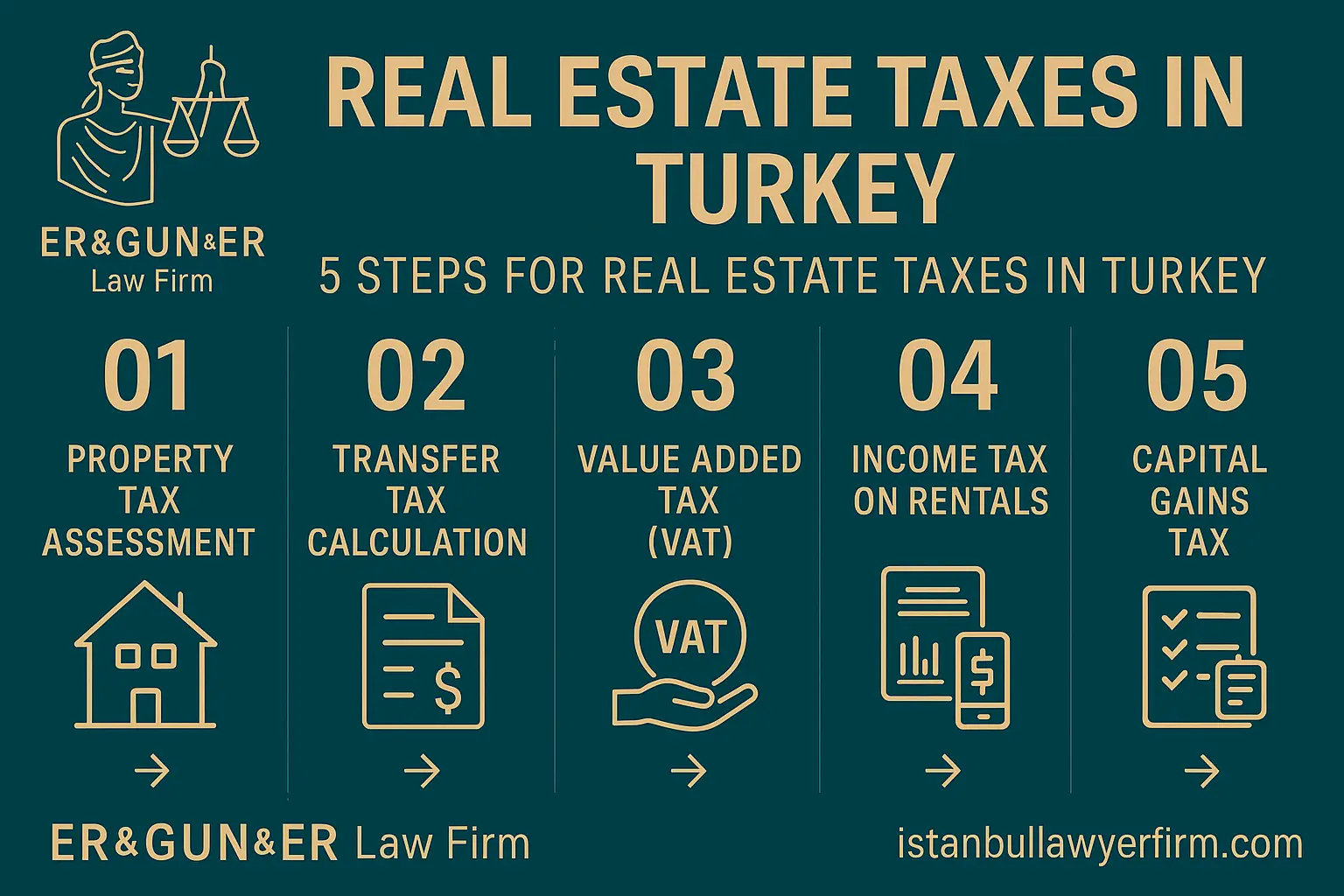

Real estate taxes in Turkey apply at three distinct stages of property ownership: acquisition, ongoing ownership, and disposal—and understanding which taxes apply at each stage, how they are calculated, what exemptions exist, and when they must be paid is essential for any foreign buyer or property owner who wants to manage their Turkish real estate investment without costly surprises. The acquisition stage triggers the title deed transfer fee (tapu harcı) calculated on the declared sale value, and for new residential properties purchased from developers, value added tax (KDV) at rates that vary by property size and value. The ownership stage triggers the annual real estate tax (emlak vergisi) assessed by the municipality on the property's registered tax value, and for properties generating rental income, annual income tax filings on the net rental income at graduated rates. The disposal stage triggers capital gains tax (değer artış kazancı) on the difference between the acquisition cost and the sale price, subject to an important five-year holding period exemption that significantly affects disposal planning. Beyond these main taxes, inheritance and gift tax (veraset ve intikal vergisi) applies when property is transferred by death or gift rather than by arm's length sale. Each of these tax obligations is governed by separate legislation—primarily the Tax Procedure Law (Vergi Usul Kanunu), the Income Tax Law (Gelir Vergisi Kanunu), the Real Estate Tax Law (Emlak Vergisi Kanunu), and the Value Added Tax Law (Katma Değer Vergisi Kanunu)—and is administered by different authorities: the title deed office (tapu dairesi), the municipality (belediye), and the tax office (vergi dairesi). This guide walks through each tax category systematically—applicable rates, calculation methodology, exemptions, filing obligations, and practical compliance steps—addressed to foreign nationals purchasing residential or commercial property in Turkey and to existing property owners managing their ongoing tax position.

Title deed transfer fee (tapu harcı)

A lawyer in Turkey advising on the property acquisition tax Turkey framework must explain that the title deed transfer fee (tapu harcı) is the primary tax cost at the point of purchase and is calculated as a percentage of the declared sale price stated in the title deed transfer deed (tapu senedi). The current rate applies equally to both the buyer and the seller—each party pays their own share at the time of the title deed transfer at the land registry office (Tapu ve Kadastro Müdürlüğü). The combined buyer and seller fee constitutes the total transaction-level tax cost at acquisition. Practice may vary by authority and year — check current guidance on the current tapu harcı rate from the Turkish Revenue Administration (Gelir İdaresi Başkanlığı), accessible at gib.gov.tr, before finalizing any property acquisition budget.

