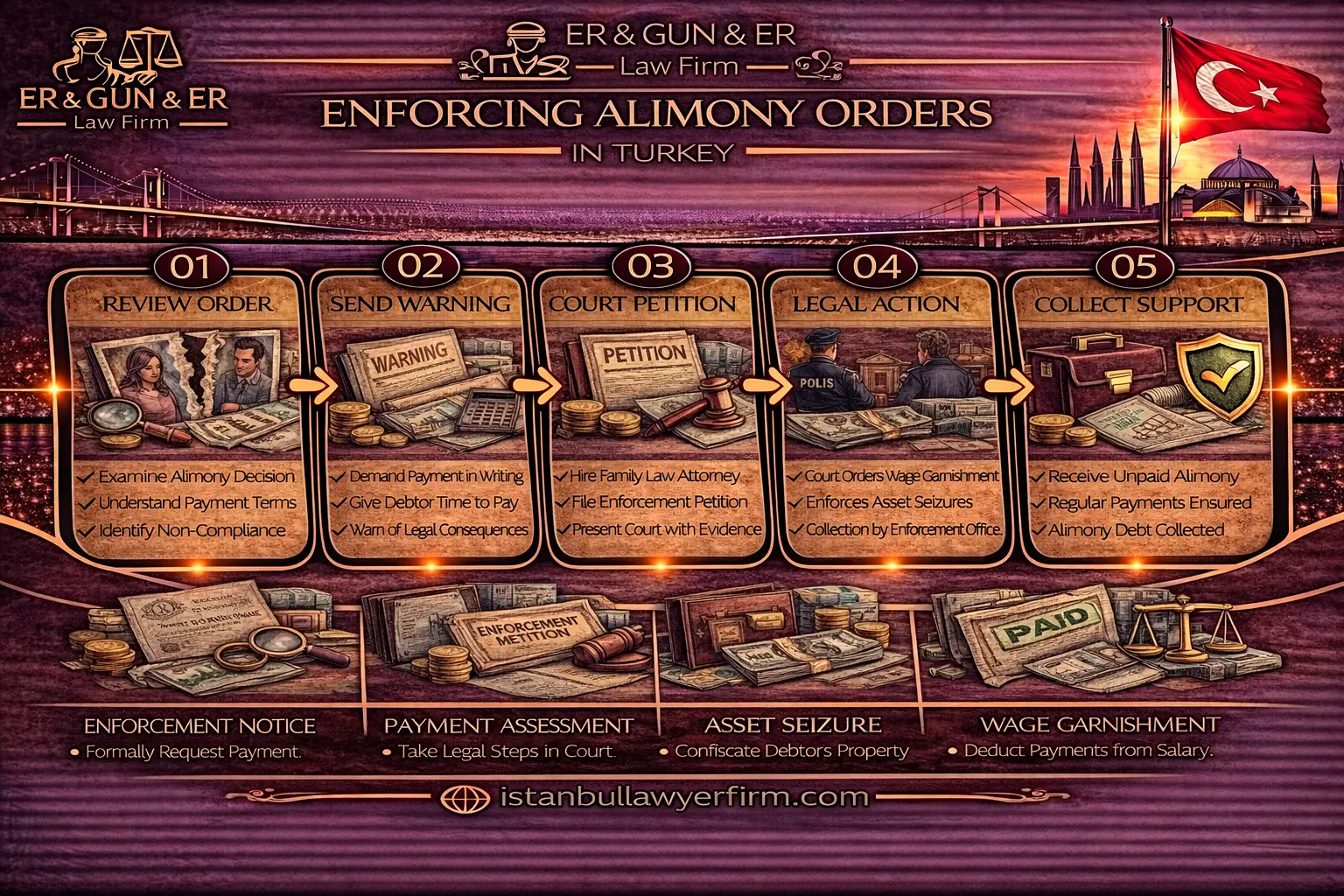

Enforcing alimony is often separate from the divorce merits because collection runs through execution offices and proof files. An enforceable title is the written document that authorizes the execution office to act, usually a court judgment or a court-approved protocol. Once you have a title, the main question becomes whether non-payment is provable through statements, receipts, and a clear arrears schedule. Many parties discover late that messaging and verbal promises do not replace documentary proof, especially when the payer disputes months and amounts. This is why enforcing alimony orders Turkey is fundamentally an evidence and procedure exercise rather than a negotiation exercise. Alimony enforcement Turkey also intersects with payroll and banking systems, so identifying employer and bank targets early reduces delay. “practice may vary by authority and year — check current guidance.” If the record is complex or bilingual, coordinating the file with lawyer in Turkey counsel can prevent technical errors that later trigger objections.

Enforceable alimony titles

An alimony order is enforceable only when you hold an enforceable title issued or approved by a competent authority. In practice this title is usually a final family court judgment or a settlement protocol that the court recorded and approved. Some interim decisions can also be enforceable while the main case continues, but the paperwork must show the interim nature clearly. The execution office does not re-litigate whether alimony is fair, and it focuses on what the written title orders. You therefore start by obtaining a clean copy of the judgment page that states the monthly amount and the payment start point. You also obtain the decision’s identification details so the execution office can open the correct enforcement file. If the order includes both spouse maintenance and child-related payments, the title should show each component distinctly. Where the order references future indexation or adjustments, the wording should be read carefully before any calculation is made. If the order is vague, enforcement becomes slower because the execution office may ask for clarification documents. A cautious creditor therefore asks the court registry for a certified copy where needed and keeps it in the enforcement binder. If the alimony is recorded in a court-approved settlement, the signed protocol should be attached as part of the title set. If the protocol references other documents, those referenced pages should also be collected so nothing appears missing. The enforcement logic under the Execution and Bankruptcy Law is document-led, and missing pages create avoidable objections. For this reason, enforcing alimony orders Turkey begins with a title audit rather than with messages to the debtor. Once the title is clean, you can move to execution proceedings for alimony Turkey with less procedural friction.

Not every payment label in a divorce file is automatically enforceable as alimony, so the first step is to confirm the legal nature of the obligation. A family court may order different support types, and the execution office will enforce only what is written as a clear payment obligation. If you are unsure how a particular support item is classified, the background at alimony law guidance can help you map terminology to enforceable content. Court minutes, interim hearing notes, and informal undertakings are usually weak substitutes for a formal enforceable title. Where a spouse promised to pay voluntarily, you still need a formal title if you want execution tools against bank accounts and salaries. The most common enforceable titles contain a monthly amount, a payee identity, and a clear instruction that the debtor must pay periodically. If the order includes arrears, the order should show the arrears period or a method to calculate it. If the order is silent on arrears, enforcement will typically proceed on the amounts that can be calculated from the monthly obligation and the dates proven. A creditor should also check whether the title was later modified, because enforcing an outdated amount creates unnecessary objections. If a modification exists, collect both the older order and the newer order and label them clearly in the binder. For evidence of non-payment alimony Turkey, the core documents are bank statements and payment receipts that show what was paid and what was not paid. A practical file therefore includes a payment ledger that reconciles each due month with an incoming transfer or a recorded missing amount. The ledger is not the proof by itself, but it helps the execution office and later the court see the chronology without re-reading every statement. Many creditors bring this file discipline to counsel early, and a law firm in Istanbul can coordinate indexing so the case stays document-led. A clean title set and a clean payment ledger together reduce the chance that the debtor reframes the dispute as a merits argument.

