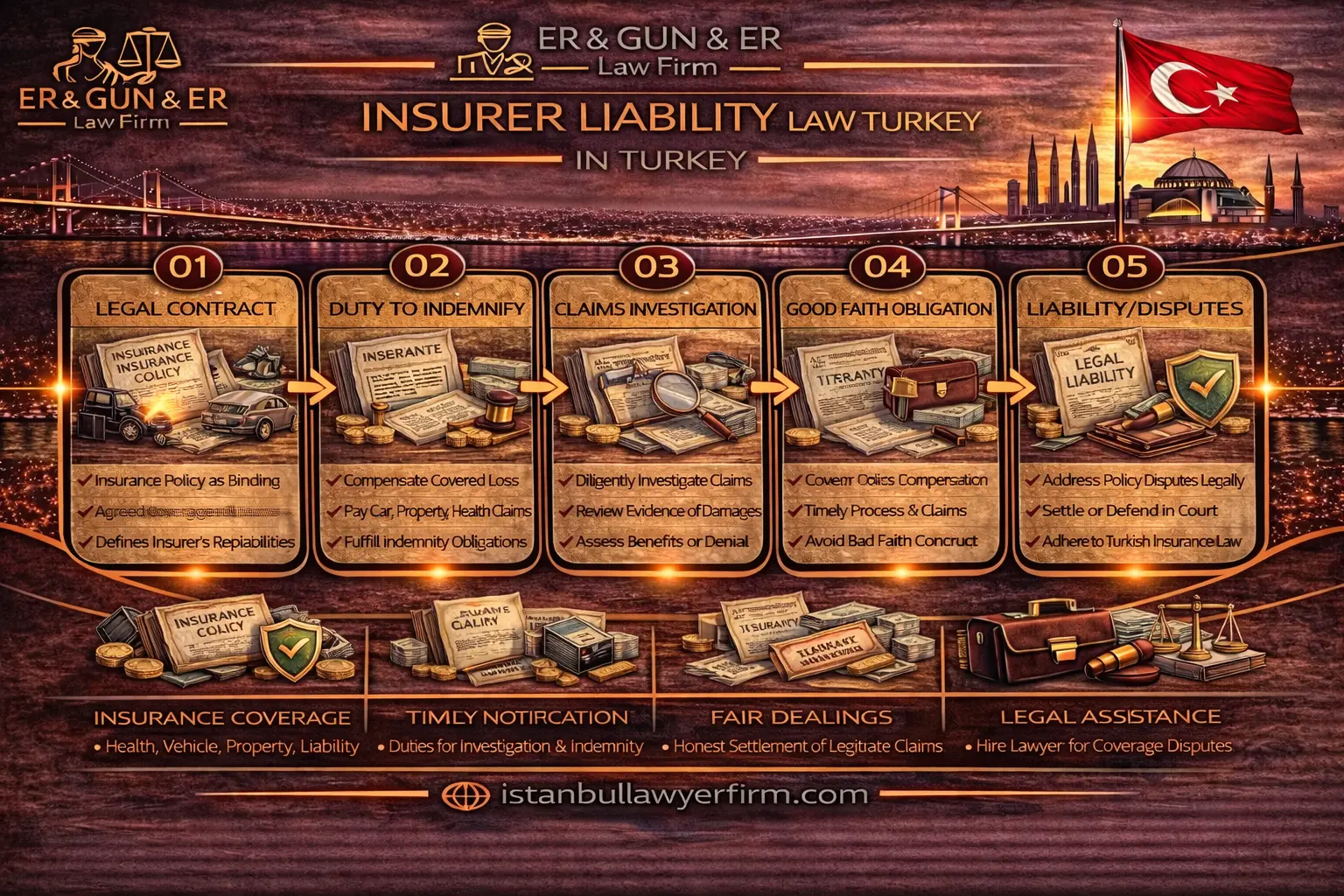

A lawyer in Turkey who advises on insurer liability understands that insurer liability law Turkey describes the conditions under which an insurer must pay, explain, or rectify a claim decision under policy terms and general contract and good faith principles—and that most insurer liability disputes arise from coverage scope disagreements, exclusion application arguments, causation questions, and alleged failures to satisfy notice and documentation conditions whose outcomes are determined almost entirely by the quality of the documentary record rather than by the parties' subjective assessments of fairness. An Istanbul Law Firm that advises on insurer liability Turkey provides the integrated guidance covering every stage of this liability analysis: confirming the insurer's specific payment obligations under the final issued policy and endorsements; evaluating good faith compliance through the investigation record, communication discipline, and decision consistency; addressing disclosure and misrepresentation arguments through the pre-contract documentation archive; building element-by-element responses to exclusion and causation defenses; managing notice and cooperation compliance to prevent procedural denials; coordinating adjuster and expert management as formal evidentiary governance; analyzing payment obligation, interest, and damages claims on a strict proof basis; and planning insurance litigation Turkey strategy and enforcement as a connected evidentiary exercise. A Turkish Law Firm that advises on insurer liability for both insurers and policyholders understands that the decisive variable in nearly every insurance claim denial dispute Turkey is the quality and completeness of the file rather than the strength of abstract legal argument—making documentation discipline, indexed delivery, and consistent correspondence the most important operational investments available to all parties in a coverage dispute. An English speaking lawyer in Turkey who advises on insurer liability for cross-border policyholders provides the bilingual coordination that keeps notice narratives, investigation responses, expert instructions, and court submissions consistent across languages and decision-making levels. Practice may vary by authority and year — verify current Turkish insurance liability standards, current good faith requirements, and current enforcement mechanisms with qualified counsel before taking any action, since insurer liability standards are applied through regulatory guidance and judicial practice whose current versions determine the specific requirements applicable to each line of insurance, each policy type, and each factual situation.