An Istanbul Law Firm advising on the declared sale value dimension must explain that the tapu harcı is assessed on whichever is higher: the declared sale price in the transfer deed or the minimum value set by the municipality (rayiç bedel). Turkish property transactions have historically been conducted with declared values below the actual transaction price—a practice the Turkish tax authorities have consistently targeted through rayiç bedel systems and enhanced scrutiny. A buyer who agrees to declare a value below the actual purchase price to reduce the tapu harcı is participating in a tax compliance risk that can result in additional assessment, penalties, and interest if the underdeclaration is discovered. The real estate due diligence Turkey framework—covering legal and tax verification before purchase—is analyzed in the resource on real estate due diligence for foreigners Turkey. Practice may vary by authority and year — check current guidance on the current Turkish tax authority approach to declared value verification in property transactions.

A Turkish Law Firm advising on the timing and payment mechanics of the tapu harcı must explain that the fee is payable at the land registry office on the day of the title deed transfer—it cannot be deferred, and the title deed transfer will not proceed until the fee payment receipt is presented to the land registry officer. Both parties must be present or represented by a duly authorized attorney (vekil), and the fee must be paid through the designated bank or payment channel accepted by the land registry in advance of the appointment. A foreign buyer who has not budgeted for the tapu harcı as a closing cost will face a practical problem on the day of transfer if the funds are not available in a Turkish bank account in time. Practice may vary by authority and year — check current guidance on the current payment methods accepted at the specific land registry office handling the transaction and on any recently changed payment procedures.

VAT on new property purchases

A law firm in Istanbul advising on the VAT property purchase Turkey rules must explain that value added tax (KDV) applies to the purchase of new residential and commercial properties from developers and construction companies—it does not apply to resale transactions between private individuals. The VAT rate applicable to a residential property purchase depends on the property's net floor area and the construction cost per square meter as certified by the municipality: properties below a certain size threshold and below a certain cost threshold are taxed at a reduced residential rate, while larger or higher-value residential properties and all commercial properties are taxed at the standard rate. Practice may vary by authority and year — check current guidance on the current KDV rate applicable to residential properties in the specific size and cost category of the property you are purchasing, as these rates have been subject to legislative changes and the applicable rate at the time of purchase controls the tax liability.