Before filing, confirm that the title is readable and that the debtor’s identity details match the information you will use in the execution request. If the debtor has multiple names or different spellings in different documents, prepare a reconciliation note supported by identity copies. If the debtor is a foreign national, include passport copies where available so service and identification are not delayed. If the alimony was ordered in a combined divorce judgment, extract the specific pages that set out the alimony obligation and annex them as the enforceable portion. Keep the full judgment archived, but submit a focused bundle so the execution office can verify the operative wording quickly. Where the order includes a child component, ensure you also keep the child’s identity documentation available because some offices ask for clarity. If payments were partly made in cash, collect any signed receipts and keep them in chronological order to avoid later disputes about double counting. If payments were made through third-party accounts, document the relationship and preserve the payment references so the office can match inflows. A prudent creditor also checks whether the debtor has appealed or obtained any stay that affects execution posture. You should not assume a stay exists or does not exist, and you should verify the current procedural status from official records. A short cover note that lists what is being enforced and which months are unpaid often helps keep the file focused. This is where alimony enforcement Turkey becomes a matter of precision rather than emotion, because execution is a technical process. If the debtor threatens to challenge the file, do not respond with messages and instead preserve communications as potential exhibits. Many families prefer to work with best lawyer in Turkey profiles when the file is high value because one mistake in the title bundle can cost months. The practical goal at this stage is to enter enforcement with a clean proof spine so later objections can be answered quickly.

When enforcement can start

Enforcement usually starts when an installment becomes due and remains unpaid, because execution is driven by arrears. The title typically states the payment frequency, and the creditor proves which installments are unpaid by statements and receipts. In some files, the order is interim and continues until final judgment, but the paperwork must show the interim nature clearly. If a final judgment replaces an interim order, you should determine which months are governed by which order and label them in the ledger. A common mistake is to demand amounts for months that were not yet due or months covered by a different order. That mistake invites objections and can delay collection even when the core obligation is undisputed. The execution office generally expects a clear arrears calculation that can be checked against the judgment wording. For that reason, you should prepare a month-by-month table that references the due month and the payment evidence for each month. Do not guess interest or penalties in this table, and instead separate principal arrears from any later calculations. If the debtor made partial payments, record the partial payments with dates and amounts to prevent later double-collection claims. If the debtor paid directly in cash, preserve signed receipts and identify which month each receipt covers. If the debtor claims that payment was made by a third party, preserve the bank reference and the identity link to avoid confusion. When people ask about unpaid alimony consequences Turkey, they often focus on punishment, but the first practical step is document-based execution. Many Turkish lawyers advise starting execution promptly after arrears accumulate because delay increases tracing difficulty and increases bargaining games. “practice may vary by authority and year — check current guidance.”

Enforcement timing is also influenced by whether the order is framed as a monthly ongoing duty or as a lump sum arrears duty. Where the order is ongoing, each missed month becomes a new arrears item that can be added to the enforcement file. Some creditors prefer to open enforcement quickly and then update the file with new months as they fall due. Other creditors prefer to wait until a meaningful arrears balance exists, but waiting can increase collection risk if assets move. A careful strategy is to balance administrative cost against dissipation risk and the debtor’s payment behavior pattern. If the debtor has a stable salary, early filing can support a steady garnishment track once service is completed. If the debtor is self-employed, early filing can support early bank attachment attempts before accounts are emptied. If the debtor is abroad or frequently traveling, service and identification steps can take longer and should be planned early. Where the title was issued in a settlement protocol, confirm that signatures and court approval pages are complete before filing. If a child support component exists, separate it in the ledger so later disputes do not confuse spousal alimony and child-related payments. If you expect parallel custody or property disputes, keep communications disciplined so enforcement does not become a bargaining weapon. In bilingual families, a structured explanation memo can help the debtor understand the arrears schedule without escalating conflict. This is one reason parties sometimes involve English speaking lawyer in Turkey counsel to maintain calm, precise correspondence and clean exhibits. The safest rule is that enforcement starts from an enforceable title and a provable non-payment record, not from informal promises. “practice may vary by authority and year — check current guidance.”

When alimony is ordered during a divorce, enforcement is often procedurally separate from the divorce merits file. The divorce file decides entitlement and amount, while the execution file collects arrears through enforcement tools. This separation matters because a creditor can pursue collection even while other divorce-related disputes continue. It also matters because the execution office will not re-evaluate the fairness of the order and will focus on the written command. A creditor should therefore avoid filing emotional complaints to the execution office and instead submit documents that prove arrears. A debtor who disputes the amount should use the procedural objection path rather than informal negotiation at the execution desk. If the debtor claims that circumstances changed, the correct route is usually a modification action in family court, not refusal to pay. Until a modification decision exists, the execution office typically treats the existing title as binding for collection steps. Where payments are made irregularly, the creditor should allocate each payment to specific months and keep a clear allocation rule. Where the debtor pays directly to third parties, such as paying school fees, treat those payments carefully and do not assume they offset alimony without clear agreement. If the parties agree on offsets, put the agreement in writing and keep it as an exhibit to avoid later disputes. If the debtor pays by cash, request signed receipts because cash without receipts creates endless disputes about what was paid. If the debtor uses different bank accounts, keep the incoming references and bank statements so each transfer is traceable. A disciplined start date strategy also reduces later enforcement friction because the file remains consistent when new months are added. “practice may vary by authority and year — check current guidance.”

Execution office filing steps

Filing begins by choosing the correct execution office based on the debtor’s address, assets, or the office’s competence rules. The creditor prepares an enforcement request that identifies the enforceable title and the arrears amount claimed. The request must include the debtor’s identity details so service can be completed without ambiguity. The request should attach the judgment or approved protocol pages that contain the alimony obligation wording. If the obligation is monthly, the request should also include an arrears schedule that lists each month and whether payment was received. The schedule should be supported by bank statements and receipts, not only by a spreadsheet. Where partial payments were made, the schedule should show allocation to specific months to prevent later double counting. The creditor should also prepare a service address package, because incorrect address information causes long delays. If the debtor is employed, the creditor should prepare employer information for later garnishment notices. If the debtor is self-employed, the creditor should prepare bank and registry targets for later attachment steps. If the debtor has real estate, the creditor should prepare land registry identifiers for annotation requests. The enforcement office will open a file and issue the payment order based on the submitted title and schedule. The creditor should keep a copy of every submitted page and every receipt because later objections rely on this record. A well-prepared file reduces back-and-forth at the desk and shortens the path into execution proceedings for alimony Turkey. “practice may vary by authority and year — check current guidance.”

After filing, the execution office serves the payment order and records the service date in the file. Service date matters because later steps often refer to when the debtor was formally notified of the claim. The creditor should obtain the service proof and store it as a separate exhibit in the enforcement binder. If service fails, the creditor should correct the address quickly and request re-service without rewriting the claim. Once service is complete, the office will proceed according to the procedural track applicable to judgment based claims. The creditor should avoid informal communication with the debtor that contradicts the enforcement schedule, because contradictions become objections. If the debtor wants to pay voluntarily, the debtor should be directed to pay through traceable channels and to provide payment proof. Payment proof should be attached to the file and the arrears schedule should be updated as a dated supplement. If the debtor pays only part, the creditor should confirm in writing which months were covered and keep that confirmation. If the debtor pays in cash, insist on a signed receipt and then scan it into the file immediately. If the creditor needs a conceptual overview of how execution files move, this enforcement procedures guide can help explain the sequence without replacing case-specific planning. The creditor should also plan early which assets are reachable, salary, bank accounts, or registrable assets, because each requires different notices. In alimony enforcement Turkey, the practical friction often comes from missing service proofs and unclear month allocation, so focus on those first. Keep communications calm and factual so any later court review sees procedural discipline rather than escalation. “practice may vary by authority and year — check current guidance.”