Insurer Liability Law Turkey: Core Concepts, Good Faith Duties and Investigation Standards

A lawyer in Turkey who advises on insurer liability concepts explains that the insurer's payment obligation is triggered only when the insured proves an insured event that falls within the coverage grant of the final issued policy—and that insurer liability law Turkey disputes arise most frequently when courts must determine whether the insurer applied the grant consistently, whether its investigation was structured and proportional, and whether its denial letter accurately reflected the file's factual findings rather than introducing new grounds that were never investigated. An Istanbul Law Firm that advises on insurer liability for policyholders and insurers helps parties understand the specific liability framework most important for each dispute type: confirming that an insurance coverage dispute Turkey is ultimately decided by courts who test the file for consistency between investigation record and decision letter; confirming that a shift in denial grounds across correspondence is treated as a credibility problem that weakens the insurer's position; and confirming that an insurer whose file shows structured investigation, proportional requests, and reasoned decision-making is significantly more defensible than one whose decisions appear arbitrary or whose investigation gaps are unexplained. Turkish lawyers advising on insurer liability help parties understand that the decisive investment is building a file whose chronology allows verification of each decision step rather than relying on the inherent authority of the insurer's position—and that a file whose investigation steps are documented with timestamps, whose requests are linked to specific coverage elements, and whose decisions follow from the collected evidence is consistently more defensible than a file that reaches identical conclusions through undocumented reasoning. Practice may vary by authority and year.

An Istanbul Law Firm that advises on the insurer duty of good faith Turkey explains that good faith is a general contract principle that shapes how the insurer investigates and communicates—and that the practical markers of good faith are a request log that shows proportionality, an investigation record that shows engagement with the insured's exhibits, and a decision letter that accurately summarizes the file rather than mischaracterizing evidence or introducing factors not present in the investigation. Turkish lawyers advising on good faith compliance help organizations implement the specific file discipline most effective for each duty: avoiding arbitrary delay by maintaining a dated chronology with a decision milestone; avoiding shifting reasons by confirming internal consistency between coverage memos and external letters before dispatch; tailoring document requests to the coverage trigger and causation question rather than requesting generic data whose relevance is unexplained; and documenting internal approvals for denial decisions so courts can see that decisions were process-based rather than discretionary. An English speaking lawyer in Turkey who advises on good faith compliance for cross-border insurance operations provides the bilingual coordination that keeps cross-border files consistent—preventing the inconsistencies between Turkish-language file notes and English-language management communications that create credibility problems when both sets of documents are disclosed—and confirming that the same factual description of the loss event is used in Turkish-language internal memos and English-language management reports to prevent the interpretation gaps that opposing parties convert into evidence of inconsistency. Practice may vary by authority and year.

A Turkish Law Firm that advises on claims investigation insurer Turkey standards explains that the investigation record is the foundation of every insurer liability defense—and that an investigation file whose every step is documented with timestamps, whose requests are linked to coverage elements, whose expert mandates are defined in writing, and whose decision follows from the collected evidence is consistently more defensible than a file that reaches the same conclusion through undocumented reasoning. An English speaking lawyer in Turkey who advises on investigation governance for complex insurance claims implements the specific investigation approach most effective for each claim type: opening a file note that states what is known, what is unknown, and what evidence is needed to decide; requesting documents that directly answer those specific unknowns; appointing adjusters and experts with written mandates whose scope is tied to policy clause elements; maintaining a status communication that informs the insured of each investigative step without prejudging the outcome; and confirming that denial letters are not dispatched until the decision memo is internally consistent with every exhibit in the file. The best lawyer in Turkey for insurer liability matters combines knowledge of Turkish insurance liability law, good faith standards, investigation discipline, disclosure and misrepresentation analysis, exclusion and causation methodology, notice and cooperation compliance, adjuster and expert management, payment obligation and damages analysis, and litigation and enforcement strategy with the English-language communication that enables cross-border policyholders and insurers to manage Turkish insurance liability effectively. Practice may vary by authority and year.