The VAT exemption for foreign buyers—a significant incentive historically available to foreign nationals who purchase property in Turkey using foreign currency—has been one of the most practically important tax advantages in the Turkish property market for international investors. This exemption, where available, allows qualifying foreign buyers to purchase new properties from developers without paying the KDV that would otherwise be due, provided the purchase price is paid in foreign currency remitted from abroad and the property is not sold within a defined holding period after purchase. The precise conditions for this exemption, including the holding period and the foreign currency transfer documentation requirements, are defined in the VAT Law and its implementing circulars. Practice may vary by authority and year — check current guidance on the current availability and precise conditions of the foreign buyer KDV exemption from the Turkish Revenue Administration before structuring any purchase to rely on this exemption, as the conditions have been amended in recent years and may continue to change.

An English speaking lawyer in Turkey advising on the VAT reclaim scenario—where a qualifying buyer pays VAT at purchase and later becomes entitled to a refund—must explain that the VAT reclaim process for qualifying foreign buyers requires specific documentation: proof of foreign currency remittance from a foreign bank account to the developer's Turkish account, the sale contract, the title deed, and a formal application to the relevant tax office within the applicable time limit. A buyer who paid VAT at purchase because the exemption documentation was not arranged in time may still be able to claim a refund if the underlying conditions for exemption are met—but the refund process is administrative and requires careful documentation management. Practice may vary by authority and year — check current guidance on the current VAT refund procedures for qualifying foreign property buyers and on the specific documentation and time limits applicable to refund applications.

Annual real estate tax (emlak vergisi)

A Turkish Law Firm advising on the annual property tax Turkey framework must explain that the emlak vergisi is an annual municipal tax assessed on the registered tax value (vergi değeri) of real property—land and buildings—payable to the municipality in whose district the property is located. The tax rate differs between property types: residential buildings (konut), commercial buildings (işyeri), and land (arsa/arazi) are taxed at different rates, and properties located in major metropolitan municipalities (büyükşehir belediyesi) face a higher rate than those in smaller municipalities. The tax value on which emlak vergisi is calculated is not the market value or the purchase price—it is a municipally assessed value that is periodically updated and that is typically below market value, particularly for properties that have not been reassessed recently. Practice may vary by authority and year — check current guidance on the current emlak vergisi rates applicable to the specific property type and municipality location and on the current tax value assigned to the specific property from the relevant municipality's records.

A law firm in Istanbul advising on the emlak vergisi payment schedule must explain that the annual tax is divided into two equal installments payable in defined periods each calendar year—the first installment is due in the first half of the year and the second installment in the second half, with the specific payment months set by the municipality in accordance with the Real Estate Tax Law. A property owner who misses an installment deadline faces late payment interest (gecikme faizi) calculated on the overdue amount from the due date, and extended non-payment creates a tax debt that accrues additional penalties and can eventually result in enforcement action by the municipality. Foreign property owners who are not resident in Turkey should specifically arrange a payment mechanism—typically through a Turkish bank account or through a local attorney—to ensure timely payment in their absence. Practice may vary by authority and year — check current guidance on the current emlak vergisi payment periods and on the late payment interest rate currently applicable to overdue municipal property tax.

An English speaking lawyer in Turkey advising on the emlak vergisi exemptions must explain that Turkish law provides specific exemptions from the annual real estate tax for certain property owners and property types. The most significant exemption for foreign buyers is the residential property exemption available to owner-occupiers who own a single residential property below a defined size threshold—where qualifying, this exemption reduces or eliminates the annual tax liability. However, the exemption conditions are specific and must be formally established with the municipality through an exemption application rather than being automatically applied. A foreign property owner who qualifies for an exemption but who has not formally applied will continue to receive annual tax assessment notices and must pay unless and until the exemption is registered. Practice may vary by authority and year — check current guidance on the current emlak vergisi exemption conditions applicable to foreign property owners and on the application procedure for registering the exemption with the relevant municipality.