The creditor should maintain a file map that separates the title, the arrears schedule, the service proofs, and the attachment requests. This file map matters because execution offices and later courts often ask for a specific page and do not search the whole file. A practical file map begins with an index page and then uses consistent exhibit numbering across every supplement. Every time the creditor files a supplement, the supplement should be labeled by date and the index should be updated. If the creditor changes banks or changes the payee account, that change should be recorded so payment receipts remain consistent. If the debtor changes employer, the creditor should update the employer information quickly to avoid misdirected garnishment notices. If the debtor changes address, the creditor should obtain updated address evidence because service and notices depend on it. The creditor should also keep a communication log that records settlement offers and responses without mixing them into the court record. When the case is high conflict, a single communication channel reduces misunderstandings and reduces unnecessary objections. If the parties negotiate a payment plan, the plan should be documented and then reflected in the execution file so enforcement steps are aligned. If the plan fails, the creditor can resume enforcement with clearer proof of noncompliance under the plan. In practice, many creditors prefer to have one custodian manage these steps because it reduces document loss and inconsistent updates. This is why some families instruct Istanbul Law Firm teams to centralize the execution binder and the supplement log. Central custody does not change the debtor’s obligation, but it improves the creditor’s ability to respond quickly to procedural questions. “practice may vary by authority and year — check current guidance.”

Interest and accrual issues

Interest questions arise when arrears accumulate and the creditor seeks compensation for delay. The phrase interest on unpaid alimony Turkey is often raised, but the correct approach is to follow the title wording and the applicable execution rules without guessing rates. Some titles specify how interest is treated, while others are silent and require application of general enforcement principles. The creditor should therefore read the judgment carefully and identify whether it orders interest explicitly or leaves it to general law. Where interest is claimed, the creditor should separate principal arrears from any interest calculation in the arrears schedule. This separation helps because debtors often object to arithmetic and the court prefers transparent schedules. A transparent schedule lists each missed installment, the date it became due, and the payment history for that installment. The schedule then states that interest is claimed from the legally applicable point without inserting a speculative percentage. If the debtor made partial payments, allocation rules affect what portion of the principal remains outstanding, and that affects interest logic. If the debtor paid late for some months, record late payments by date so the office can see that delay is proven. If the debtor claims that the parties agreed to waive interest, the waiver should be proven by a written agreement, not by memory. If the creditor accepted reduced payments, document whether acceptance was conditional or final so later disputes do not arise. In contentious files, Turkish Law Firm can help prepare a calculation method note that is conservative and evidence-led. “practice may vary by authority and year — check current guidance.” The practical aim is to keep the interest discussion procedural and document-based rather than emotional.

Accrual issues also include deciding how to treat months that are partly paid and months that are fully unpaid. A creditor should avoid rolling different months into one lump sum without showing the month breakdown. Month breakdown matters because execution files often distinguish recurring obligations from one-time obligations. A recurring obligation can generate new installments during the case, and the file must be updated without losing the older record. For that reason, a creditor should maintain a running ledger that is updated only by supplements, not by overwriting old numbers. Each ledger update should state what was newly added and what was newly paid, with dates and payment references. If the debtor paid directly to a child’s expense, record the payment but do not assume it offsets alimony unless the title or a written agreement permits it. If the debtor paid through a third party, record the third-party identity and preserve the bank reference to avoid confusion. If the debtor claims that the amount was reduced informally, ask for written proof and keep the demand as an exhibit. Courts and execution offices typically need clarity on what is principal and what is a secondary claim, so labeling matters. Labeling also matters because a debtor can object to arithmetic, and the response depends on being able to show each source statement page. If the debtor argues that the creditor delayed enforcement, the creditor should respond by showing that each month was still unpaid and proven. A creditor should also be careful about mixing multiple titles, such as an interim order and a final order, without labeling the switch date. If the title changed, the ledger should show the switch month and should cite the order date as an exhibit reference. “practice may vary by authority and year — check current guidance.”

When you claim interest or other accrual components, document how you computed them so the file remains auditable. An auditable method starts with the due date for each month and the proof that the month was unpaid on that due date. It then records any partial payments and the date those payments arrived, using bank references. It then states that interest is claimed from the appropriate point under the applicable rules without inserting guessed rates. The reason to avoid guessed rates is that courts and execution offices apply legally defined rates that can change over time. If you write a rate without proof, you invite an unnecessary dispute about arithmetic instead of focusing on arrears proof. A creditor can attach a simple calculation sheet that shows columns for due date, paid date, and unpaid days, but the sheet must cite statement pages. If the debtor challenges the calculation, the creditor should respond by showing the ledger and the underlying bank statements, not by rewriting numbers. If the debtor files an objection to alimony enforcement Turkey, the court will usually test whether the objection is about title validity or about arithmetic. Title validity objections require certified copies and procedural status proof, while arithmetic objections require statement evidence and allocation clarity. For arithmetic disputes, it is often effective to propose that the court accept principal arrears immediately and leave interest for later clarification if needed. This approach can preserve collection momentum while still respecting procedural fairness. If the debtor proposes a settlement, keep settlement offers separate from the arrears ledger so the record does not look inconsistent. If a settlement is signed, update the ledger as a dated event and preserve the settlement document as an exhibit. “practice may vary by authority and year — check current guidance.”

Salary garnishment tools

Salary garnishment is often the most reliable collection tool when the debtor has formal employment. In salary garnishment alimony Turkey practice, the creditor uses the execution file to reach wages through the employer as a third party. The execution office sends a notice to the employer that specifies the alimony title and the arrears schedule. The employer is then expected to withhold the attachable portion and transfer it to the execution account or the creditor, depending on the instruction. The creditor should provide the employer’s legal name and workplace address so service is not misdirected. The creditor should also provide the debtor’s identification details so the employer can match the notice to the correct payroll profile. Wage attachments work best when the arrears ledger is month-by-month and supported by bank statements showing non-payment. The creditor should avoid vague totals because payroll departments need clear month mapping to avoid disputes. If the debtor changes jobs, the garnish can stop suddenly unless the creditor updates employer information promptly. If the debtor receives bonuses, commissions, or allowances, the creditor should expect questions about whether those items are treated as wage for attachment. The execution office will typically require traceable payment references so later objections cannot claim double collection. The creditor should keep copies of every employer notice and the employer’s response as part of the enforcement binder. If the employer fails to comply, the creditor may need additional steps against the employer, so documentation of noncompliance matters. A wage tool also reduces direct conflict because it turns payment into an administrative process rather than a monthly negotiation. The creditor should remember that the underlying family court order remains the basis and the execution office implements it procedurally. practice may vary by authority and year — check current guidance.