Disclosure, Misrepresentation and Coverage Grant Obligations

A lawyer in Turkey who advises on disclosure obligations in insurance explains that most misrepresentation insurance Turkey dispute files succeed or fail based on three documents—the proposal form or questionnaire, the broker submission pack if applicable, and the issuance record showing what wording was delivered—and that an insurer relying on misrepresentation must show both that a material fact was misstated and that the fact mattered to the risk, with courts consistently scrutinizing whether the fact was even asked in the documented process. An Istanbul Law Firm that advises on disclosure disputes for policyholders and insurers helps parties implement the specific approach most effective for each disclosure situation: confirming through the quotation emails, drafts, and broker correspondence what was actually communicated and when; testing whether the alleged missing fact was requested through a specific written question; and assessing whether the insurer's prior conduct—including premium acceptance and renewal without raising the disclosure issue—affects the disclosure defense. Turkish lawyers advising on disclosure disputes help policyholders understand that preserving all pre-contract communications in dated form—including correction emails and delivery proofs—is the most effective single action for preventing a disclosure allegation from becoming a viable denial ground. Practice may vary by authority and year.

An Istanbul Law Firm that advises on coverage grant obligations in insurer liability law explains that the coverage grant is the core promise whose consistent application determines whether the insurer satisfied or breached its contractual obligation—and that policy coverage analysis Turkey on the final issued wording and endorsements is the first mandatory step, because courts rely on the contract text rather than marketing summaries and because coverage applied under the wrong wording version is a common avoidable litigation embarrassment. Turkish lawyers advising on coverage grant compliance help parties implement the specific coverage analysis most effective for each claim type: confirming that the insured event matches the grant language rather than only the common label used in emails; mapping each coverage element—trigger, property or person covered, causation requirement, territorial scope—to a specific exhibit; and confirming that the claimant is the named insured or a documented beneficiary under the specific policy version applicable to the loss date. An English speaking lawyer in Turkey who advises on coverage grant analysis for cross-border insurance claims provides the systematic coverage mapping that confirms each element is addressed by documentary evidence—preventing the situation where coverage is assumed to exist based on the general nature of the policy rather than confirmed through clause-by-clause analysis of the issued text. Practice may vary by authority and year.

A Turkish Law Firm that advises on the integrated disclosure and coverage framework explains that insurers have an obligation to apply the coverage grant consistently across similar fact patterns—and that when coverage is applied differently to similar events without documented explanation, courts treat the inconsistency as evidence of arbitrary denial rather than as a legitimate exercise of underwriting judgment. An English speaking lawyer in Turkey who advises on coverage consistency for insurers implements the specific governance approach most effective for each portfolio: maintaining a request log with timestamps that shows investigation was structured and relevant; documenting what factual evidence was considered and whether the insured's exhibits were engaged; and confirming that denial letters do not introduce grounds that were never investigated. Practice may vary by authority and year — verify current Turkish coverage analysis standards, current disclosure requirements, and current grant application methodology with qualified counsel before taking any action in an insurance coverage dispute.

Exclusions, Causation Analysis and Evidence Framework

A lawyer in Turkey who advises on exclusion interpretation in insurance disputes explains that exclusions must be applied through the exact wording delivered to the insured for the relevant policy period—and that the first step in any exclusion analysis is confirming the correct wording and endorsements, because exclusions frequently change at renewal or via mid-term endorsement in ways whose non-disclosure becomes a separate argument against the exclusion's effectiveness. An Istanbul Law Firm that advises on exclusion defense for insurers and policyholders helps parties implement the specific approach most effective for each exclusion type: mapping each exclusion as a checklist of elements rather than applying a label; linking each element to a specific factual exhibit; confirming that the insurer can show the exclusion trigger with evidence rather than speculation; and assessing whether any carve-out to the exclusion is activated by facts that the insured can prove with specific evidence. Turkish lawyers advising on exclusion analysis help policyholders understand that requesting the adjuster report's raw data basis is frequently the most effective single action for challenging an exclusion defense—because adjuster report insurance dispute Turkey arguments often fail when the underlying technical data does not support the conclusions. Practice may vary by authority and year.

An Istanbul Law Firm that advises on causation analysis for insurance liability disputes explains that causation analysis is the technical bridge between the factual event and the policy response—and that disputes about causation must be resolved through experts with narrow mandates tied to specific policy clause elements rather than through broad technical investigations whose conclusions drift away from the legal questions the court must answer. Turkish lawyers advising on causation analysis help parties implement the specific evidence approach most effective for each causation dispute: preserving the physical and digital evidence before repairs begin so expert conclusions are based on original materials rather than reconstructed assumptions; confirming that competing expert reports are compared by methodology and data rather than by authority; and insisting that multi-cause analyses specifically allocate which cause triggers which exclusion rather than relying on a general statement that the loss is excluded. An English speaking lawyer in Turkey who advises on causation analysis for cross-border insurance disputes provides the bilingual technical coordination that keeps causation descriptions consistent across expert instructions, correspondence, and court submissions—preventing the terminology drift whose inconsistency defendants exploit to argue that multiple different events are being described across different documents. Practice may vary by authority and year.

