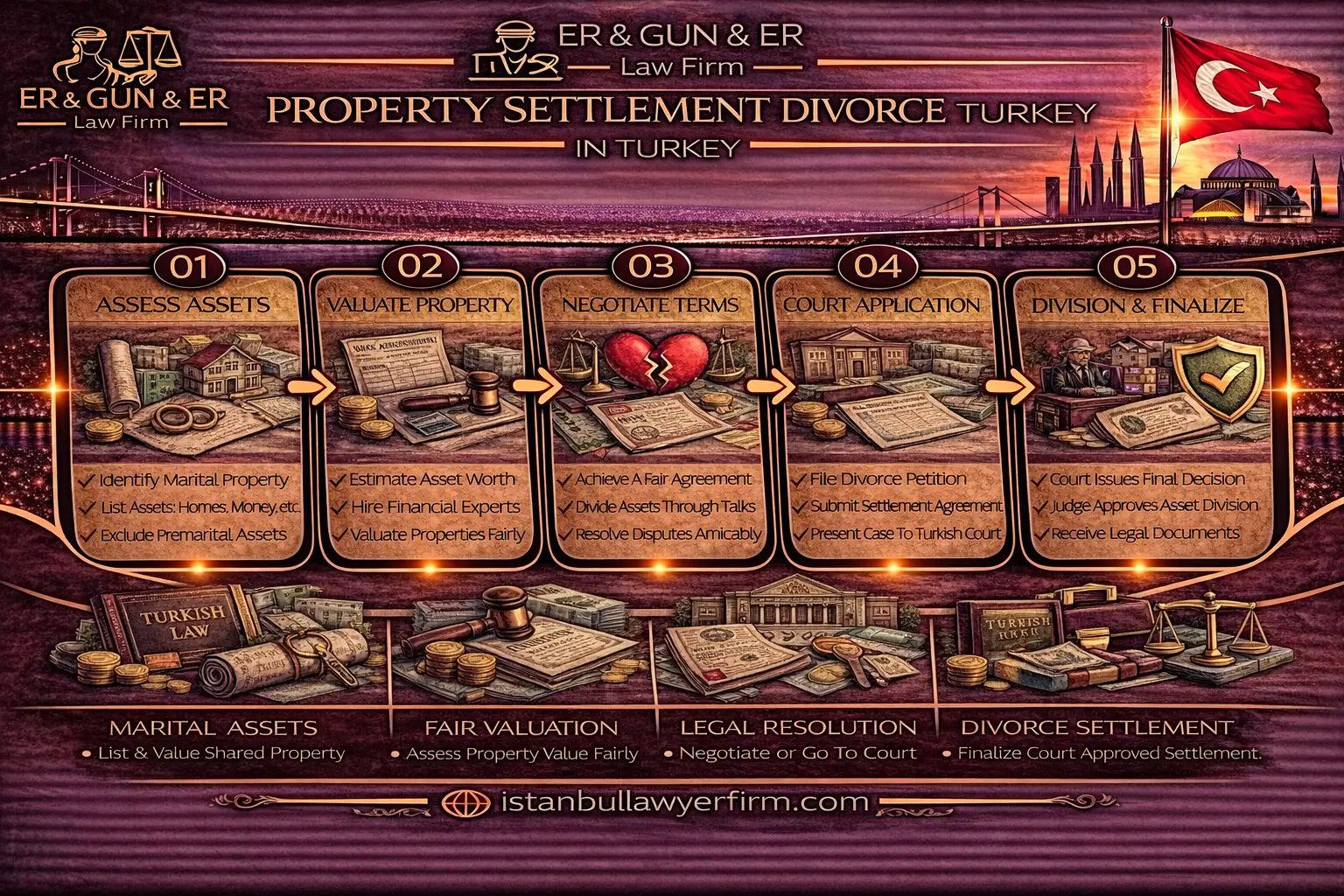

Property settlement in Turkish divorce is the financial liquidation between spouses that follows the dissolution of the marital bond — the systematic accounting of assets, debts and compensatory claims that converts the substantive marriage relationship into a dischargeable economic separation. The framework that governs the process is set primarily by the Türk Medeni Kanunu (Law No. 4721, the Turkish Civil Code), which establishes the marital property regimes (mal rejimleri), the default edinilmiş mallara katılma rejimi (participation in acquired property regime) that applies absent a contractual choice, the contractual alternatives available to spouses through prenuptial or post-marital agreements, and the substantive rules governing classification of assets as acquired (edinilmiş mal) or personal (kişisel mal). The framework is supplemented by the Hukuk Muhakemeleri Kanunu (Law No. 6100) governing civil procedure including proceedings before the Aile Mahkemesi (Family Court) and ihtiyati tedbir (interim injunction) procedure; the İcra ve İflas Kanunu (Law No. 2004) governing enforcement of property settlement judgments; and the Tapu Kanunu (Law No. 2644) governing real estate registration including post-divorce property transfers. Practice may vary by authority and year.