The first practical task is to identify the correct employer and to confirm that the debtor is on payroll under that legal entity. If the debtor works for a group, confirm whether the paying entity is a subsidiary, a branch, or a different company, because notices sent to the wrong entity delay collection. Employer details can be verified through payroll slips, SGK records, and workplace correspondence that shows the employer’s registration name. When the debtor works multiple jobs, the creditor may need parallel notices, and each notice should be linked to the same enforceable title. In execution proceedings for alimony Turkey, the creditor should keep a file note that records when each employer notice was served and what response was received. If the employer asks for clarification, respond with a copy of the judgment page and the month-by-month arrears table, not with informal explanations. If the employer offers voluntary payroll deduction, insist on traceable bank transfers with clear references to the month covered. If the debtor receives irregular pay, the creditor should still track payments by date and allocate them to months in writing. Some employers require the creditor to confirm the debtor’s identity number or personnel number, so keep identity documents ready for matching. If the debtor is paid through multiple bank accounts, the wage notice may not reach all payments, so bank attachment steps can be planned in parallel. If the debtor is on unpaid leave, the creditor should record the leave period because wage deductions may pause without meaning the obligation ended. If you need coordinated drafting and consistent employer communication, a law firm in Istanbul can manage the notice package and supplement log. A procedural overview of how divorce files translate into enforcement tasks is available in divorce representation overview. Use that overview to separate emotional divorce issues from the evidence-driven enforcement steps. practice may vary by authority and year — check current guidance.

Wage attachment is less effective when the debtor is self-employed, paid in cash, or paid through informal arrangements. In those profiles, the creditor should treat salary tools as one lane and open parallel lanes for bank attachments and asset tracing. Even when the debtor is employed, employers sometimes change payroll descriptors, and the creditor should monitor whether transfers still arrive regularly. If payments arrive without references, the creditor should immediately allocate them to specific months and notify the debtor in writing to prevent later disputes. If the employer deducts less than expected, the creditor should request the employer’s written explanation and store it as an exhibit. If the debtor claims that wage deductions are enough, compare the deductions to the arrears ledger and identify the remaining balance precisely. If the debtor changes employment, update the execution file quickly, because service delays can create long gaps in collection. If the debtor works abroad but is paid through a Turkish payroll, coordinate with the employer on where notices should be served and who handles payroll compliance. If the debtor attempts to resign to avoid attachment, document the timing and pursue alternative assets rather than relying on one tool. If the debtor negotiates a partial voluntary payment, confirm it in writing and keep the enforcement file active until the full arrears are cleared. A creditor should also track new monthly installments while collecting arrears so the case does not fall behind again. If you anticipate persistent disputes, consult a best lawyer in Turkey for a document-first strategy that minimizes procedural errors. That strategy usually includes a single ledger, a supplement protocol, and consistent payment references. It also includes monitoring of employer responses and immediate escalation when compliance fails. practice may vary by authority and year — check current guidance.

Bank account attachments

Bank attachments are used when wage deductions are insufficient or when the debtor has liquid funds that can be frozen quickly. In bank account attachment alimony Turkey practice, the execution office sends attachment notices to banks so balances are blocked up to the claimed amount. The creditor’s first job is to identify likely banks based on past transfers, salary payments, and known account relationships. The creditor should also confirm the debtor’s identification details so banks can match the notice to the correct customer profile. Attachments can reach multiple accounts, including demand deposits and sometimes other products, depending on how the bank classifies them. The creditor should not assume one bank is enough, because debtors often spread funds across multiple institutions. A focused request that lists target banks is usually more efficient than a vague request that expects the office to search blindly. The execution file should include a month-by-month arrears schedule so the bank block amount is tied to provable non-payment. If the debtor uses joint accounts, the file may require additional clarification steps, because ownership of funds can be disputed. If the debtor receives incoming transfers after the block is placed, those inflows may be captured depending on how the attachment is implemented. The creditor should store bank response letters and confirmation screenshots as part of the enforcement binder. A broader family enforcement context is available in family law context, which helps you keep the alimony lane distinct from other divorce disputes. Turkish lawyers often emphasize that bank attachments work best when combined with updated employer and registry information. This is because debtors shift funds once they realize wages are being reached. practice may vary by authority and year — check current guidance.

Before requesting attachments, reconcile your arrears ledger against your own bank statements to confirm what was actually received. A bank attachment request is stronger when each unpaid month is supported by a statement page showing absence of the transfer. If the debtor paid through cash or through third parties, label those payments clearly and attach receipts so banks are not asked to freeze amounts already satisfied. If the debtor disputes the ledger, keep your allocation rule consistent and document it in writing to prevent shifting arguments. When the execution office issues attachment notices, keep copies of the notices and record the dispatch date for each bank. When banks respond, record whether they blocked funds, whether they found no balance, and whether they requested additional identifiers. If a bank requests an identity number, provide it through the execution office channel and keep proof of delivery. If the debtor uses multiple currencies, your request should state the claim in a way the bank can operationalize without guessing. If the debtor has accounts under slightly different name spellings, prepare a reconciliation note supported by identity documents. In bilingual files, an English speaking lawyer in Turkey can help keep identity tokens consistent across foreign statements and Turkish execution notices. Consistency matters because banks match by identifiers, not by narrative explanations. If a bank blocks funds, request written confirmation so the file proves the block occurred. If a bank does not block funds, treat it as a lead and shift to other banks and asset types rather than repeating the same request blindly. Update the ledger after each collection so the next request is not inflated. practice may vary by authority and year — check current guidance.

Bank attachments can be fast, but they are not a complete solution when the debtor keeps funds outside the banking system. If the debtor uses cash-heavy practices, the creditor should shift attention to wage sources, receivables, and registrable assets. If the debtor holds assets through companies, bank attachments may reach only personal accounts and not company accounts without additional legal steps. If the debtor empties accounts quickly after payday, repeated sweeps and timing discipline become important. A creditor should therefore monitor incoming payments and file updated attachment requests when new arrears accrue. Where the debtor uses joint accounts, third parties may object and claim that part of the balance is not the debtor’s, which can slow collection. In such disputes, keep proof of the debtor’s control, such as salary inflows and regular spending patterns, to rebut nominal ownership arguments. If a bank blocks a balance but releases it due to a procedural error, record the reason and cure the error rather than blaming the bank. If the debtor negotiates a voluntary transfer, do not lift the attachment informally without receiving traceable funds and written confirmation. If you need centralized custody of bank responses and supplement logs, Istanbul Law Firm teams can keep the execution binder consistent. Consistent binders reduce disputes because every bank response is stored with its date and reference number. Bank attachments should also be coordinated with other tools so the debtor cannot simply move funds from accounts to assets. Coordination means filing employer notices, registry searches, and interim measures in a coherent sequence. The creditor should avoid excessive requests that are not supported by a clean ledger, because the file can become cluttered and less credible. practice may vary by authority and year — check current guidance.

Asset tracing and discovery

When salary and bank tools are insufficient, the next step is identifying assets that can be attached and sold through execution. Asset tracing for alimony Turkey begins with mapping the debtor’s known lifestyle, employment history, and registrable asset footprint. Start with land registry searches based on known cities and known prior addresses to identify real estate holdings. Then check vehicle ownership records and insurance evidence to identify cars and other registrable vehicles. Then check trade registry records to identify company shareholdings and directorship roles that may signal business income. The creditor should also review prior divorce and property documents because they often reveal banks, workplaces, and asset identifiers. If the debtor used real estate during the marriage, obtain historical title extracts to see whether transfers occurred after separation. If the debtor used a company, obtain current trade registry extracts to see whether shareholding changed close to enforcement steps. The creditor should avoid assuming that ownership equals control, and should look for control indicators such as continued use and continued payment of expenses. Control indicators can be proven through utility bills, maintenance payments, and repeated bank transfers to the same asset-related payees. If the debtor appears to have transferred assets to relatives, identify the relative relationship and preserve any transfer evidence as dated exhibits. A structured tracing program is easier when it is managed as one indexed project rather than as scattered requests. If you need a standardized tracing template and a supplement log, Turkish Law Firm support can keep requests consistent across registries. Consistency matters because registries and execution offices respond better to precise identifiers than to broad allegations. practice may vary by authority and year — check current guidance.