A Turkish Law Firm that advises on the integrated evidence framework for insurance exclusion disputes explains that the burden of proof in exclusion litigation typically requires the insurer to prove the exclusion trigger while the insured rebuts with evidence that the carve-out conditions are satisfied—and that both parties' evidence strength depends entirely on the quality of the preservation decisions made during the first days after the loss event. An English speaking lawyer in Turkey who advises on evidence framework design for complex insurance exclusion disputes implements the specific approach most effective for each exclusion defense: building a preservation protocol that captures pre-loss condition evidence, maintenance records, and service logs before repairs alter the physical evidence; confirming that raw data and laboratory outputs are preserved alongside expert reports; and aligning the evidence framework with the specific clause elements so every exhibit is linked to a specific coverage question rather than collected broadly and organized after the fact. Practice may vary by authority and year.

Notice and Cooperation Duties: Proof Standards and Defense Strategies

A lawyer in Turkey who advises on notice and cooperation duties explains that notice obligation insurance Turkey disputes and cooperation clause insurance Turkey disputes are common denial grounds whose success depends on whether the insurer can demonstrate actual prejudice from the alleged failure—and that courts assess notice and cooperation disputes by looking at what each party did during each period of the claim rather than by accepting general allegations of deficiency. An Istanbul Law Firm that advises on notice and cooperation compliance helps policyholders implement the specific compliance approach most effective for each claim situation: preserving the first internal incident report, the first written notice to the insurer, and the insurer's acknowledgment; documenting in writing why any delay occurred so courts can assess reasonableness on facts rather than on assumption; and maintaining an indexed delivery record whose completeness defeats non-cooperation allegations by showing a pattern of prompt, documented responses. Turkish lawyers advising on notice and cooperation compliance help organizations understand that implementing an internal incident reporting protocol that triggers immediate notice review for all policies is the most effective single governance investment for preventing procedural denial grounds from arising. Practice may vary by authority and year.

An Istanbul Law Firm that advises on notice and cooperation defense strategy for insurers explains that notice and cooperation arguments are strongest when they are grounded in a specific documented request that received no response—and that general allegations that cooperation was poor rarely succeed without timestamps, specific document descriptions, and a demonstration of actual prejudice to the insurer's ability to investigate. Turkish lawyers advising on insurer notice and cooperation defense help insurers implement the specific approach most effective for each alleged cooperation failure: maintaining a request log with dates, document descriptions, and delivery proofs that shows the insurer's investigation was structured and proportional; documenting the specific investigation capability that was lost due to the alleged failure rather than asserting prejudice generally; and confirming that the insurer pursued every available alternative investigation approach before relying on non-cooperation as a denial ground. An English speaking lawyer in Turkey who advises on notice and cooperation compliance for cross-border corporate policyholders provides the coordination framework that ensures different departments do not send inconsistent responses to the same insurer—preventing the factual contradictions between parallel communications that insurers cite as evidence of non-cooperation. Practice may vary by authority and year.

A Turkish Law Firm that advises on the relationship between notice and cooperation duties and good faith obligations explains that cooperation disputes frequently become a proxy for causation disputes—because insurers invoke non-cooperation when causation evidence is uncertain—and that the most effective defense against a cooperation-based denial is preserving causation evidence promptly and offering inspection access immediately so the non-cooperation allegation cannot be supported by factual evidence of investigation impairment. An English speaking lawyer in Turkey who advises on integrated notice and cooperation strategy for complex insurance disputes implements the specific approach that builds a mutual chronology table showing what each party did during each period—converting the abstract allegation of non-cooperation into a specific factual question whose answer is visible in dated delivery logs and inspection records. Practice may vary by authority and year — verify current Turkish notice obligation standards, current cooperation duty requirements, and current prejudice analysis methodology with qualified counsel before taking any action in a notice or cooperation dispute.

Adjuster and Expert Management in Insurance Liability Disputes

A lawyer in Turkey who advises on adjuster management in insurance liability disputes explains that adjusters are the insurer's fact-gathering function whose mandate, inspection scope, and report integrity determine the quality of the investigation record on which the insurer will ultimately rely—and that confirming the adjuster mandate in writing, maintaining an inspection attendance note, documenting chain of custody for samples taken, and requesting the signed final report with version control are the minimum steps required to build an adjuster record that withstands later dispute scrutiny. An Istanbul Law Firm that advises on adjuster management for insurers and policyholders helps parties implement the specific approach most effective for each adjuster interaction: confirming in writing which questions the adjuster is tasked to answer; ensuring that interim adjuster updates are logged and delivery-evidenced; requesting correction of factual errors in preliminary reports promptly; and maintaining a document delivery log that shows which exhibits the adjuster received and at what date. Turkish lawyers advising on adjuster management help organizations understand that adjuster report insurance dispute Turkey arguments frequently fail not because the adjuster's conclusions were wrong but because the process record is missing—making process documentation as important as substantive accuracy. Practice may vary by authority and year.