An English speaking lawyer in Turkey advising foreign spouses on Turkish-property settlement will explain that the divorce judgment terminates the marriage but does not automatically liquidate the marital property regime — the property accounting proceeds either through a separate liquidation case (mal rejimi tasfiyesi davası) before the Aile Mahkemesi or through a settlement agreement that the parties negotiate either before or after the divorce decree. The body of this guide walks through the legal framework of marital property regimes, the acquired-versus-personal classification analysis, the asset inventory and tracing discipline including hidden asset techniques, the valuation methodology for real estate and business interests, the evidence collection and interim measures architecture, the expert report (bilirkişi raporu) framework, the settlement negotiation strategy, the court procedure before the Aile Mahkemesi, and the judgment enforcement under the İcra ve İflas Kanunu. For procedural orientation on adjacent topics, our notes on family law in Turkey, divorce counsel framework, title deed verification, precautionary attachment basics, enforcement proceedings and prenuptial agreements in Turkish law can be read alongside this material.

1) Legal Framework: Marital Property Regimes under the Türk Medeni Kanunu

A lawyer in Turkey who maps the marital property regime framework will start with the Türk Medeni Kanunu's substantive structure. Since 2002, the Civil Code has provided four mal rejimi (marital property regime) options: the default edinilmiş mallara katılma rejimi (participation in acquired property regime) that applies absent a contractual choice; mal ayrılığı rejimi (separation of property regime) that maintains complete separation; paylaşmalı mal ayrılığı rejimi (separation of property with sharing of certain assets); and mal ortaklığı rejimi (community of property regime). Spouses can select an alternative through a written agreement executed before a Turkish notary either before marriage (prenuptial agreement) or during marriage (post-marital agreement); absent such an agreement, the default edinilmiş mallara katılma rejimi applies automatically as the operative regime governing all asset classification and liquidation analysis.

An Istanbul Law Firm advising on the default regime's mechanics will explain that the edinilmiş mallara katılma rejimi distinguishes between two categories of assets: edinilmiş mal (acquired property) — assets acquired during the marriage through marital effort or income — and kişisel mal (personal property) — assets owned before the marriage, gifts and inheritances received during the marriage, and certain other categories including personal-use items and compensation for non-pecuniary damages. Upon dissolution, each spouse retains ownership of their personal property; the acquired property pool is divided according to the regime's settlement rules, with each spouse entitled to participate in half the net value of the other spouse's acquired property after deduction of debts and personal claims. The procedure ordinarily requires the calculation to be performed at a defined valuation date set by the Civil Code's framework, with the marital property regime ending on the date of divorce filing rather than on the date of separation or the date of judgment.

A Turkish Law Firm coordinating the regime determination at the kick-off stage will identify the regime period segmentation that applies where spouses changed their regime during marriage. Where spouses entered into a contractual alternative regime midway through marriage, the property accounting can be segmented into pre-change and post-change periods with different regime rules applying to each segment, requiring careful timeline mapping that aligns asset acquisition dates and principal payment dates with the operative regime in force on each date. The standard approach is to fix the regime structure at the kick-off stage through documentary review (marriage certificate, any notarized property agreement, any subsequent amendment) before any classification or valuation work begins, because every later step depends on which regime governs which segment. Practice may vary by authority and year. The discipline outlined in our note on prenuptial agreements in Turkish law covers the contractual-regime architecture in greater depth. The valuation-date analysis under the default regime deserves separate attention because it determines what value figure enters the participation calculation. The Civil Code's framework distinguishes between the regime-ending date (the divorce filing date for the default regime) and the valuation date for individual assets, with the latter typically set at the date of judgment or settlement for assets that remain in existence and at the date of disposition for assets that were sold or otherwise transferred during the regime period or thereafter. Where the asset's value has changed substantially between the regime-ending date and the valuation date, the change can affect either spouse's participation entitlement; the standard approach is to track the asset's value through documentary evidence at multiple dates so the file can support whichever date the court ultimately treats as legally relevant. Where the spouse-side analysis differs on the date question, the file presents both valuations with the underlying methodology rather than committing to a single number that may not align with the court's eventual determination.

2) Acquired vs. Personal Asset Classification under the Default Regime

An English speaking lawyer in Turkey explaining the classification analysis will start with the substantive distinction between edinilmiş mal and kişisel mal under the default regime. Acquired property includes all assets acquired during the marriage through marital effort or income, with employment income, business income, professional fees, investment returns generated during marriage, and assets purchased with such income all presumptively classified as acquired property absent contrary proof. Personal property includes assets owned by either spouse before marriage; gifts received from third parties during marriage; inheritance received during marriage; personal-use items including clothing and personal effects; non-pecuniary damages compensation for personal injury or moral harm; and substitution assets where personal property has been converted into a different form (sale of pre-marital real estate followed by purchase of replacement real estate) provided the conversion chain can be documented through traceable transfers.

Turkish lawyers who handle the classification disputes that drive most property settlement litigation will identify the recurring boundary cases. Renovations or improvements to personal property using marital income create a participation claim by the non-owner spouse against the increased value, with the calculation methodology depending on whether the improvement is documented as a discrete contribution or as a continuous funding pattern. A business started before marriage but grown substantially during marriage creates classification questions about whether the value increase is attributable to marital effort, to market appreciation, or to a combination, with the proportion typically requiring expert analysis. A bank account opened before marriage but receiving salary deposits during marriage creates mixing problems where the file must segregate pre-marital balance from marital deposits to determine which portion is personal and which is acquired. Professional goodwill — the value attributable to a spouse's individual professional reputation and practice — produces particularly complex classification issues because the goodwill cannot be transferred independently of the practitioner.