Business-related assets require a different tracing approach because value may sit in shares, receivables, or inventory rather than in visible bank balances. If the debtor owns company shares, obtain trade registry extracts and compare them to older extracts to identify recent changes. If the company has real estate, obtain the company’s property extracts so you do not miss assets held indirectly. If the debtor is a director, examine whether the company pays benefits that substitute for salary, such as vehicle leases and housing payments. These payments can signal ongoing ability to pay even when personal accounts look empty. If the debtor claims poverty, test the claim against corporate transactions that show continuing cash flow. This approach is similar to tracing in marital property files, and the methodology described in property settlement tracing can help you structure the evidence pack. When the debtor has multiple companies, build a company map that lists each entity, its registered address, and its signatory information. Then match the map to bank inflows and outflows that show dividends, management fees, or shareholder loan movements. If the debtor uses shareholder loans, request loan agreements and repayment trails to distinguish genuine debt from value extraction. If the debtor transfers shares to a relative, request the sale contract and payment proof to test whether the sale was real or nominal. A lawyer in Turkey can help convert these findings into targeted execution requests that identify the correct debtor asset and the correct registry identifier. Targeted requests reduce delay because the execution office does not need to interpret vague allegations. They also reduce objections because the debtor is confronted with specific documents and dates. practice may vary by authority and year — check current guidance.

Tracing should also include debtor receivables because receivables can be attached even when the debtor holds few liquid assets. Receivables can be identified through known customers, known employers, and repeated bank inflows from the same payers. If the debtor is a contractor, examine invoices and payment references that show which businesses pay regularly. If the debtor is a professional, examine professional platforms and client communications that reveal ongoing work streams. The creditor should avoid illegal surveillance and instead rely on lawful sources, public registries, and court-assisted document requests. Public social media can sometimes show location and lifestyle clues, but it should be treated cautiously and only as a lead, not as proof. Leads should be converted into document requests, such as registry extracts and bank confirmation requests, so the file remains evidential. If the debtor disputes that an asset belongs to them, prove control through payment of taxes, maintenance, and insurance where available. If the debtor claims that a transfer was a genuine sale, test the sale by requesting payment proof and comparing the price to market indicators. If the debtor claims that a transfer was repayment of an old debt, test it by requesting the original debt agreement and any prior repayment history. If the creditor finds repeated transfers to one relative, build a timeline and show that the pattern began only after enforcement pressure. A timeline is more persuasive than a single transaction because it shows intent through pattern without requiring speculation. Record every tracing step as a dated note so you can show diligence and explain why interim measures are needed. Keep your tracing file separate from settlement communications so negotiation does not contaminate evidence. practice may vary by authority and year — check current guidance.

Interim measures and freezes

Interim measures are used when the debtor is moving assets and ordinary execution steps may arrive too late. In interim injunction alimony Turkey practice, the creditor asks for targeted protections that preserve collectability while the enforcement file proceeds. The creditor should identify the specific asset at risk, such as a bank balance, a property transfer, or a vehicle sale. The creditor should then attach evidence that shows urgency, such as recent transfers, sudden withdrawals, or a sale listing. The request should be proportional, because overly broad freezes can be rejected as excessive. Proportionality is shown by matching the requested measure to the arrears amount and the risk evidence. Where the tool is a precautionary attachment, the conceptual framework in precautionary attachment overview helps explain how courts assess risk. The creditor should keep the alimony title and arrears ledger attached so the court sees that the claim is concrete and documented. The creditor should also show why ordinary wage or bank attachments are insufficient in the specific factual pattern. If the debtor is selling real estate, a registry annotation can be requested to warn third parties and reduce dissipation. If the debtor is transferring vehicles, a targeted restriction can prevent new registrations until the claim is resolved. If the debtor is moving cash through multiple accounts, a targeted bank freeze can preserve balances for execution. The creditor should also plan service and implementation steps, because a granted order is useless if it is not served properly. Interim tools should be integrated into the main execution plan so the case remains coherent. practice may vary by authority and year — check current guidance.

Implementation begins with obtaining a clear order that lists identifiers, account numbers, parcel numbers, or vehicle identifiers where relevant. If identifiers are missing, banks and registries may apply the order narrowly or refuse implementation. The creditor should therefore prepare identifier exhibits in advance and attach them to the interim motion. After the order is issued, serve it through the correct channel and keep service proof as a dated exhibit. Service proof is important because later objections often claim that the order was never properly notified. Once served, request written confirmations from banks or registries where possible so the file shows compliance. If a bank confirms a freeze, update the arrears ledger so later collections do not overreach the frozen amount. If a registry confirms an annotation, obtain the updated registry extract as proof of the annotation date. If the debtor attempts a transfer despite the order, preserve the attempt evidence and raise it procedurally. Interim measures should not be used as threats in negotiation, because courts expect them to be evidence-driven safeguards. If the debtor offers voluntary payment after an interim order, receive payment through traceable channels and document allocation to months. If the debtor proposes a settlement, keep the interim order in place until the settlement is signed and performance begins. If the debtor partially pays, adjust the requested scope for continued measures so proportionality remains defensible. If the court requests security or other procedural conditions, comply promptly and archive proof. practice may vary by authority and year — check current guidance.

Interim freezes should be coordinated with ongoing monthly accrual, because new installments may fall due while measures are in place. A creditor should therefore keep a running ledger and file updates as needed rather than relying on an old snapshot. Courts often expect interim measures to be time-sensitive, so the creditor should monitor whether the risk remains or has been cured. If the debtor changes employer or bank, reassess targets quickly because old targets may become empty. If the debtor is self-employed, consider whether receivable attachments and registry measures are more effective than wage tools. If the debtor holds assets through companies, assess whether corporate assets are reachable through the specific execution posture and avoid assuming direct access. If the debtor is already in financial distress, interim measures may preserve only limited value and should be paired with realistic settlement planning. Interim measures also require careful communication so the case does not escalate into parallel retaliation filings. Keep all communications factual and focused on compliance and payment proof rather than on personal conflict. If the debtor files objections, respond with service proof, the title pages, and the arrears schedule so the court sees a coherent record. If the debtor claims hardship, the creditor can still insist on traceable partial payments and a documented plan rather than informal promises. If the interim order covers property, monitor for new mortgages or liens because those can affect collectability even without a sale. If the interim order covers bank balances, monitor whether balances are released and re-frozen, and record each event with dates. Interim tools work best when they are used early, before assets are dissipated, and supported by a clean evidence spine. practice may vary by authority and year — check current guidance.

Non-payment consequences

Non-payment is treated as an arrears problem, not a new divorce problem. In practice, unpaid alimony consequences Turkey begin with a clean month-by-month ledger that shows what was due and what was received. The execution office will enforce the written title, so the first consequence is procedural pressure rather than argument about fairness. Once a file is opened, notices are served and the debtor is confronted with an official claim number and a payment demand. Each missed installment can be added to the same file, which means the debt does not stay static even if the debtor stays silent. If the debtor pays irregularly, the creditor must allocate each payment to specific months so the remaining arrears are provable. When allocation is unclear, disputes shift from non-payment to arithmetic, and collection slows. A debtor who ignores notices may face attachments on reachable income streams, including formal wages and identifiable receivables. A debtor who keeps funds in bank accounts may face rapid blocking once attachment notices reach the correct banks. “practice may vary by authority and year — check current guidance.” The debtor’s ability to obtain routine banking services can also be disrupted when accounts are repeatedly frozen and unfrozen. Where the debtor holds registrable assets, enforcement steps can create annotations and seizure risk that complicate later sales. These measures are designed to secure payment, not to create punishment narratives in the family file. The creditor should still keep communications professional, because hostile messaging is sometimes used to justify delay tactics. A disciplined file makes it easier to move from demand letters to concrete collection steps without repeated hearings. When the stakes are high, a lawyer in Turkey can help keep the ledger and service proofs coherent so the case stays about provable arrears.