Rental income tax

A Turkish Law Firm advising on the rental income tax Turkey framework must explain that a foreign national who owns property in Turkey and who receives rental income from that property is subject to Turkish income tax on that rental income—the obligation exists regardless of whether the owner is a Turkish resident or a non-resident, because the source of the income is in Turkey. The rental income is reported on an annual income tax declaration (yıllık gelir vergisi beyannamesi) filed with the tax office in the district where the property is located, covering the income earned in the previous calendar year, with the declaration deadline and payment schedule set by the Income Tax Law. Practice may vary by authority and year — check current guidance on the current declaration deadline for rental income from Turkish property and on the current income tax rates applicable to rental income declared by non-resident foreign property owners.

A law firm in Istanbul advising on the net rental income calculation—specifically, which expenses can be deducted from gross rental income to arrive at the taxable base—must explain that Turkish income tax law allows property owners to deduct certain expenses from their gross rental income. The two deduction methods available are: the actual expense method (gerçek gider yöntemi), which allows deduction of documented actual expenses including mortgage interest, maintenance costs, insurance, depreciation, and management fees; and the flat-rate deduction method (götürü gider yöntemi), which allows a fixed percentage deduction from gross rental income without requiring documentation of individual expenses. The flat-rate method is simpler to apply but may not capture the full value of actual expenses where those are high; the actual expense method requires expense documentation but may produce a lower tax liability where expenses are substantial. Practice may vary by authority and year — check current guidance on the current flat-rate deduction percentage applicable to rental income and on any recently changed rules regarding deductible expense categories under the actual expense method.

An English speaking lawyer in Turkey advising on the rental income exemption threshold—the annual rental income amount below which no declaration obligation exists—must explain that Turkish income tax law provides a minimum exemption amount for rental income from residential properties: rental income below this threshold in a given year is exempt from income tax and does not require a tax declaration. The exemption amount is updated annually by the Turkish government to reflect cost of living changes. A foreign property owner whose Turkish rental income for the year falls below the current threshold has no filing obligation for that year—but a property owner whose income exceeds the threshold must file even if the taxable income after deductions would be zero. Practice may vary by authority and year — check the current annual exemption amount for residential rental income in Turkey from the Turkish Revenue Administration before determining your filing obligation for the current or previous year.

Capital gains tax on property sales

A Turkish Law Firm advising on the capital gains tax property Turkey framework must explain that profit made on the sale of Turkish real property is subject to income tax on the capital gain—calculated as the difference between the inflation-adjusted acquisition cost and the sale price. However, the most important planning variable in the capital gains analysis is the five-year holding period rule: property held for more than five full years from the date of acquisition is fully exempt from capital gains tax regardless of the amount of profit realized. This five-year exemption is not a reduced rate or a partial relief—it is a complete exemption from tax liability on the gain, making it one of the most valuable tax planning tools available in the Turkish real estate market. Practice may vary by authority and year — check current guidance on the current five-year holding period rule and on how the acquisition date is determined for properties purchased under construction or through title deed procedures involving multiple steps.

A law firm in Istanbul advising on the capital gains calculation methodology for properties sold within the five-year holding period must explain that the taxable gain is not simply the difference between the nominal purchase price and the nominal sale price—Turkish tax law applies an inflation adjustment (enflasyon düzeltmesi) to the acquisition cost using the producer price index (ÜFE), which increases the effective acquisition cost to reflect inflation between the purchase date and the sale date. For properties purchased in periods of high inflation—such as Turkey's recent inflationary environment—this adjustment can significantly reduce the nominal gain and therefore the tax liability. A property owner who calculates their gain without applying the inflation adjustment will significantly overestimate their tax liability. Practice may vary by authority and year — check current guidance on the current inflation adjustment methodology and on whether the ÜFE-based adjustment currently applies to property capital gains in the same form as historically or whether amendments have changed the calculation approach.