An Istanbul Law Firm building the classification architecture will treat each disputed asset as a documentary chain rather than as a category label. The procedure ordinarily requires matching each asset to its acquisition evidence (purchase contract, deed, share transfer record), then matching the acquisition evidence to its funding evidence (bank statement showing the payment, salary record showing the funding source, gift transfer documentation showing the personal channel where applicable), then assembling the documentary chain into a single classification memorandum that connects each step by date. Where the chain crosses foreign accounts, foreign vital records or foreign supporting documents, apostille or consular legalization with sworn Turkish translation must be added to the chain. Where one spouse controls the documents and disclosure is incomplete, the file should record each disclosure request and refusal as dated events that justify court-assisted disclosure motions later. Practice may vary by authority and year, and the classification architecture is the foundation on which every subsequent valuation and tracing step rests. The classification memorandum format itself deserves attention because the document operates as both an internal analytical tool and an external pleading exhibit. The standard format covers the asset description and identification reference (TAPU number for real estate, IBAN for bank accounts, plate number for vehicles, share-register entry for company shares); the acquisition date and acquisition mechanism (purchase, gift, inheritance, succession); the funding source and funding-channel evidence connecting acquisition to either marital income or a personal-channel inflow; the classification conclusion (acquired property, personal property, mixed with segregable components, or unresolved pending additional evidence); and the supporting exhibit references with specific document numbers and page-range citations. Where the asset is mixed with both acquired and personal funding sources, the memorandum performs component-by-component segregation rather than collapsing the analysis into a single binary conclusion, because component-level analysis preserves the file's optionality for either expert-side or court-side resolution of the unresolved portion.

3) Asset Inventory, Tracing Discipline and Hidden Asset Analysis

A Turkish Law Firm coordinating the asset inventory will treat it as the operational foundation of the property settlement file because the case cannot proceed beyond what is listed and documented. The procedure ordinarily requires the inventory to cover real estate (with TAPU references and current Tapu Müdürlüğü extracts), vehicles (with traffic registration records), bank accounts (with statements covering the entire regime period rather than only recent months), securities and investment accounts, business interests (with Ticaret Sicil Müdürlüğü extracts and shareholder register records), receivables and intellectual property where the spouse is self-employed, valuable movables (jewelry, art, collectibles), and the corresponding debt schedule listing creditor names and supporting loan documentation. Tracing connects each asset to its funding source and to the regime period through a transaction timeline showing when money moved, who controlled it, and what it purchased; tracing also identifies related-party transfers that may have reduced the visible marital pool below its actual size. The inventory governance discipline operates as a continuous workstream rather than as a discrete kick-off task because new assets often surface as the proceeding develops — through expert analysis, through court-ordered disclosure, through discovery of foreign holdings, or through patterns identified through cash-flow reconstruction. The standard approach is to maintain a master inventory document with version control showing each addition, modification and verification with the date and source; to maintain a parallel evidence index showing which exhibits support each inventory entry; and to maintain a custody log recording who holds each original document so authenticity questions can be answered without delay. Where the inventory expands substantially during the proceeding, the file's procedural posture should expand correspondingly through supplemental pleadings rather than left to argue the new assets at a single end-of-case hearing where the court has limited capacity to absorb new factual developments.

An English speaking lawyer in Turkey advising on asset concealment risk will explain that the inventory must be assembled urgently because assets can move quickly once separation becomes likely. Common concealment patterns include repeated cash withdrawals reducing visible bank balances, transfers to close relatives presented as loan repayments or gifts, sudden shifts of vehicle or share ownership to third parties while the spouse continues to use or control the asset, sales of assets below market value with the difference recorded as unexplained discount, and operational concealment in business families where personal expenses are paid through company accounts and labeled as business costs. The procedure ordinarily requires the file to freeze a baseline inventory at the earliest possible point through registry extracts, account snapshots and corporate records; build a movement timeline flagging transactions occurring near separation events; identify the "control person" for each asset (who can sign, withdraw, sell); and build dated request-and-refusal logs that support later court-assisted disclosure motions before the Aile Mahkemesi.

Turkish lawyers who handle cross-border concealment patterns will note that hidden asset work often becomes international because funds may be routed through foreign accounts, overseas companies or foreign relatives. The procedure ordinarily requires preserving identity continuity (consistent passport-name spelling across foreign and Turkish documents), obtaining foreign bank statements in official authenticated form with metadata preservation, collecting corporate extracts and director lists for foreign-held entities with evidence of bank-mandate control, and coordinating tax-narrative consistency so that court submissions do not contradict tax filings or other regulatory submissions. Where offshore entities, trusts or nominee arrangements exist, the operative analytical question is who enjoys the benefit and who can revoke the arrangement rather than the formal title structure. The standard approach is to convert concealment suspicion into a finite set of documented transfer questions that an expert and judge can answer through verifiable exhibits, rather than to proceed on broad allegations that the courts treat as fishing expeditions. Practice may vary by authority and year. Cross-border concealment cases also produce specific evidentiary advantages where the receiving foreign jurisdiction maintains beneficial-ownership registers (now common in many European jurisdictions following anti-money-laundering reforms) or imposes mandatory beneficial-ownership disclosure for company structures. The standard approach in such files is to obtain the foreign register extracts as part of the documentary chain, with apostille or consular legalization as the authentication route appropriate to the jurisdiction. Where the concealment vehicle is a trust or nominee arrangement in a jurisdiction without public beneficial-ownership disclosure, the operative analytical strategy shifts to documentary surrogates — payment instructions, email approvals, signature logs and corporate banking mandates — that demonstrate de facto control regardless of the formal structure. The discipline outlined in our note on divorce counsel framework covers the broader procedural architecture within which cross-border concealment analysis operates.