Non-payment can also create procedural consequences beyond attachments, because the debtor may face additional enforcement steps when repeated defaults are documented. Execution offices often request that the creditor keep the file updated, because the office needs current arrears figures before sending new notices. If the creditor does not update, the debtor can argue that the file is inflated or unclear, and the dispute becomes procedural. Where the debtor claims inability to pay, the creditor should focus on objective indicators like wages, bank inflows, and asset use rather than on moral arguments. If the debtor is self-employed, enforcement pressure may shift toward bank sweeps, receivable attachments, and registrable asset seizures. If the debtor holds real estate, enforcement can restrict the debtor’s ability to dispose of property without resolving the file. If the debtor holds vehicles, seizure and sale tools can be pursued, but implementation depends on identification and location. “practice may vary by authority and year — check current guidance.” In some files, persistent refusal to pay can also trigger coercive remedies under enforcement law, but the conditions and procedure must be checked carefully. The creditor should therefore document each missed month with bank statements so the non-payment pattern is not disputed. Non-payment also increases litigation risk in parallel family disputes, because courts may read chronic default as noncooperation with court orders. That reputational effect is not a legal shortcut, but it can influence how the court trusts future undertakings like voluntary payment plans. Debtors sometimes attempt to pay in cash to avoid bank traces, and creditors should avoid that trap by insisting on traceable transfers. Traceable transfers protect both sides because they prevent later arguments about whether a month was paid. If the debtor threatens cross-border travel to avoid collection, the creditor should not assume flight equals evasion and should instead strengthen tracing. When the file involves foreign documents or bilingual pay records, an English speaking lawyer in Turkey can help keep translations and identity tokens consistent so the enforcement story remains verifiable.

A creditor should also understand that enforcement is rarely a single event, because alimony is recurrent and the file may stay active for months. That means the creditor needs a routine to add new months, record new payments, and reconcile balances without confusion. A monthly update habit reduces disputes because the debtor cannot claim the creditor waited and inflated the file. It also improves settlement leverage because both sides see the same running balance at any given date. If the debtor pays sporadically, the creditor should confirm allocation by a short written note so the record stays consistent. If the debtor pays through third parties, the creditor should request a transfer reference that identifies the month and the type of support. Where both spousal support and child-related support exist, the creditor should keep separate ledgers so one payment is not mischaracterized as covering both. Courts and offices are sensitive to misallocation because it can create double-counting disputes and delay collection. Non-payment also affects the household indirectly when budgeting becomes unstable, which is why predictability matters. The creditor should therefore choose tools that create predictable inflows, such as wage deductions, when they are feasible. If the debtor disputes that the obligation still exists, the creditor should point to the title and to any modification record rather than to negotiations. If the debtor claims an oral agreement to pause payment, ask for written proof and keep the request as an exhibit. If the debtor claims set-off against other divorce claims, treat it as a defense that must be proven and approved, not as a default. “practice may vary by authority and year — check current guidance.” A disciplined approach to consequences is therefore not about escalating pressure, but about keeping the file provable and the tools proportional.

Payment plans and settlements

Payment plans can be useful when the debtor has irregular income but is willing to resolve arrears without repeated attachments. The phrase alimony payment plan Turkey describes agreements that convert a volatile enforcement file into a predictable payment rhythm. A plan should start from a verified arrears ledger so both sides agree on the opening balance. It should then specify how future monthly installments will be paid while arrears are being cleared. A plan should require traceable transfers with clear references to the month covered, because references prevent later re-litigation. A plan should avoid cash handovers, because cash creates disputes about timing and amount. A plan should also address what happens if one payment is missed, so the creditor can resume execution without argument. The creditor should be careful about pausing enforcement steps without a written plan, because informal pauses can weaken leverage. The debtor should be careful about promising amounts that cannot be sustained, because broken promises create new procedural friction. “practice may vary by authority and year — check current guidance.” A plan can be documented as a written settlement and then filed into the execution record so later steps can rely on it. If the debtor wants a discount or interest waiver, the creditor should require immediate performance elements as security for the concession. If the debtor offers a lump sum, the creditor should verify funding source to avoid a payment that later bounces or is reversed. If the debtor offers installment payments, the creditor should consider whether additional security is needed, such as a pledge or a registry annotation. Because drafting details matter, many parties ask a law firm in Istanbul to format the plan in a way that is executable and easy to audit. The core principle is that a plan replaces uncertainty only when it is written, dated, and tied to the enforcement ledger.

A workable plan should also address banking logistics, because the debtor and creditor may use different banks and different transfer reference formats. The plan should state the creditor’s receiving account clearly and should specify whether payment must be made from an account in the debtor’s name. If the debtor pays from a third party account, the plan should require a written note identifying the debtor and the month covered. This reduces later defenses that payments were unrelated gifts or unrelated debt repayments. The plan should define whether payments are due on a fixed date or within a fixed window, but it should avoid assumptions about office processing times. The plan should define whether the debtor must send proof of payment on the same day and what form that proof takes. If the debtor claims technical banking problems, the plan should require immediate written notice and alternative transfer attempts. The plan should also define how partial payments are allocated, because allocation disputes are common in later objections. If arrears are large, the plan can include periodic reconciliation checkpoints where both sides sign an updated ledger. “practice may vary by authority and year — check current guidance.” If reconciliation is signed, it becomes a strong exhibit that reduces later claims of miscalculation. If the debtor’s income is seasonal, the plan can reflect that reality by combining smaller routine payments with occasional larger catch-up payments. Any such structure should remain realistic and should be supported by traceable payment proofs. In practice, a centralized drafting and custody role by Istanbul Law Firm can help keep the signed plan, the ledger updates, and the bank proofs in one coherent binder. Coherent custody prevents a later dispute about which version of the plan was agreed and which payments correspond to which clause.

Settlements should also consider how the execution file will be handled after payment begins. If the creditor closes the file too early, re-opening later can take time and the debtor may exploit the gap. If the creditor keeps the file open, the debtor may argue that ongoing enforcement measures are disproportionate once the plan is followed. The safer middle path is to keep the file open but suspend aggressive measures while payment is regular, with written confirmation of the suspension terms. Any suspension should be reversible if a payment is missed, and that reversibility should be written clearly. If the settlement includes a lump-sum component, the creditor should confirm receipt and allocation immediately in writing. If the settlement includes a waiver of some arrears, the waiver should be conditional on full performance, not unconditional from day one. If the settlement covers both spousal maintenance and child-related support, allocate payments explicitly to avoid later misclassification. The settlement should also address future modifications, stating that only a court modification changes the legal obligation. “practice may vary by authority and year — check current guidance.” The debtor should avoid claiming that the settlement automatically changes the underlying judgment, because the judgment remains the title until modified. The creditor should avoid using settlement drafts as leverage by threatening unrelated enforcement actions, because that can harm credibility. If property disputes are ongoing, keep settlement wording consistent with other case files so one statement does not contradict another. If the debtor’s assets are volatile, consider keeping a limited freeze on specific assets until a defined performance milestone is reached. A settlement works only when it is implemented as a verifiable payment routine with receipts, references, and a clean update log.