An Istanbul Law Firm that advises on expert management in insurance liability disputes explains that experts differ from adjusters because they provide technical opinions that can decide causation and quantum—and that expert mandates that are too broad generate irrelevant conclusions that confuse courts while mandates that are too narrow miss decisive technical elements, making mandate precision the most important single variable in managing expert evidence quality. Turkish lawyers advising on expert management help parties implement the specific approach most effective for each technical dispute: defining the expert mandate in terms of the specific policy clause element whose factual basis is in dispute; requiring the expert to document what materials were reviewed and what materials were unavailable; preserving raw data including measurements, laboratory outputs, and device logs so conclusions are verifiable; and confirming that joint inspection protocols are documented in writing with meeting minutes exchanged for correction. An English speaking lawyer in Turkey who advises on expert management for cross-border insurance disputes provides the bilingual technical coordination that ensures expert reports address the specific policy clause elements in terminology consistent across the investigation file, the correspondence record, and any court submissions—preventing the technical language inconsistencies that courts interpret as narrative drift—and maintains the terminology sheet that prevents transliteration differences from creating the appearance of inconsistent causation narratives. Practice may vary by authority and year.

A Turkish Law Firm that advises on the integrated adjuster and expert governance framework for insurance liability disputes explains that expert evidence is persuasive only when the claim file demonstrates that the insurer and insured cooperated on access and data—and that emergency repair situations, where physical evidence may be altered before inspection, require specific documentation of the urgency rationale and pre-repair photographs that allow experts to reconstruct the condition even without access to the original physical evidence. An English speaking lawyer in Turkey who advises on complex adjuster and expert coordination for multinational insurance disputes implements the specific governance approach that ensures translation of expert technical terms is consistent across every annex, that raw data and signed final report versions are archived together with the mandate letter, and that internal approval records document why one expert opinion was preferred over a competing report. Practice may vary by authority and year.

Payment Obligations, Partial Payments and Interest Claims

A lawyer in Turkey who advises on insurance claim payment obligation Turkey explains that payment obligations arise when the insured proves an insured event and the insurer has sufficient documented material to make a coverage and quantum decision—and that the insurance claim payment obligation Turkey analysis focuses on when the file became decision-ready, when that readiness was confirmed, and whether any subsequent delay was caused by the insurer's own investigation steps or by the insured's documentation delivery. An Istanbul Law Firm that advises on payment obligation management helps parties implement the specific approach most effective for each payment situation: documenting when each requested document was delivered and requesting written completeness acknowledgment; confirming that the insurer has scheduled any required inspection promptly after document delivery so the insurer cannot use pending inspection as an indefinite payment delay mechanism; and separating coverage analysis from quantum refinement so coverage decisions can be made while specific valuation questions are resolved. Turkish lawyers advising on payment obligation management help policyholders understand that building a dated chronology of document delivery and completeness confirmation is the foundation of every interest on unpaid insurance claim Turkey argument—because interest claims are only viable when the policyholder can show that the file was decision-ready and payment was nonetheless withheld. Practice may vary by authority and year.

An Istanbul Law Firm that advises on partial payment disputes for insurance claims explains that partial payments create secondary disputes when the allocation between accepted and disputed heads is not documented in writing—and that the insured should insist that any partial payment is accompanied by a written breakdown showing which heads are accepted, which remain disputed, and on what basis each disputed item is withheld. Turkish lawyers advising on partial payment management help policyholders implement the specific approach most effective for each allocation dispute: confirming that partial payment acceptance is documented as without prejudice to the disputed balance; requesting the insurer's specific clause or condition basis for withholding each disputed cost item; responding with an updated index that shows exactly where each supporting document sits for each disputed item; and preserving bank proofs and payment records so the allocation is traceable in any subsequent enforcement or litigation. An English speaking lawyer in Turkey who advises on partial payment disputes for cross-border corporate policyholders provides the bilingual financial coordination that ensures allocation breakdowns are consistently described in both Turkish-language and English-language communications—preventing the miscommunication between local and group functions that creates inconsistent payment records. Practice may vary by authority and year.

A Turkish Law Firm that advises on damages for wrongful denial Turkey insurance explains that additional monetary remedies beyond the insured amount require strict proof of a causal link between the insurer's specific conduct—such as ignoring a decisive exhibit or refusing inspection without reason—and a specific consequential loss documented through external dated evidence such as bank financing letters, customer termination notices, or asset disposal records. An English speaking lawyer in Turkey who advises on interest and damages claims for insurance payment failures implements the specific approach most effective for each damages claim: treating interest arguments as an evidence exercise that links document delivery dates to insurer acknowledgment dates; maintaining a consequential loss ledger whose every entry is supported by a bank proof or dated third-party document; and framing damages claims specifically around identified insurer conduct rather than general characterizations of bad faith. Practice may vary by authority and year — verify current Turkish payment obligation standards, current interest calculation methodology, and current damages for wrongful denial standards with qualified counsel before asserting any payment obligation or damages claim.

Denial Strategies, Damages Framework and Consumer versus Commercial Disputes

A lawyer in Turkey who advises on denial response strategy explains that insurance claim denial dispute Turkey responses are most effective when they address each denial ground element by element with a specific exhibit rather than with general arguments about commercial fairness—and that the insured's first action upon receiving a denial letter should be requesting a written final position that identifies the exact clause and factual trigger for each reason, because that written position fixes the dispute posture and prevents the insurer from shifting grounds in later correspondence. An Istanbul Law Firm that advises on denial defense for policyholders helps implement the specific response approach most effective for each denial category: if the insurer alleges late notice, producing first notice proof and claim number acknowledgment with delivery evidence; if the insurer cites an expert report, obtaining the signed report and raw data basis; if the insurer alleges non-cooperation, producing the indexed delivery log showing every request and every response. Turkish lawyers advising on denial defense help policyholders understand that documenting ground shifts across correspondence—where the insurer changes its stated reason between letters—is one of the most effective tools for challenging denial credibility in insurance litigation Turkey. Practice may vary by authority and year.