4) Real Estate Valuation, Bank Accounts and Cash-Flow Reconstruction

An Istanbul Law Firm advising on real estate valuation will explain that real estate is typically the largest asset category in property settlement files and drives both negotiation leverage and judgment enforcement complexity. The procedure ordinarily requires an indexed valuation pack covering the legally relevant valuation date for the specific file, the property's status as vacant, occupied or subject to lease, the encumbrance profile (mortgages, liens, lease registrations) affecting net value, the renovation and improvement contribution analysis where marital funds enhanced the property, comparable sales evidence supporting the value range, and an expert appraisal applying methodology appropriate to the property type. Where the property is held jointly, the file should distinguish between disputes about the registered ownership ratio and disputes about compensation for unequal contributions. Where the property is in a site complex, common-area fees and site restrictions affect market value and should be documented. Where the property is under construction, valuation methods differ from completed-stock comparables.

A lawyer in Turkey coordinating bank-account analysis will explain that bank accounts present the inverse problem to real estate: easy to move and difficult to reconstruct after separation. The procedure ordinarily requires listing every known bank and account type used during the marriage, requesting full statement coverage for the entire regime period rather than only recent months, building a cash-flow timeline that ties each major inflow and outflow to dated supporting evidence, matching salary inflows to employment records, labeling family-member transfers with transfer descriptions and supporting correspondence, and reconciling the cash-flow timeline against asset acquisitions to confirm that funded purchases align with provable inflows. The discipline outlined in our note on title deed verification covers the registry-side analysis that supports the real estate inventory; the bank-side reconstruction operates as the parallel financial layer that connects funding evidence to acquisition evidence.

Turkish lawyers who handle cash-flow disputes will note that household consumption and asset acquisition produce different legal consequences and must be separated in the analysis. Routine living expenses do not create shareable assets but explain where withdrawals went; asset purchases funded through bank transfers must be mapped to registry records and contracts for traceability. Where a spouse used corporate accounts for personal spending, the file must separate corporate evidence from personal evidence carefully because mixing creates ownership-question ambiguity that courts treat skeptically. Where deposits are characterized as gifts, loans or sale proceeds, the relevant supporting evidence (donor transfer note, loan agreement and repayment trail, sale contract and payment confirmation) must be in the file rather than asserted in pleadings. Practice may vary by authority and year. Foreign bank statements can be used in Turkish proceedings but require sworn translation with consistent identity-token spelling so the same account does not appear to belong to different persons across the file. The currency-exposure analysis adds a separate dimension where the marital pool includes assets denominated in foreign currencies, because exchange rate movements between the regime-ending date and the valuation date can materially affect the participation calculation. The standard approach is to record the exchange rate on each legally relevant date through Türkiye Cumhuriyet Merkez Bankası (TCMB) reference data, then apply the appropriate rate at each calculation step rather than collapsing currency conversion into a single end-of-case rate that may misrepresent the marital pool's underlying value. Where the spouses' commercial life involved frequent currency movements (international employment income, foreign-asset disposals during marriage, multi-currency banking), the cash-flow reconstruction must track the currency of each transaction so the expert analysis works from accurate denominations rather than from approximated Turkish-lira equivalents that lose precision across multiple conversion steps.

5) Company Shares, Business Valuation, Gifts and Inheritances

A Turkish Law Firm advising on business valuation will explain that company interests are typically the most contentious asset category because value is not visible on a registry extract and depends on accounting integrity, market conditions and management discipline. The procedure ordinarily requires identifying the legal form of the business interest (shares in an anonim şirket, ortaklık payı in a limited şirket, partnership interest, sole proprietorship), obtaining Ticaret Sicil Müdürlüğü extracts and shareholder registers showing ownership percentages over time, determining whether the business interest was acquired during the regime period or before it, and assembling the financial inputs (annual financial statements, ledger detail for key accounts, tax filings, management accounts, customer contracts) that support the valuation analysis. Where the company holds real estate, the real estate valuation should be separated from the operating business valuation to avoid double counting; where the company holds vehicles, equipment or intellectual property, those items should be inventoried separately with encumbrance analysis. The capital-structure analysis adds a separate dimension where the company has multiple share classes, preferred shareholders or investor-side rights through shareholder agreements, because each layer affects the realizable value of the spouse's share interest. The standard approach is to obtain the full capital structure documentation — the company's articles of association (esas sözleşme), any shareholder agreement (pay sahipleri sözleşmesi), any share-class differentiation, any transfer-restriction provisions, any drag-along or tag-along rights, any preferred-distribution arrangements — and to map the spouse's share interest against this structure to identify what realizable value the share interest actually carries. Where the share interest is structurally illiquid (closely held company without realistic exit path, transfer restrictions blocking third-party sale, minority discount applicable, preferred shareholder priority reducing common-share residual), the valuation analysis cannot apply unadjusted enterprise-value methodology without overstating the spouse's actual entitlement, and the participation calculation must reflect the realizable rather than the theoretical value.