Objections and defenses

Debtors often respond to enforcement by filing procedural objections rather than by paying immediately. The phrase objection to alimony enforcement Turkey covers challenges that target the title, the ledger, the service record, or the collection step. A creditor should treat objections as normal and prepare a response pack before filing, because objections slow collection when the file is disorganized. The first common objection is that the amount is calculated incorrectly, usually because payments were not allocated clearly to months. The second common objection is that payments were made in cash or through third parties and were not credited properly. The third common objection is that the order was modified, suspended, or replaced, and the creditor is enforcing an outdated title. The fourth common objection is that service was defective, meaning the debtor claims the notice was not properly delivered. The fifth common objection is that the claimed months were not yet due or were already covered by another payment obligation. Each objection must be answered with documents, not with argument about fairness or hardship. “practice may vary by authority and year — check current guidance.” A creditor should therefore keep a title tab, a service tab, and a ledger tab so each objection category can be answered quickly. Where the debtor claims payment, demand the bank reference and the date so the claim is testable. Where the debtor claims modification, demand the court decision and its notification proof so the change is verified. Where the debtor claims set-off, demand a written agreement or court decision, because set-off is not assumed. Because objection response requires procedural precision, some creditors consult a best lawyer in Turkey to keep the file clean and to avoid technical slips. A clean response often narrows the dispute to one arithmetic point that can be cured by a supplement without stopping all collection.

Debtors also raise defenses that are not strictly procedural but still influence how the court views the execution file. One defense is that the creditor accepted a different payment arrangement orally, and the debtor argues that enforcement is bad faith. The creditor should answer by asking for written proof and by showing that the judgment remained in force. Another defense is that the debtor paid other family expenses and believes those expenses should offset alimony. The creditor should answer by pointing to the title wording and by showing that offsets require written agreement or court adjustment. Another defense is that the debtor is unemployed and cannot pay, but inability claims still must be tested against asset and bank evidence. If the debtor has a business, examine corporate inflows and benefits to test whether income is merely hidden. Another defense is identity confusion, where the debtor claims the attachment targeted the wrong person with a similar name. Identity defenses are answered by passport copies, national ID numbers where available, and consistent service records. “practice may vary by authority and year — check current guidance.” Another defense is that the creditor’s ledger double-counts months, which is why a stable allocation rule is essential. If the debtor alleges double counting, provide statement pages and a ledger that allocates each incoming transfer to a specific due month. If the debtor alleges that the creditor inflated interest, respond by separating principal and interest and asking the office to apply the legally correct method. In complex files with multiple titles and multiple modifications, a Turkish Law Firm can maintain a consolidated chronology so defenses are answered consistently. Consolidated chronology matters because defenses often succeed only when the file contains internal contradictions that the debtor can exploit.

A creditor should also decide which disputes are worth litigating and which can be cured quickly by clarification. If the dispute is about one month, a fast cure can be more efficient than a long fight that delays collection of all months. A common cure is to file a corrected arrears table with supporting statements and to request that enforcement continue on the undisputed portion. Another cure is to provide a written allocation note that states which months were covered by each payment reference. If the debtor provides a new payment receipt, the creditor should verify it against their own statement before conceding. If the debtor provides a modification decision, the creditor should verify notification dates and effective scope before adjusting the ledger. If the debtor challenges service, the creditor should obtain service proof from the file and confirm address details for re-service if needed. If the debtor claims that attachments are excessive, the creditor should show proportionality by limiting requests to the proven arrears amount. If the debtor proposes settlement during objection, the creditor should not abandon the file unless the settlement is signed and performance starts. “practice may vary by authority and year — check current guidance.” Objection management also includes communication discipline, because hostile messages can be used to frame enforcement as harassment. Keep communications factual and refer to the ledger and receipts rather than to emotions. If the debtor is represented, send communications through counsel to avoid inconsistent side statements. If the creditor is represented, ensure that every supplement is logged and every exhibit number is consistent across submissions. A structured objection response keeps enforcement focused on proof and prevents the debtor from turning the case into a general divorce conflict.

Evidence and documentation

Enforcement is won or lost on the quality of the evidence pack, because execution offices and courts implement documents, not memories. The phrase evidence of non-payment alimony Turkey refers to bank statements, receipts, and allocation records that show exactly which months were unpaid. Start with the enforceable title and place the operative pages at the front of the binder. Then attach a month-by-month ledger that lists due amounts and incoming payments with bank references. Then attach your own bank statements that show incoming transfers, or show their absence, for each relevant month. Where payments were made in cash, attach signed receipts and label which month each receipt covers. Where payments were made through third parties, attach the transfer proof and a note linking the payer to the debtor. Where the obligation includes child elements, keep a separate sub-ledger and coordinate it with the guidance at child support rules so allocation is not confused. Keep service proofs for every notice, because service is often challenged in objections. Keep copies of employer notices and bank attachment notices, because they prove what actions were taken and when. “practice may vary by authority and year — check current guidance.” A disciplined evidence pack also includes a chronology page that lists filing date, service date, and each enforcement step date. Chronology helps the judge understand why interim measures were requested or why repeated attachments were necessary. Many Turkish lawyers recommend building this binder before filing so you can answer objections on the same day they arrive. Binder discipline also reduces conflict because it makes the dispute about numbers and proofs, not about blame. When the binder is complete, the execution office can move quickly from title verification to practical collection steps.

Documentation must also be presented in a form that is easy for a clerk to check under time pressure. Use an index page that lists each exhibit and the page range where it appears in the binder. Use consistent naming conventions for PDF files if you submit digitally, such as Month-Year-Statement and Month-Year-Receipt. Do not submit cropped screenshots without account identifiers, because they invite authenticity objections. If you use exports from a banking app, keep the export metadata and the bank confirmation page that shows the export is official. If you translate any document, attach the source and translation together and keep identity spellings consistent. If the debtor has multiple identities or name variants, include a token sheet and a reconciliation note. If you calculate arrears, show your method in a simple table and cite the statement page for each unpaid month. If you claim interest, keep the principal ledger separate from the interest method note so the dispute does not become arithmetic noise. “practice may vary by authority and year — check current guidance.” If the debtor pays after you file, update the ledger as a dated supplement and attach the payment proof to the file. If the debtor pays directly to you rather than through the office, record that payment in writing and store the message as a supplementary exhibit. If the debtor pays in cash, insist on a signed receipt with date and month allocation, and store a scan immediately. If you negotiate a plan, attach the signed plan to the binder and mark which months are governed by the plan. Documentation discipline reduces the risk that the debtor can claim confusion and delay collection through procedural objections.

Evidence should be preserved even after partial collection, because enforcement files often stay open across multiple months. Preserve each year’s statements and receipts as a separate archive tab so you can answer questions quickly later. Preserve the execution office correspondence, because later disputes may ask what notices were sent and what responses were received. Preserve proof of service, because service can be challenged months later when the debtor changes address. Preserve employer responses, because employer changes are common and past employer compliance may still be relevant. Preserve bank responses, because banks often ask for reference numbers when you renew an attachment request. If the debtor makes payments sporadically, preserve allocation confirmations so the record does not drift. If a modification action is filed, preserve the modification pleadings and any interim orders, because the enforcement ledger must adjust only when a court decision is effective. If a cross-border issue later arises, preserve identity documents and translations so recognition steps are not delayed by missing pages. “practice may vary by authority and year — check current guidance.” Preserve your own bank statements as well, because the absence of incoming transfers is often the simplest proof of non-payment. Preserve any settlement drafts separately from the execution binder to avoid accidental admissions in the formal file. Preserve your communication log, because the log shows cooperation attempts and rebuts harassment narratives. If you change counsel, perform a handover audit so the new counsel receives the full binder and not a partial selection. A preserved, indexed archive turns enforcement into a repeatable routine and reduces the chance that the case collapses into confusion.