An Istanbul Law Firm that advises on the damages framework for wrongful denial claims explains that courts are skeptical of broad bad faith labels without proof—and that effective damages pleadings identify the specific insurer act, such as ignoring a decisive exhibit or refusing an inspection invitation, connect it to a specific documented consequence, and support each consequence with dated external evidence rather than internal estimates. Turkish lawyers advising on damages framework design help policyholders implement the specific proof approach most effective for each damages category: pleading each additional loss as a specific item whose causal link to the insurer's conduct is provable through a contemporaneous external record; avoiding over-claiming because over-claiming reduces credibility and increases litigation cost; and confirming that any consequential loss claim is secondary to the primary coverage entitlement because damages fail if coverage fails. An English speaking lawyer in Turkey who advises on the damages framework for cross-border policyholders provides the bilingual pleading coordination that ensures consequential loss evidence assembled in multiple countries is presented consistently in the Turkish forum. Practice may vary by authority and year.

A Turkish Law Firm that advises on consumer versus commercial insurance dispute dynamics explains that consumer insurance disputes Turkey involve heightened scrutiny of disclosure clarity and the insured's ability to understand exclusions at the time of contracting—while commercial insurance disputes Turkey assume more sophisticated parties but still require coherent insurer reasoning and a stable evidential record—making the first practical step in any dispute the accurate classification of the policyholder's status based on the actual relationship and policy purpose. An English speaking lawyer in Turkey who advises on consumer versus commercial classification for cross-border insurance disputes provides the classification analysis that determines which forum dynamics apply and which disclosure and governance documentation must be preserved—and confirms that the same indexed file discipline produces defensible outcomes in both consumer and commercial settings because courts in both contexts evaluate the written record. Practice may vary by authority and year.

Insurance Litigation, Burden of Proof, Enforcement and Collection

A lawyer in Turkey who advises on insurance litigation Turkey strategy explains that burden of proof drives case strategy because courts allocate proof tasks between insured and insurer—with the insured typically proving the insured event, insurable interest, and quantum through credible documents; and the insurer typically proving exclusion triggers and condition breaches relied upon for denial—making the most important investment in any insurance litigation the quality of the indexed exhibit file whose completeness allows the judge to verify each allocated proof task without requiring reconstruction of history. An Istanbul Law Firm that advises on insurance litigation strategy for complex disputes helps parties implement the specific approach most effective for each dispute type: building a petition that separates coverage trigger facts from notice and cooperation facts so the court sees distinct manageable issue clusters; attaching the full policy set and endorsement history so clause arguments can be verified; and proposing narrow expert mandates tied to the specific technical questions whose factual resolution determines coverage outcomes. Turkish lawyers advising on insurance litigation help parties understand that pleadings that avoid contradicting earlier complaint letters—because courts treat description drift as credibility failures—are consistently more effective than pleadings drafted without reference to the pre-litigation correspondence record. Practice may vary by authority and year.

An Istanbul Law Firm that advises on enforcement and collection for insurance judgments and settlements explains that winning a judgment or settlement is only the beginning if payment is not voluntary—and that enforcement of insurance judgment Turkey requires confirming the correct insurer entity through trade registry records before filing, drafting settlement agreements with clear payment mechanics and proof standards, and maintaining a clean calculation sheet that separates principal, awarded interest, costs, and any partial payments. Turkish lawyers advising on enforcement and collection help policyholders implement the specific approach most effective for each collection situation: confirming enforcement feasibility by identifying the insurer entity's assets and banking relationships during litigation rather than after judgment; treating post-settlement payment failure as a procedural project with a dated submission record and documented compliance confirmation; and coordinating with the enforcement office efficiently so procedural objections receive evidence-backed responses rather than informal rebuttals. An English speaking lawyer in Turkey who advises on enforcement coordination for cross-border insurance judgments provides the systematic enforcement file management that ensures each submission to execution offices is supported by accurate debtor identification and current balance calculations—preventing the avoidable delays that arise when enforcement documents are assembled under time pressure rather than prepared in parallel with the litigation. Practice may vary by authority and year.

A Turkish Law Firm that advises on integrated litigation and recovery strategy for insurance disputes explains that parallel recourse actions against third parties responsible for the loss should be planned during litigation rather than after judgment—because evidence preservation decisions made during the primary dispute determine recourse viability, and because coordinating the insurance claim causation narrative with the recourse demand causation narrative prevents the factual inconsistencies that defendants exploit in both proceedings. An English speaking lawyer in Turkey who advises on integrated insurance litigation and enforcement for complex disputes implements the specific approach that keeps the insurance claim file, the litigation bundle, and the enforcement file as three versions of the same indexed chronology—so that each proceeding benefits from the documentation investment made in the previous stage rather than requiring independent reconstruction. Practice may vary by authority and year — verify current Turkish insurance litigation standards, current burden of proof allocation, current enforcement procedures, and current parallel recovery coordination requirements with qualified counsel before initiating any insurance litigation or enforcement proceeding.