An English speaking lawyer in Turkey advising on business-valuation disputes will note the recurring patterns that make this category technically demanding. Where bookkeeping is weak, the expert may rely on bank flows and third-party invoices to reconstruct performance; where the company is closely held, related-party transactions can distort profit figures and require ledger-level scrutiny; where the spouse claims that revenue fell suddenly, the claim should be tested against bank inflows, customer contracts and tax declarations; where the spouse claims the company is worthless or alternatively highly profitable, both extremes should be tested against documentary reality rather than accepted as positions. Where transfer restrictions limit share marketability, a discount argument may apply but must be supported by the corporate documents and any shareholder agreement. Where dividends were paid during separation or salaries were used to extract value, payroll records and expense policies become valuation inputs alongside the financial statements.

Turkish lawyers who handle the gifts-and-inheritances classification dimension will note that this is one of the most frequently invoked exclusion arguments and one of the most commonly under-documented in foreign-spouse files. The procedure ordinarily requires the gift or inheritance claim to be supported by donor transfer evidence (bank credit, donor capacity proof, contemporaneous correspondence explaining purpose) for gifts, or probate documents and estate distribution records for inheritances, with the funds traced through the receiving account into any subsequent acquisition the claimant attributes to the personal source. Where the inherited or gifted funds were mixed with marital income in the same account, the file must attempt component-by-component segregation through dated records rather than abandoning tracing entirely. Where the donor is abroad, foreign bank statements with consistent identity tokens become central; where the donor is deceased, estate distribution evidence must be obtained early because estate documentation becomes harder to access over time. Practice may vary by authority and year, and the classification of gifts and inheritances frequently determines whether a substantial asset is shareable, partially shareable through participation in increased value, or excluded entirely. The mixing analysis under the default regime deserves separate treatment because mixed-funding scenarios produce some of the most technically complex disputes in property settlement files. Where the spouse used personal-channel funds together with marital income to fund a single acquisition, the asset is treated as partially personal and partially acquired in proportion to the funding contributions, with the participation calculation applying only to the acquired portion. Where the personal-channel and acquired-channel contributions cannot be cleanly separated because the funds were commingled in a single account before the acquisition, the file faces a presumption-vs-proof question that the spouse claiming personal-channel character must rebut through documentary segregation. The standard approach is to maintain separate accounts for personal-channel funds where possible during marriage; where this discipline was not followed during marriage, the post-separation forensic reconstruction attempts to restore the segregation through dated bank-statement analysis showing which deposits funded which subsequent withdrawals.

6) Evidence Collection, Interim Measures and Expert Reports

A lawyer in Turkey advising on evidence collection will explain that the discipline must be planned before the first hearing because many assets change hands quickly once separation is known. The procedure ordinarily requires starting with official registries (Tapu Müdürlüğü extracts for real estate, Ticaret Sicil Müdürlüğü extracts for companies, traffic registration records for vehicles), then proceeding to banking (full statements for key accounts with salary inflows and outgoing payments matching acquisitions), then employment and social security evidence where income tracing is disputed, then contract evidence (sale agreements, loan agreements, lease agreements explaining large transfers). Each document is tied to a date because the date determines whether the asset falls inside the regime period; each document is tied to a custodian because custody shows where the original can be obtained if authenticity is challenged. Where one spouse controls key documents, each request and each response (including silence and refusal) is recorded as evidential foundation for court-assisted disclosure motions before the Aile Mahkemesi.

An Istanbul Law Firm coordinating ihtiyati tedbir (interim injunction) requests will explain that interim measures preserve the marital pool's value where credible dissipation risk exists. The procedure ordinarily requires the request to identify specific assets (with TAPU references for real estate, account identifiers for bank accounts, share details for company interests), demonstrate the dissipation risk through documented events (recent transfers, unusual withdrawals, refusal to disclose documents that should exist), propose a feasible implementation path (because orders that cannot be implemented are ineffective), and address proportionality concerns. Real estate protections typically take the form of registry annotations alerting third parties; bank protections take the form of targeted freezing orders requiring specific account identifiers; company-share protections require coordination with the corporate share ledger and Ticaret Sicil Müdürlüğü records. Practice may vary by authority and year. The discipline outlined in our note on precautionary attachment basics covers the underlying conceptual framework for asset preservation requests.

