using completed claims as feedback to update templates, procedures, and evidence preservation kits is the most practical way to reduce future disputes—because the pattern of what caused friction in closed claims reliably predicts the pattern of what will cause friction in future claims. An English speaking lawyer in Turkey who advises on claims governance program design for corporate and international policyholders implements the specific improvement approach most effective for each organization: running post-claim reviews that identify what caused delays or disputes; updating the document index template to add categories that recurred as missing items; updating the notice email template to clarify any causation language that was later misunderstood; and updating the escalation ladder with the specific timing and evidence thresholds learned from completed dispute proceedings. Practice may vary by authority and year — verify current Turkish insurance procedural requirements, current compliance standards, and current dispute resolution mechanisms applicable to the specific policy line with qualified counsel before finalizing any claims governance arrangements.

A Turkish Law Firm that advises on corporate insurance claims governance explains that the difference between organizations that resolve claims efficiently and organizations that spend years in disputes is almost always the quality of their pre-loss documentation habits—specifically whether policy storage, evidence preservation kits, notice authority assignments, and incident reporting templates are operational before any loss occurs. An English speaking lawyer in Turkey who advises on claims governance program design for corporate and international policyholders provides the program implementation guidance that converts theoretical compliance intentions into tested operational procedures—including periodic drills that verify whether CCTV export steps work, whether portal submission acknowledgments are received, and whether incident report templates produce internally consistent outputs. Practice may vary by authority and year.

A Turkish Law Firm that advises on post-claim dispute file management explains that when a claim moves into formal dispute, the most effective defensive preparation is building a dispute bundle whose completeness and internal consistency can withstand court examination from the first day of filing rather than being assembled under filing deadline pressure. An English speaking lawyer in Turkey who advises on dispute file preparation for cross-border corporate policyholders provides the systematic bundle management that ensures all translations are consistent with the original documents, every claim element is supported by a specific exhibit, and each exhibit's delivery to the insurer is evidenced—so that the dispute bundle is a complete and coherent record rather than a collection of separately assembled document sets that must be reconciled before they can be used. Practice may vary by authority and year.

Frequently Asked Questions

- What is the first step in the insurance claims process in Turkey? The first step is giving timely written notice to the insurer identifying the policy number, the loss date, the location, and the type of damage—without speculative causation labels. Request a written acknowledgment containing a claim reference number. Create a parallel personal claim file from the first day with copies of all communications sent and received. Practice may vary by authority and year.

- What documents are needed for an insurance claim in Turkey? Core insurance claim documents Turkey include the final issued policy schedule and wording for the relevant policy period, ownership or insurable interest proof, photographs taken before repairs, official incident reports, maintenance and service records, and identity documentation. Additional documents vary by line of insurance. Deliver all documents through one channel with a cover letter and an index, and request written receipt confirmation. Practice may vary by authority and year.

- How should evidence be preserved after an insurance loss in Turkey? Evidence preservation insurance claim Turkey practice requires photographing the scene before repairs, exporting CCTV footage promptly with documented chain of custody, preserving damaged components and product samples, collecting maintenance logs and service records, and creating an evidence index that lists each item with its date and collector. Digital evidence should preserve original metadata. Practice may vary by authority and year.

- What is the role of the insurance adjuster in Turkey? The insurance adjuster Turkey claim role is to inspect the site, interview stakeholders, request documents, and produce a factual report that the insurer uses in its coverage decision. The insured should confirm the adjuster identity and mandate in writing, keep an inspection log, request correction of factual errors promptly, and ensure that the same consistent chronology is presented to the adjuster as in the written notice. Practice may vary by authority and year.

- What should an insured do when receiving a reservation of rights letter? Respond in writing, confirm receipt, provide indexed documents, correct any factual errors with delivery proof, and ask the insurer to clarify ambiguous requests. Treat the letter as a litigation-readiness trigger by preserving all evidence, freezing relevant emails, and organizing the exhibit index. Practice may vary by authority and year.

- What are the most common reasons for insurance claim denial in Turkey? Common denial reasons include late or defective notice, alleged non-disclosure at underwriting, exclusion application, breach of cooperation or mitigation conditions, disputed causation through expert report, and disputed quantum. Each denial reason should be addressed element by element with specific exhibits—notice denial is rebutted by delivery proof, exclusion denial by element-by-element wording analysis, causation denial by preserved technical evidence. Practice may vary by authority and year.