A Turkish Law Firm that advises on the practical roadmap for insurer liability disputes explains that both insurers and policyholders benefit from treating every claim file as a potential liability file from the first day—and that the most effective single investment in insurer liability risk management is establishing a standardized claim file architecture whose chronology, exhibit index, and communication log allow every decision step to be demonstrated without reconstruction. An English speaking lawyer in Turkey who advises on claim file architecture for complex insurance disputes provides the systematic design that ensures the same indexed file structure serves simultaneously as the cooperation record, the coverage analysis evidence, the quantum proof, and—if escalation occurs—the court submission bundle without requiring any additional organizational work under dispute pressure. Practice may vary by authority and year.

A Turkish Law Firm that advises on disclosure and misrepresentation risk management explains that the disclosure archive whose preservation begins at the proposal stage and whose contents are confirmed and updated at each renewal is the most reliable protection against misrepresentation allegations—because a complete dated archive demonstrating that the insured provided specific information in response to specific questions leaves the insurer with the burden of showing that the information was wrong in a way that mattered to the risk. An English speaking lawyer in Turkey who advises on disclosure archive design for cross-border corporate policyholders implements the specific archiving approach that captures all quotation communications, correction emails, broker submission confirmations, and insurer acknowledgments in a dated indexed file maintained in parallel with the policy register—so that any misrepresentation allegation can be addressed immediately by reference to a specific document rather than by reconstructing a communication history under dispute pressure. Practice may vary by authority and year.

A Turkish Law Firm that advises on the governance of enforcement and collection in insurance disputes explains that enforcement planning should be integrated into the litigation strategy from the beginning—because identifying the correct insurer entity, confirming asset locations, and preparing the calculation basis before judgment is obtained consistently produces faster collection than beginning enforcement preparation after judgment—and that a settlement agreement drafted with clear payment mechanics, a specific proof standard for confirming payment, and an automatic enforcement trigger for payment failure is more valuable than an identical settlement whose ambiguous terms create a second dispute about what was agreed. An English speaking lawyer in Turkey who advises on enforcement integration for multinational insurance disputes provides the coordinated enforcement preparation that ensures the litigation bundle, the settlement document, and the execution file all reference the same insurer entity with the same identification data—preventing the avoidable delays that arise when enforcement submissions contain inconsistent entity descriptions. Practice may vary by authority and year.

A Turkish Law Firm that advises on continuous improvement in insurance liability dispute management explains that using each completed dispute as feedback to update coverage maps, claim intake protocols, notice procedures, and expert mandate templates is the governance discipline that reduces the frequency of avoidable repeat disputes—because most successive disputes within a portfolio share the same root cause, whether that is a wording ambiguity, a notice procedure gap, or an evidence preservation failure, whose identification and remediation after one dispute prevents its recurrence in the next. An English speaking lawyer in Turkey who advises on dispute-informed governance improvement for insurance organizations provides the post-dispute review process that converts each dispute's documentation failures and process gaps into specific template updates and training refreshments whose implementation is confirmed through the next sampling cycle. Practice may vary by authority and year.

Frequently Asked Questions

- What triggers insurer liability in Turkey? Insurer liability arises when the insured proves an insured event within the coverage grant of the final issued policy and the insurer fails to pay, inadequately investigates, or denies on grounds that cannot be supported by the file evidence. The decisive variable is the quality of the documentary record on both sides. Courts test whether the investigation was structured, whether decision letters matched the file, and whether denial grounds were consistent across correspondence. Practice may vary by authority and year.

- What does the insurer duty of good faith Turkey require? Good faith requires the insurer to investigate proportionally, communicate clearly and consistently, avoid arbitrary delay, engage with the insured's exhibits, and document internal approvals for denial decisions. A request log showing proportionality, a decision memo tied to factual findings, and letters consistent with the internal file are the core good faith evidence. Courts assess good faith through the quality of the file rather than through moral characterizations. Practice may vary by authority and year.

- How should a misrepresentation insurance Turkey dispute be defended? The insured should retrieve the full proposal form, broker submission pack, and correction emails showing what was actually disclosed. The insurer must show both that a specific material fact was misstated and that the fact was relevant to risk selection. If the insurer never asked the question in the documented process, the misrepresentation allegation weakens significantly. Contemporaneous delivery proof is essential. Practice may vary by authority and year.

- What is required for policy coverage analysis Turkey? Coverage analysis requires confirming the final issued wording and endorsements for the relevant policy period, mapping each coverage element—trigger, insured property or person, territorial scope, causation requirement—to a specific exhibit, and confirming that the claimant is the named insured or documented beneficiary. Marketing summaries do not govern; courts rely on the contract text. Practice may vary by authority and year.