An English speaking lawyer in Turkey advising on the capital gains tax rate and filing obligation must explain that capital gain from property sale within the five-year holding period is reported as part of the property owner's annual income tax declaration and is taxed at the graduated income tax rates applicable to the total taxable income in that year—the gain is added to any other Turkish income the individual has and taxed at the marginal rate applicable to the combined income. The tax declaration for a capital gain from a property sale in one calendar year is due in the following year by the declaration deadline. A property owner who sells Turkish real estate must plan for this filing obligation even if they have departed Turkey by the time the declaration is due. The tax law Turkey framework—covering the broader Turkish income tax compliance picture—is analyzed in the resource on tax law Turkey. Practice may vary by authority and year — check current guidance on the current graduated income tax rates and on the specific capital gains declaration procedures applicable to non-resident foreign property sellers.

Inheritance and gift tax on property

A Turkish Law Firm advising on the inheritance tax property Turkey framework must explain that the transfer of Turkish real property through inheritance (veraset) or gift (intikal) triggers inheritance and gift tax (veraset ve intikal vergisi) assessed on the value of the property transferred. The tax is payable by the recipient—the heir or the gift recipient—rather than by the estate or the donor. The tax rates are graduated based on the value of the property received and are different for inheritance transfers and gift transfers, with gift transfers taxed at higher rates than inheritance transfers between family members. Practice may vary by authority and year — check current guidance on the current inheritance and gift tax rate schedule from the Turkish Revenue Administration and on the current valuation methodology applied to Turkish real property for inheritance and gift tax purposes.

A law firm in Istanbul advising on the inheritance tax exemptions must explain that Turkish inheritance and gift tax law provides specific exemptions and reduced rates for transfers between close family members—spouses, children, and parents—that can significantly reduce the tax burden on standard family property inheritance. The exemption amounts are updated periodically and must be verified against the current legislation rather than assumed from historical figures. A foreign heir who inherits Turkish property and who is unaware of the applicable exemptions may pay more than the legally required amount or may fail to file the required declaration within the statutory deadline, creating penalty exposure. The inheritance law Turkey framework—covering the complete picture of property inheritance for foreign heirs—is analyzed in the resource on inheritance law Turkey. Practice may vary by authority and year — check current guidance on the current inheritance tax exemption amounts applicable to transfers between specific family member categories.

An English speaking lawyer in Turkey advising on the inheritance tax declaration and payment obligation for foreign heirs must explain that foreign nationals who inherit Turkish real property must file an inheritance tax declaration with the Turkish tax office and pay the assessed tax—the obligation exists regardless of whether the heir is a Turkish resident or a non-resident living abroad. The declaration must be filed within a defined period after the date of death, and the tax is typically payable in installments over a period of years. A foreign heir who is unaware of this obligation and who fails to file on time faces penalties and late payment interest in addition to the underlying tax. Coordinating the inheritance tax compliance with the probate and title deed transfer process—which have their own procedures and timelines—requires careful planning. Practice may vary by authority and year — check current guidance on the current declaration deadline for inheritance tax following the death of a Turkish property owner and on the installment payment schedule applicable to the assessed tax.

Tax exemptions for foreign buyers

A Turkish Law Firm advising on the real estate tax exemptions Turkey available specifically to foreign buyers must explain that Turkey has historically used property tax incentives as part of its strategy to attract foreign real estate investment, and several exemptions have been available that reduce the effective tax cost of Turkish property acquisition and ownership for qualifying foreign nationals. These exemptions are not permanent features of the Turkish tax system—they are legislative choices that have been introduced, modified, and in some cases narrowed over time—and a foreign buyer who plans their purchase around an exemption that has since been amended or eliminated faces an unexpected tax liability. The current availability and precise conditions of each exemption must be verified from current official sources rather than from broker representations or community information. Practice may vary by authority and year — check current guidance on each exemption category directly from the Turkish Revenue Administration before structuring any transaction to rely on an exemption.

A law firm in Istanbul advising on the KDV exemption for foreign buyers—the VAT exemption discussed in the acquisition section—must reiterate that this exemption requires a specific factual pattern to qualify: the buyer must be a foreign national not resident in Turkey for tax purposes, the purchase must be from a VAT-registered developer or company rather than from a private individual, the price must be paid in foreign currency transferred from a foreign bank account, and the property must be held for the defined minimum period after purchase before sale. A buyer who meets all of these conditions and who properly documents the foreign currency transfer at the time of purchase can claim the exemption either at the point of sale (paying no VAT to the developer) or through a subsequent refund application. A buyer who does not meet all conditions does not qualify regardless of their general status as a foreigner. Practice may vary by authority and year — check current guidance on the current eligibility conditions and documentation requirements for the foreign buyer KDV exemption from the Turkish Revenue Administration.