Criminal law overlaps

Enforcement files sometimes intersect with criminal law narratives, but the legal lanes are different. Execution is designed to collect money under a written title, not to decide guilt. Non-payment is usually handled through execution proceedings and coercive procedural tools, not through ordinary criminal charges. Parties should therefore avoid threatening language that suggests punishment will follow automatically. The execution office implements the order and records payments and arrears in a file. If the debtor argues hardship, the correct response is still evidence and procedure, not confrontation. Where enforcement law provides coercive measures, those measures are initiated through specific applications and judicial review. They are not a substitute for wage attachment, bank attachment, or asset seizure. A creditor should keep the file focused on provable arrears, service proofs, and allocation of payments to months. A debtor should keep the file focused on provable payments and provable modifications, not on general complaints. If parallel accusations exist, parties should still preserve the enforcement record because the enforcement record is often the most objective timeline. Courts and offices tend to respond better when the communication is calm and supported by exhibits. If a protective order is involved, the parties should comply with it and use neutral channels for payment communication. The creditor should also avoid using relatives as messengers because that creates new conflict evidence. “practice may vary by authority and year — check current guidance.” In contested files, coordination with counsel can help keep the enforcement lane separated from any criminal allegations and prevent procedural mistakes.

Turkey’s enforcement system includes mechanisms that can have coercive effects when a debtor persistently ignores a court-ordered support duty. These mechanisms are processed through the enforcement judiciary framework rather than through ordinary criminal prosecution files. A creditor should confirm the exact procedural prerequisites in the specific execution office file before making any application. A debtor should also confirm the prerequisites before assuming that a payment plan will stop every step automatically. If the debtor has objections, they must be presented through the correct objection channel with supporting documents. If the debtor has made payments, the debtor should submit bank proofs and request ledger correction rather than rely on verbal explanations. If the debtor’s account is frozen, the debtor should coordinate release only after payment is recorded in the file. If the creditor seeks a coercive step, the creditor should attach the service record, the arrears table, and the non-payment proofs as exhibits. If the creditor seeks a coercive step for multiple months, the months should be listed clearly so there is no ambiguity about scope. If the debtor claims that the title was modified, the debtor should provide the modification decision and notification proof. If the debtor claims that the creditor waived arrears, the debtor should provide a written waiver rather than a message fragment. Some files also include allegations of document falsification, concealment, or fraudulent asset transfers, which can create separate criminal investigations. Those investigations do not replace the execution file and do not automatically collect arrears. If such allegations exist, keep the enforcement submissions strictly evidence-led so the execution court can proceed without being distracted. A creditor should not use criminal complaints as leverage in settlement messaging because it can backfire and complicate negotiation. A debtor should not assume that filing a complaint will pause execution because execution and investigation lanes are distinct in practice.

Criminal-law overlap concerns also appear when parties mix alimony disputes with broader divorce conflict narratives. Courts will usually separate the financial duty from personal blame and will focus on the enforceable title. If child support exists alongside spousal support, keep separate ledgers so enforcement does not become confused. If property settlement enforcement is also pending, keep separate files so bank and registry actions are not mischaracterized. Debtors sometimes argue that they are paying other expenses and therefore should not face enforcement, but execution follows the written title. Creditors sometimes argue that a debtor’s new spending shows bad faith, but the stronger approach is to trace attachable income and assets. If the parties agree on temporary offsets, document them carefully and file them as supplements so the execution ledger reflects the agreement. If the parties do not agree, avoid self-help offsets because they frequently become objections. If the debtor threatens to report the creditor for harassment, keep communications formal and route them through counsel when necessary. If the creditor fears intimidation, use lawful protective channels and keep payment communication separate from personal contact. If an enforcement hearing is scheduled, bring the full ledger, service proofs, and updated payment receipts in an indexed binder. If the debtor is abroad, keep service proofs and translation packages complete so procedural challenges do not derail the file. If the debtor is self-employed, focus on receivable attachments and registry assets rather than expecting wage tools to work. If the debtor is a company owner, focus on personal distributions and personal assets because corporate assets have their own legal lanes. “practice may vary by authority and year — check current guidance.” The practical rule is to keep the enforcement file provable and narrow so any parallel investigation does not freeze progress.

Cross-border enforcement

Cross-border enforcement begins when the debtor lives outside Turkey, holds assets abroad, or receives income through foreign channels. The phrase cross-border alimony enforcement Turkey captures the need to coordinate Turkish execution tools with foreign collection realities. A Turkish execution file can reach assets located in Turkey, but it cannot directly seize assets located in another country without an external process. The creditor should therefore map where the debtor’s income is paid and where accounts are held before choosing tools. If the debtor has a Turkish salary but travels abroad, wage attachment may still be the most efficient tool. If the debtor has foreign salary only, the creditor must consider recognition or cooperation mechanisms in the foreign jurisdiction. If the debtor uses international banks with Turkish branches, the creditor should confirm whether Turkish attachments can reach the specific account. If the debtor holds Turkish real estate, the creditor can use registry attachments and sale tools regardless of residence abroad. If the debtor holds Turkish companies, the creditor can trace personal distributions and personal accounts within Turkey. Service is often harder when the debtor is abroad, so the creditor should keep address proof and contact identifiers current. If the debtor disputes identity, the file should include passport copies and consistent name spellings across translations. If the creditor is abroad, a representative can manage the file, but the representative authority document must be complete and usable. If payments must be received abroad, the creditor should still insist on traceable transfers and clear month references. Cross-border situations also raise travel and immigration questions for the debtor, but the enforcement lane remains document-driven. “practice may vary by authority and year — check current guidance.” A careful plan treats cross-border enforcement as a project with a Turkey asset lane and a foreign asset lane that are coordinated but separate.

Sometimes the creditor holds an alimony order issued by a foreign court and needs to enforce it against assets in Turkey. The phrase recognition of foreign alimony order Turkey refers to the legal step that makes a foreign decision usable for Turkish enforcement. This step is not automatic, because Turkish authorities usually require a recognition and enforcement process before execution offices act. The starting point is to collect the complete foreign judgment, including finality notes, service records, and any annexes that define the payment duty. The next step is to obtain a certified translation that preserves names, dates, and amounts without drift. The next step is to prepare a procedural petition that explains the foreign decision and requests recognition and enforcement in Turkey. If the foreign decision includes both support and other family orders, the petition should isolate the enforceable payment obligation clearly. If the debtor argues lack of proper notice abroad, the creditor must answer with service proofs and procedural records from the foreign file. If the debtor argues public policy, the creditor should keep the argument technical and tied to the record rather than emotional. A helpful overview of the general process is available in recognition and enforcement procedure. After recognition is granted, the creditor can open a Turkish execution file using the recognized decision as the title. If the debtor paid partially abroad, the creditor should keep payment proofs so the Turkish ledger does not overstate arrears. If the debtor has multiple currencies in the foreign order, the creditor should separate principal from conversion mechanics and avoid speculative assumptions. If the creditor is enforcing ongoing monthly installments, the petition should clarify how future months will be treated in Turkey. “practice may vary by authority and year — check current guidance.” Recognition work is therefore an evidence packaging exercise that must be completed before ordinary Turkish attachments are effective.