- How are exclusions applied in insurer liability law Turkey disputes? Exclusions must be applied through the exact issued wording, with each exclusion element mapped to a specific factual exhibit. The insurer cannot rely on an exclusion whose trigger is not proven with evidence. Carve-outs require the insured to prove specific conditions such as suddenness or accidental nature. Ambiguous exclusions may be interpreted against the insurer. Practice may vary by authority and year.

- What are the notice obligation insurance Turkey requirements? Notice obligations require timely written notice to the insurer through the channel specified in the policy, with specific information about the event. The insured should preserve the first notice with delivery proof, document any delay with objective reasons, and keep the insurer's acknowledgment confirming the claim reference. Cooperation after notice requires indexed delivery of requested documents with written acknowledgment. Practice may vary by authority and year.

- How is claims investigation insurer Turkey discipline assessed? Investigation is assessed through the request log—which must show proportionality and relevance—the inspection record, the expert mandates, and whether the insurer engaged with the insured's exhibits. An investigation that ignores decisive evidence or delays without documented reason creates insurer liability exposure. The insured should preserve a parallel chronology showing its own responsiveness. Practice may vary by authority and year.

- What is the adjuster report insurance dispute Turkey standard? Adjuster reports must be signed, dated, and stored with version control. Factual errors must be corrected promptly in writing. The adjuster mandate should be confirmed in writing and tied to specific policy clause elements. The raw data basis for each conclusion must be preserved so conclusions can be verified. If the report is incomplete, the insured should submit a correction letter with an updated exhibit index. Practice may vary by authority and year.

- How does the insurance claim payment obligation Turkey work? Payment obligation arises when coverage is established and the quantum is verified through documented evidence. The insured should request completeness acknowledgment from the insurer and preserve all delivery proofs. If payment is delayed after a complete file, the interest on unpaid insurance claim Turkey argument begins from the point of confirmed completeness. Practice may vary by authority and year.

- How should partial payment disputes be managed in insurance claims? Partial payments should be accompanied by a written allocation showing which heads are accepted and which are disputed with specific reasons. The insured should accept partial payments without prejudice to the balance and document that reservation. Each disputed item should receive an indexed response with supporting exhibits. Practice may vary by authority and year.

- What is required for damages for wrongful denial Turkey insurance claims? Damages beyond the insured amount require strict proof of a causal link between a specific insurer act and a specific documented consequential loss. Each consequential loss must be supported by an external dated document rather than an internal estimate. Interest arguments must demonstrate when the file became decision-ready. Courts are skeptical of broad bad faith labels without exhibit-specific proof. Practice may vary by authority and year.

- How do consumer insurance disputes Turkey and commercial insurance disputes Turkey differ? Consumer disputes involve heightened scrutiny of disclosure clarity and the insured's ability to understand exclusions at contracting. Commercial disputes assume sophisticated parties but still require coherent insurer reasoning. Both settings require indexed file discipline because courts in both contexts evaluate the written documentary record. Classification of policyholder status should be analyzed before choosing forum strategy. Practice may vary by authority and year.

- What is required for insurance litigation Turkey preparation? Insurance litigation requires a petition that separates coverage trigger facts from notice and cooperation facts; attaches the full policy set and endorsement history; includes the denial letter and the claim chronology; proposes narrow expert mandates tied to disputed clause elements; and maintains consistency with all pre-litigation correspondence. Pleadings that contradict earlier complaint letters are treated as credibility failures. Practice may vary by authority and year.

- How is enforcement of insurance judgment Turkey managed? Enforcement requires confirming the correct insurer entity through trade registry records, maintaining a clean calculation sheet separating principal, interest, costs, and partial payments, and submitting to execution offices with accurate debtor identification. Settlement agreements must include clear payment mechanics and proof standards so payment failure allows immediate enforcement without re-litigating facts. Practice may vary by authority and year.

- Does ER&GUN&ER Law Firm provide legal services for insurer liability matters in Turkey? Yes. ER&GUN&ER Law Firm provides legal services for insurer liability matters in Turkey including good faith compliance assessment, investigation record review, disclosure and misrepresentation analysis, coverage grant mapping, exclusion and causation strategy, notice and cooperation compliance documentation, adjuster and expert mandate design, payment obligation analysis, interest and damages framework, denial response preparation, partial payment allocation management, consumer versus commercial classification, insurance litigation preparation and pleadings, burden of proof strategy, enforcement coordination, and parallel recovery planning—with English-language client communication and bilingual documentation throughout each engagement.

Author: Mirkan Topcu is an attorney registered with the Istanbul Bar Association (Istanbul 1st Bar), Bar Registration No: 67874. His practice focuses on cross-border and high-stakes matters where evidence discipline, procedural accuracy, and risk control are decisive.

He advises individuals and companies across Immigration and Residency, Real Estate Law, Tax Law, and cross-border documentation matters where procedural accuracy and evidence discipline are decisive.

Education: Istanbul University Faculty of Law (2018); Galatasaray University, LL.M. (2022). LinkedIn: Profile. Istanbul Bar Association: Official website.