An English speaking lawyer in Turkey advising on the citizenship-by-investment dimension—where a foreign national purchases property specifically to qualify for Turkish citizenship through the investment threshold—must explain that the tax obligations on a citizenship-qualifying property purchase are identical to those on any other property purchase. The citizenship-by-investment pathway does not create additional tax exemptions or preferential rates. However, the investment threshold requirement—which sets a minimum declared property value for citizenship qualification purposes—interacts with the tapu harcı calculation in a way that must be specifically managed: the declared property value in the title deed must meet the citizenship investment threshold, which means it must accurately reflect the actual transaction price, removing any possibility of value underdeclaration at this stage. The Turkish citizenship by investment framework is analyzed in the resource on Turkish citizenship by investment. Practice may vary by authority and year — check current guidance on the current citizenship investment threshold and on the tax implications of declaring the full investment value in the title deed.

Tax obligations for non-resident owners

A Turkish Law Firm advising on the tax obligations of non-resident foreign property owners must explain that Turkish tax law taxes non-residents on their Turkish-source income—meaning that a foreign national who does not reside in Turkey but who owns Turkish property and receives rental income is subject to Turkish income tax on that rental income, and a foreign national who sells Turkish property within the five-year holding period is subject to Turkish capital gains tax on the gain. The annual real estate tax (emlak vergisi) applies to all property owners regardless of residency. Non-residency does not exempt a foreign national from Turkish property-related taxes—it simply means that only the Turkish-source income is subject to Turkish tax rather than the individual's worldwide income. Practice may vary by authority and year — check current guidance on the current Turkish tax authority's enforcement approach toward non-resident foreign property owners who have not complied with their Turkish filing and payment obligations.

A law firm in Istanbul advising on the double taxation treaty dimension must explain that Turkey has concluded double taxation avoidance agreements (çifte vergilendirmeyi önleme anlaşmaları) with a significant number of countries, and these treaties may affect whether a specific Turkish tax liability can be offset against a tax liability in the foreign owner's country of residence. The treaty provisions applicable to real property income—rental income and capital gains from immovable property—generally allocate the primary taxing right to the country where the property is located (Turkey), meaning that the treaty typically does not eliminate Turkish tax on Turkish property income but may provide relief against double taxation in the owner's country of residence. The double taxation treaty Turkey framework is analyzed in the resource on double taxation treaty Turkey. Practice may vary by authority and year — check current guidance on the specific double taxation treaty provisions applicable between Turkey and the foreign owner's country of residence.

An English speaking lawyer in Turkey advising on the Turkish tax number (vergi kimlik numarası) requirement for non-resident property owners must explain that every foreign national who owns property in Turkey, receives rental income, or completes a property transaction must hold a Turkish tax identification number. This number is obtained from any Turkish tax office with a passport and is issued immediately and free of charge—it is not a complex procedure. However, a foreign national who has not yet obtained a Turkish tax number and who is attempting to complete a title deed transfer, open a Turkish bank account for rental income collection, or file a tax return will find that the tax number is a prerequisite for each of these steps. Obtaining the tax number before any property transaction—ideally at the earliest stage of the purchase process—eliminates a common last-minute obstacle. Practice may vary by authority and year — check current guidance on the current Turkish tax number application procedure for foreign nationals and on any identification documents required beyond the passport.

Short-term rental tax compliance

A Turkish Law Firm advising on the tax obligations of foreign property owners operating short-term rentals through platforms such as Airbnb, Booking.com, or similar channels must explain that short-term rental income is subject to Turkish income tax on exactly the same basis as long-term rental income—the source of the income is Turkey, and the income tax obligation exists regardless of the platform used, the currency received, or whether the owner has a Turkish presence or bank account. A foreign property owner who collects short-term rental income through a foreign platform and who does not declare this income to the Turkish tax authority is in non-compliance with Turkish tax law. The Turkish Revenue Administration has increasingly focused enforcement resources on identifying undeclared short-term rental income, including through data exchange with rental platforms. Practice may vary by authority and year — check current guidance on the current Turkish tax authority enforcement approach to short-term rental income and on any recently enacted platform reporting obligations that may affect income disclosure for properties rented through digital platforms.