Turkish lawyers who manage the bilirkişi raporu (expert report) framework will note that expert evidence is central in property settlement cases because courts often need technical assistance to value assets and reconstruct cash flow. The procedure ordinarily requires ensuring the expert mandate matches the legal questions in dispute (separating classification questions, valuation questions and tracing questions); providing the expert with complete bank statements rather than summaries; supplying registry extracts and purchase contracts for ownership and acquisition dates; supplying company financial statements and ledgers where business value is contested; supplying loan documents and repayment trails where debt allocation is contested; and coordinating site inspection access for real estate where the expert needs to view the property. After report filing, the parties read the report as a method document checking documented inputs, valuation methodology fit, correct dates, gross-vs-net distinction, and treatment of debts and transfers; objections cite specific exhibit numbers rather than generalized disagreement, and supplemental questions are narrow to avoid scope creep that delays the proceeding. The objection-pleading architecture itself deserves separate planning because the document operates as the file's principal opportunity to challenge unfavorable expert findings before judgment. The standard approach structures the objection around four discrete categories: documentary omissions where the expert failed to consider exhibits actually filed; methodological errors where the expert applied incorrect valuation methodology to the asset type; dating errors where the expert used an incorrect valuation date; and inferential errors where the expert drew conclusions inconsistent with the documentary record. Each category produces specific remedial requests — production of overlooked exhibits with targeted re-evaluation, supplemental expert analysis applying corrected methodology, recalculation using the legally appropriate dates, or substitute conclusions consistent with the corrected factual base. Practice may vary by authority and year, and the objection-pleading discipline determines whether the expert's preliminary findings translate into the final judgment unchanged or whether they are revised through the supplementary expert process the court typically permits where well-founded objections are filed.

7) Settlement Negotiation Strategy and Court Procedure

An English speaking lawyer in Turkey advising on settlement negotiation will explain that settlement works best when both spouses agree on the asset universe before they argue about shares — exchanging a written inventory listing every bank account, property, vehicle and business interest with identifiers, then exchanging key supporting proofs (Tapu extracts, bank statements, Ticaret Sicil Müdürlüğü records) so the inventory is verifiable. Where either side refuses disclosure, negotiation is treated as premature and the file shifts to targeted court-assisted disclosure requests. Settlement drafting then proceeds as a transfer plan rather than a narrative compromise: each asset described with registry identifiers, account identifiers and share ratios so implementation is mechanical; each debt listed with creditor name and supporting documents for transparent net calculation; each payment obligation specifying currency, payment channel and proof standard; each real estate transfer identifying Tapu Müdürlüğü appointment preparation steps; each bank-asset division identifying bank letter and instruction steps; each company-share division identifying corporate approval and share ledger update process. The structural choice between division and buyout deserves separate negotiation focus because the choice determines both the immediate cash-flow impact on each spouse and the long-term operational complexity of the post-divorce relationship. Division produces continued co-ownership that requires either ongoing coordination (for income-generating real estate) or eventual sale (for non-productive holdings); buyout produces complete separation but requires the buying spouse to fund the buyout amount through cash on hand, financing secured against the asset, or installment-payment commitment. Where the buying spouse cannot fund the buyout cleanly, hybrid structures combining partial buyout with continued co-ownership can produce executable settlements that purer structures cannot achieve. The structural choice should be tested against execution feasibility at the negotiation stage rather than after the settlement is signed, because settlement structures that cannot actually be implemented through the relevant institutions produce post-settlement disputes that consume the goodwill the negotiation generated. The execution-feasibility analysis is therefore an integral part of negotiation strategy rather than a downstream operational concern, and the spouse-side counsel who anticipates execution friction during drafting produces materially more durable settlements than counsel who treats execution as a discrete post-signing exercise.

A Turkish Law Firm coordinating the court-procedure layer will explain that property liquidation disputes are usually handled through a separate procedural track from the divorce decree even when both move in parallel before the Aile Mahkemesi. The procedure ordinarily requires defining the claim type and requested relief at the outset, identifying which documents must be obtained through court orders because voluntary disclosure is unlikely, requesting early identification of the property regime and key disputed assets so expert work is not wasted, and building a hearing file with index, chronology and asset cross-reference table. Courts rely heavily on written submissions, so late and inconsistent filings harm credibility; party-side timing is managed through document readiness rather than through optimistic calendar assumptions. The discipline outlined in our note on family law in Turkey covers the general procedural environment within which the property liquidation case operates.

Turkish lawyers who handle the parallel divorce-and-property-file consistency requirements will note that inconsistent statements between the two files create credibility problems for both. Where the divorce file contains admissions about ownership or funding, the property file should address them with documents rather than denial; where the divorce file contains temporary housing arrangements, the property file should document how those arrangements affect use and value calculations. Courts typically separate emotional conflict from financial accounting, so pleadings remain technical and evidence-based; when the other side raises irrelevant allegations, the response redirects to the asset schedule and proof chain rather than engaging the irrelevant material. Where translations are needed between Turkish and the foreign spouse's language, source and translation are kept together with consistent identity-token spelling. Practice may vary by authority and year, and procedural discipline produces final judgments that are clearer and easier to enforce than judgments emerging from chaotic procedural environments. The appellate-review architecture also depends on procedural-discipline at the trial level because appellate review (istinaf before the Bölge Adliye Mahkemesi and temyiz before the Yargıtay where applicable) is limited to the file as documented at trial. Where the trial file contains comprehensive evidence pack, indexed exhibits, dated chronology and reasoned objections to expert findings, the appellate court can review the substantive analysis on a complete record; where the trial file is fragmented, late-filed or inconsistent, the appellate court typically defers to trial-level findings even where the underlying analysis was incorrect because appellate review cannot substitute its own factual conclusions for the trial court's where the record does not support reversal. The standard approach in property settlement files where appellate exposure is anticipated — typically high-value cases where either spouse is likely to appeal an unfavorable allocation — is to maintain trial-level documentary discipline at the level required for appellate scrutiny rather than at the minimum required for trial-level success.