- How should a policyholder respond to an insurance claim denial in Turkey? Request a written denial letter specifying the factual basis and policy terms relied upon. Build a defense by mapping each denial element to a specific exhibit. If the denial depends on technical causation, obtain the raw data basis of the insurer's expert report and challenge methodology. If the denial shifted grounds during investigation, document the shift as a credibility point. Practice may vary by authority and year.

- How does insurance settlement negotiation work in Turkey? Insurance settlement negotiation Turkey practice requires freezing the chronology and exhibit index before exchanging numbers; supporting any proposed amount with invoices, quotations, and a transparent calculation worksheet; requesting that counter-proposals include the data basis; and documenting settlement authority internally before negotiations begin. The settlement agreement should specify payment channel, currency, invoice form, and precise release scope. Practice may vary by authority and year.

- What is an interim injunction in an insurance dispute in Turkey? An interim injunction insurance dispute Turkey application asks a court to preserve evidence, secure assets, or prevent disposal of disputed property while the main claim is pending. The application must demonstrate both urgency and a plausible substantive right. Evidence of ongoing harm and a coherent claim file are required. Applications whose factual record is thin are consistently less successful. Practice may vary by authority and year.

- How should a policyholder file a complaint about an insurance claim denial in Turkey? Frame the complaint around specific record defects—documents delivered but not considered, factual errors, shifted denial grounds. Send through a traceable channel with delivery proof. Attach the claim chronology and exhibit index so the reviewer can verify points independently. Maintain a professional tone throughout as complaint correspondence frequently becomes a court exhibit. Practice may vary by authority and year.

- What is subrogation and how does recovery planning work in insurance claims in Turkey? Subrogation rights Turkey insurance allows the paying insurer to pursue responsible third parties after indemnity is paid. Recovery planning should start during the primary claim investigation by preserving causation evidence, sending preservation notices to potential tortfeasors, and confirming that contractual indemnity provisions are included in the recovery file. Payment proof and settlement documents must be organized for recovery demand letters. Practice may vary by authority and year.

- What mitigation obligations apply in Turkish insurance claims? The insured must take reasonable documented steps to prevent the loss from worsening. Photograph each mitigation step with before-and-after images; keep invoices and authorization records for emergency work; retain damaged parts for insurer inspection; and document any instance where the insurer's delayed inspection required proceeding with mitigation before inspection was complete. Practice may vary by authority and year.

- When should a policyholder engage legal counsel for an insurance claim in Turkey? Legal counsel should be engaged early in high-value claims, claims where the insurer has issued a reservation of rights letter, claims with cross-border elements requiring consistent bilingual documentation, and any claim where denial appears likely. Insurance lawyer Turkey claim support is most valuable when it keeps the evidence file consistent, prevents avoidable admissions, and coordinates the coverage analysis with the document strategy before the first adjuster interaction. Practice may vary by authority and year.

- What are the key elements of a practical insurance claims governance program? A practical governance program includes a written playbook covering policy storage, notice authority, evidence preservation kits, and escalation ladders; periodic drills testing portal submissions and CCTV exports; an incident register linking each incident to a claim folder; post-claim reviews updating templates based on friction patterns; and centralized communication discipline requiring all insurer communications to pass through one designated contact. Practice may vary by authority and year.

- Does ER&GUN&ER Law Firm provide legal services for insurance claims in Turkey? Yes. ER&GUN&ER Law Firm provides legal services for insurance claims in Turkey including policy identification and coverage mapping, notice and first-step documentation management, evidence preservation strategy, adjuster and expert coordination, cooperation obligation management, reservation of rights letter responses, denial defense preparation, settlement negotiation and documentation, complaint and escalation management, insurance litigation preparation and filing, interim measures applications, subrogation and recovery planning, and claims governance program design—with English-language client communication and bilingual documentation throughout each engagement.

Author: Mirkan Topcu is an attorney registered with the Istanbul Bar Association (Istanbul 1st Bar), Bar Registration No: 67874. His practice focuses on cross-border and high-stakes matters where evidence discipline, procedural accuracy, and risk control are decisive.

He advises individuals and companies across Immigration and Residency, Real Estate Law, Tax Law, and cross-border documentation matters where procedural accuracy and evidence discipline are decisive.

Education: Istanbul University Faculty of Law (2018); Galatasaray University, LL.M. (2022). LinkedIn: Profile. Istanbul Bar Association: Official website.