The short-term rental regulatory framework—beyond the tax dimension—requires foreign property owners operating short-term rentals to comply with the Turkish short-term rental permit system introduced in recent years, which requires registration of the property for short-term rental use and compliance with specific building and homeowners' association consent requirements. A property operated as a short-term rental without the required permit is exposed to administrative fines and potentially to rental prohibition orders in addition to the underlying tax compliance obligations. The short-term rental compliance Turkey framework is analyzed in the resource on short-term rental compliance Turkey. Practice may vary by authority and year — check current guidance on the current short-term rental permit system and on the tax reporting obligations specifically applicable to permitted short-term rental operations.

A law firm in Istanbul advising on the VAT implications of commercial short-term rental operations must explain that where a foreign property owner's short-term rental activity exceeds the threshold for commercial business activity under Turkish tax law—because of the frequency, scale, or commercial nature of the operations—the activity may be reclassified from passive rental income to active commercial income, triggering different tax treatment and potentially VAT registration and collection obligations. A foreign national who owns multiple properties in Turkey and who operates them systematically as short-term rentals should specifically assess whether their activities constitute a commercial operation under Turkish tax standards rather than assuming that all rental income is treated as personal property income. Practice may vary by authority and year — check current guidance on the current Turkish tax authority's threshold and criteria for reclassifying property rental income as commercial business income and on the VAT implications of commercial rental operations by foreign nationals.

Tax planning and structuring

An English speaking lawyer in Turkey advising on tax planning for Turkish real estate investments must explain that the most impactful tax planning decisions for Turkish property are made at the acquisition stage—because the choices made at purchase determine the tax position at all subsequent stages. The acquisition structure (individual ownership versus Turkish company ownership), the declaration methodology (declared value management within compliant boundaries), the VAT exemption eligibility assessment, and the holding period planning for the five-year capital gains exemption are all elements that should be analyzed before the purchase contract is signed rather than after. A foreign buyer who acquires Turkish property without a tax planning analysis and who later discovers that a different structure or timing would have produced a significantly better tax outcome has missed an opportunity that cannot be retroactively recovered in most cases. Practice may vary by authority and year — check current guidance from a qualified Turkish tax advisor on the current tax-optimal acquisition structure for the specific property type, value, and intended use before completing any purchase.

A Turkish Law Firm advising on the Turkish company ownership structure—where a foreign investor purchases Turkish property through a Turkish limited company (limited şirket) or joint stock company (anonim şirket) rather than in their personal name—must explain that company ownership creates a different tax profile than individual ownership: the company is subject to corporate income tax on rental income at the flat corporate rate rather than at the graduated personal income rate; the five-year capital gains exemption does not apply to corporate property sales in the same way as to personal sales; the annual emlak vergisi applies at the commercial property rate if the company uses the property commercially; and dividend distributions from the company to the foreign individual shareholder may be subject to withholding tax. Company ownership can be advantageous for investors with significant portfolios and commercial operations, but it adds administrative complexity and ongoing compliance costs that must be weighed against the tax benefits for each specific situation. Practice may vary by authority and year — check current guidance on the current corporate tax rates and on the specific tax implications of Turkish company ownership of real property for foreign shareholders.

A best lawyer in Turkey completing the tax planning framework must address the real estate tax lawyer Turkey engagement question—when qualified Turkish tax counsel is essential versus when self-managed compliance is sufficient. For a foreign buyer purchasing a single residential property below a moderate value, holding it for personal use or simple long-term rental, and planning to hold it for more than five years before any sale, the tax obligations are relatively straightforward: tapu harcı at purchase (paid at the land registry), annual emlak vergisi (payable to the municipality), and rental income declaration if applicable (filed annually with the tax office). These can be managed with basic knowledge of the system and a Turkish accountant's assistance for the annual declarations. For transactions involving commercial properties, multiple properties, short-term rental operations, citizenship-by-investment structures, company ownership, inheritance planning, or disposals within the five-year capital gains window, qualified Turkish tax and legal counsel is essential. The Istanbul Bar Association at istanbulbarosu.org.tr provides resources for identifying qualified practitioners. Practice may vary by authority and year — check current guidance on all applicable tax rates, exemptions, and filing deadlines from the Turkish Revenue Administration before completing any property transaction or filing any property-related tax declaration in Turkey.