8) Judgment Enforcement and Compliance Roadmap

A lawyer in Turkey advising on judgment enforcement will explain that the property judgment must translate the asset schedule into clear allocation and payment obligations executable through the İcra ve İflas Kanunu's enforcement framework. The procedure ordinarily requires the judgment to identify which assets are included in the marital pool, how the balancing claim is calculated, the registration steps required for asset transfers, and the payment terms for any monetary balancing claim. Where the judgment is unclear on identifiers, execution becomes harder because banks and Tapu Müdürlüğü offices need precise references; party-side review of draft reasoning and expert reports therefore objects to ambiguity with exhibit citations rather than accepting unclear language that produces enforcement disputes later. Where the judgment orders transfer of a specific asset, the creditor spouse must prove identity and authority for the registry steps; where the judgment orders a balancing payment, the creditor spouse must trace debtor assets for collection through the İcra Dairesi enforcement mechanism.

An Istanbul Law Firm coordinating the enforcement architecture will note the parallel between settlement and judgment enforcement: both require the same execution-language discipline. The procedure ordinarily requires opening an icra (execution) file with the competent İcra Müdürlüğü, serving the debtor with the demand, navigating any debtor objection through the procedural steps that apply to judgment-based execution, and coordinating with the relevant institution (Tapu Müdürlüğü for registry transfer, banks for account-balance attachment, Ticaret Sicil Müdürlüğü for share-related steps). Each step produces documentary receipts and service proofs preserved against later dispute about timing and service. Where the debtor spouse has heavy debt, unstable income or an insolvent business, enforcement planning considers whether ordinary attachment will be effective or whether insolvency proceedings will intervene; where insolvency proceedings begin, the creditor spouse may need to register the claim and follow the insolvency timetable rather than rely on ordinary execution. The discipline outlined in our note on enforcement proceedings in Turkey covers the underlying execution-procedure framework.

Turkish lawyers who design comprehensive property settlement compliance roadmaps will treat the program as a sequence rather than as discrete events. The roadmap begins with confirming the marriage timeline and fixing the governing property regime in writing; proceeds through asset schedule construction with identifiers, debt schedule construction with creditor names and supporting documents, tracing timeline linking major assets to bank inflows and outflows, valuation plan separating real estate, business and cash methods for expert audit, ihtiyati tedbir analysis based on documented dissipation risk, targeted disclosure motion preparation for records controlled by the other spouse, settlement framework drafting with executable allocation rather than only percentages, and parallel enforcement planning so the final structure is collectible and registrable. Throughout, pleadings remain factual and exhibit-linked because courts decide from what is proven rather than from what is asserted. After settlement or judgment, execution is managed through checklists covering Tapu Müdürlüğü appointment preparation, bank instruction sequences, corporate share-ledger updates, debt allocation receipts, ongoing maintenance arrangements during transfer windows, and post-judgment folder maintenance documenting each compliance step. Practice may vary by authority and year. The execution-language discipline applied at the drafting stage produces materially different post-judgment outcomes from the execution-language discipline applied only after enforcement disputes arise. Where the settlement or judgment articulates each transfer step in execution-ready format — registry references with full TAPU identification (province, district, neighborhood, parcel and independent unit numbers); bank account references with full IBAN and account holder identification; share references with corporate registration number, share class and number; payment references with currency, amount, payment channel and proof requirement — the execution office can implement the obligations through standard procedural sequences without reopening substantive merits. Where the language is general or descriptive ("the family home," "the joint accounts," "the company shares") without execution-ready identifiers, the execution office typically returns the file for clarification, producing additional procedural friction that can extend the post-judgment timeline by months and create opportunities for the debtor spouse to dissipate assets while clarification proceeds.

9) Frequently Asked Questions for Spouses and International Clients

- What is property settlement in Turkish divorce? Property settlement is the financial liquidation of the marital property regime under the Türk Medeni Kanunu — the systematic accounting of assets, debts and compensatory claims that follows divorce. It can proceed either through a separate liquidation case (mal rejimi tasfiyesi davası) before the Aile Mahkemesi or through a settlement agreement negotiated by the parties.

- What property regimes does Turkish law recognize? Four: edinilmiş mallara katılma rejimi (the default participation in acquired property regime), mal ayrılığı rejimi (separation of property), paylaşmalı mal ayrılığı rejimi (separation of property with sharing), and mal ortaklığı rejimi (community of property). Spouses can select an alternative through a written agreement before a Turkish notary; absent such agreement, the default regime applies automatically.

- What does the default regime require? The edinilmiş mallara katılma rejimi distinguishes acquired property (assets obtained during marriage through marital effort or income) from personal property (pre-marital assets, gifts, inheritances, certain personal-use items, non-pecuniary damages). Each spouse retains personal property; each is entitled to participate in half the net value of the other's acquired property after deductions.