Practical compliance roadmap

Turkish lawyers developing a practical property tax compliance roadmap for foreign buyers must structure the obligations by stage. At the acquisition stage: obtain a Turkish tax identification number before the purchase contract is signed; verify bilateral KDV exemption eligibility if purchasing from a developer; budget for the tapu harcı as a closing cost payable on the day of title deed transfer; ensure the declared sale value in the title deed accurately reflects the transaction value; and obtain professional guidance on whether the foreign buyer KDV exemption conditions are met if purchasing a new property. At the ownership stage: register the property with the municipality for emlak vergisi assessment within the legally required period after title deed transfer; verify whether any emlak vergisi exemption applies and formally apply for it with the municipality; arrange a payment mechanism for the annual two-installment emlak vergisi if you will not be residing in Turkey; and establish a tax filing arrangement for annual rental income declarations if the property generates rental income. At the disposal stage: calculate whether the five-year holding period exemption applies before agreeing a sale; if selling within five years, obtain a calculation of the inflation-adjusted capital gain and the resulting tax liability before agreeing to the price; ensure the capital gains tax declaration is filed by the applicable deadline in the year following the sale; and assess the interaction with any double taxation treaty applicable to your country of residence. Practice may vary by authority and year — check current guidance on each obligation from the Turkish Revenue Administration and the relevant municipality before acting on this roadmap for a specific transaction.

The record-keeping obligation is the most commonly overlooked compliance requirement among foreign property owners. Turkish income tax declarations for rental income require documentation of income received and expenses claimed; the capital gains calculation requires the original purchase price documentation and proof of the acquisition date; and inheritance tax declarations require valuation documentation for the property at the date of death. A foreign property owner who does not maintain organized records of their Turkish property transactions—purchase contracts, title deeds, payment receipts, bank transfer records, rental income receipts, and expense invoices—will face significant practical difficulty in fulfilling these documentation requirements when the time comes. Establishing a simple filing system for Turkish property documents at the point of purchase rather than retrospectively saves substantial time and professional fees. The tax residency foreigners Turkey framework—relevant for owners who subsequently establish Turkish tax residency—is analyzed in the resource on tax residency foreigners Turkey. Practice may vary by authority and year — check current guidance on the current Turkish tax authority documentation requirements for each tax obligation covered in this guide.

A law firm in Istanbul completing the compliance roadmap must address the interaction between property tax compliance and Turkish banking. Most Turkish property tax payments—tapu harcı, emlak vergisi, income tax, and inheritance tax—must be made through Turkish banking channels rather than from foreign accounts. A foreign property owner who does not have a Turkish bank account faces practical payment obstacles that are best resolved before the first payment obligation arises rather than at the deadline. Opening a Turkish bank account for property-related payments is straightforward for foreign nationals holding a residence permit and a Turkish tax number, and for non-resident foreign property owners, certain Turkish banks offer non-resident account facilities. The property investment Turkey framework—covering the complete legal and financial picture of foreign property ownership—is analyzed in the resource on real estate law Turkey. Practice may vary by authority and year — check current guidance on the current Turkish bank account opening requirements for non-resident foreign property owners and on the payment methods currently accepted by each tax authority for the specific taxes applicable to your property situation.

Author: Mirkan Topcu is an attorney registered with the Istanbul Bar Association (Istanbul 1st Bar), Bar Registration No: 67874. His practice focuses on cross-border and high-stakes matters where evidence discipline, procedural accuracy, and risk control are decisive.

He advises individuals and companies across Real Estate Law, Tax Law, Commercial and Corporate Law, and cross-border documentation matters where procedural accuracy and evidence discipline are decisive.

Education: Istanbul University Faculty of Law (2018); Galatasaray University, LL.M. (2022). LinkedIn: Profile. Istanbul Bar Association: Official website.