- When does the property regime end? The regime ends on the date of divorce filing rather than the date of separation or the date of judgment. Asset acquisition and funding flows after the filing date generally fall outside the marital pool; the precise valuation date for individual assets may differ from the regime-ending date depending on asset category.

- How is acquired vs. personal classification proven? Through documentary chains connecting each asset to its acquisition evidence, then to its funding evidence, then to a classification memorandum stating which category the asset falls into and why. Courts decide classification on traceability rather than on labels or fairness arguments.

- What are the most common hidden asset patterns? Repeated cash withdrawals reducing visible bank balances; transfers to close relatives presented as loan repayments or gifts; sudden ownership shifts of vehicles or shares to third parties while the spouse retains control; sales below market with unexplained discounts; and operational concealment in business families through company-account personal expenses labeled as business costs.

- How is real estate valued? Through indexed valuation packs covering legally relevant valuation date, occupancy and lease status, encumbrance profile, renovation contribution analysis, comparable sales evidence, and expert appraisal applying methodology appropriate to property type. Site complex restrictions, common-area fees and zoning constraints affect market value and require documentation.

- How are bank accounts reconstructed after separation? Through full statement coverage for the entire regime period, cash-flow timelines tying each major inflow and outflow to dated supporting evidence, matching of salary inflows to employment records, labeling of family-member transfers with descriptions and correspondence, and reconciliation of cash-flow timeline against asset acquisitions.

- How are company interests valued? Through the legal form identification (anonim şirket shares, limited şirket payı, partnership interest, sole proprietorship), Ticaret Sicil Müdürlüğü extracts and shareholder register records, financial statement and ledger inputs, customer contract evidence, and expert valuation methodology fit to the business model. Real estate held by the company is separated to avoid double counting.

- How are gifts and inheritances treated? As personal property (kişisel mal) excluded from the marital pool — provided the gift or inheritance is documented through donor transfer evidence (or probate and estate distribution records for inheritances) and the funds are traced through the receiving account into any subsequent acquisition the claimant attributes to the personal source.

- What are ihtiyati tedbir (interim injunction) measures? Court-ordered protections preserving marital pool value where credible dissipation risk exists. Real estate annotations alert third parties; bank freezing orders block transfers from specified accounts; company-share protections coordinate with corporate share ledgers and Ticaret Sicil Müdürlüğü records. Each request requires specific asset identification, documented risk evidence, and feasible implementation path.

- What is the bilirkişi raporu (expert report) framework? Court-appointed expert analysis where the proceeding requires technical assistance for asset valuation, cash-flow reconstruction or business-value determination. The expert mandate separates classification, valuation and tracing questions; the parties supply complete documentary inputs rather than summaries; objections cite specific exhibit numbers rather than generalized disagreement.

- How is the property settlement case scheduled? Through the Aile Mahkemesi's docket, which is separate from the divorce decree procedure even when running in parallel. Timing depends on document readiness, expert availability and court workload rather than on fixed calendars; party-side timing management focuses on submitting complete inputs early to avoid postponements.

- How is the property judgment enforced? Through the İcra ve İflas Kanunu's enforcement framework: opening an icra file with the competent İcra Müdürlüğü, serving the debtor with the demand, navigating debtor objections through judgment-based execution procedure, and coordinating with the relevant institution for registry transfer, account attachment or share-related steps.

- Does ER&GUN&ER Law Firm advise foreign spouses on Turkish property settlement? Yes. ER&GUN&ER Law Firm is an Istanbul-based law firm advising foreign spouses, expatriates and cross-border families on the complete property settlement lifecycle, including marital property regime determination under the Türk Medeni Kanunu, edinilmiş vs. kişisel mal classification analysis, asset inventory and tracing discipline including hidden asset techniques, real estate and business valuation coordination, evidence collection and bilirkişi raporu review, ihtiyati tedbir applications for asset preservation, settlement negotiation and drafting, court procedure before the Aile Mahkemesi, and judgment enforcement under the İcra ve İflas Kanunu — with English-language client communication and bilingual documentation throughout each engagement. Files in this area are typically led personally by the managing partner rather than delegated.

Author: Mirkan Topcu is an attorney registered with the Istanbul Bar Association (Istanbul 1st Bar), Bar Registration No: 67874. His practice focuses on cross-border and high-stakes matters where evidence discipline, procedural accuracy, and risk control are decisive.

He advises foreign spouses, expatriates and international families on Turkish property settlement in divorce under the Türk Medeni Kanunu, including marital property regime determination across the four regimes (edinilmiş mallara katılma, mal ayrılığı, paylaşmalı mal ayrılığı, mal ortaklığı), acquired versus personal asset classification, asset inventory and tracing across cross-border financial structures, hidden asset analysis and dissipation risk management, real estate and business valuation coordination, bilirkişi raporu (expert report) framework management, ihtiyati tedbir (interim injunction) applications for asset preservation, settlement negotiation and execution-language drafting, court procedure before the Aile Mahkemesi (Family Court), and judgment enforcement under the İcra ve İflas Kanunu before the İcra Müdürlüğü with coordinated registry, banking and corporate-share execution sequencing.

Education: Istanbul University Faculty of Law (2018); Galatasaray University, LL.M. (2022). LinkedIn: Profile. Istanbul Bar Association: Official website.