A lawyer in Turkey who advises on inheritance tax understands that when heirs and executors ask about inheritance tax rates Turkey they are usually looking for a number, but the correct professional answer is a method: determine the taxable transfer, establish the recognized valuation basis for each asset class, identify the applicable relationship category, apply the tariff and allowances verified for the relevant year from primary sources, then follow the declaration and payment rules. An Istanbul Law Firm that advises on inheritance and gift tax Turkey matters provides the integrated guidance covering every stage of this process: mapping the estate assets to identify the taxable base; classifying each heir's relationship to the deceased under the framework applicable to the relevant year; establishing the recognized valuation basis for each asset type; preparing the declaration as an indexed evidence pack rather than a form with unsupported numbers; managing the filing and follow-up process with the tax administration; coordinating bank and land registry release with the tax compliance steps; addressing double taxation concerns where the same transfer is taxed in another country; and managing gifts and lifetime transfers whose tax treatment runs parallel to the inheritance framework. A Turkish Law Firm that advises on inheritance tax matters understands that the filing rate is not the most important professional variable—the most important variable is the quality of the evidence pack, because most rejections, delays, and follow-up requests arise from mismatched identity tokens, missing legalization steps, and inconsistent asset descriptions rather than from complicated legal questions. An English speaking lawyer in Turkey who advises on inheritance tax for cross-border estates provides the bilingual coordination that prevents the inconsistencies between Turkish and foreign documentation that cause avoidable delays at tax offices, banks, and land registries. Practice may vary by authority and year — verify current Turkish inheritance tax tariffs, current allowances, and current declaration deadlines from primary official sources before taking any action in a Turkish inheritance tax matter, since tariff schedules and allowances applicable to Turkish inheritance and gift tax can be updated annually and must be confirmed for the specific year of the transfer and the specific relationship category applicable to each heir. Practice may vary by authority and year.

Turkish Inheritance Tax Framework: Structure, Applicable Law and Key Concepts

A lawyer in Turkey who advises on the Turkish inheritance tax framework explains that inheritance and gift taxation in Turkey operates under the Inheritance and Gift Tax Law, which covers both transfers that occur by death and certain gifts made during a person's lifetime—and that the system's core structure connects taxable base determination, relationship classification, and year-verified tariff and allowance application as sequential steps whose correct execution determines both the amount payable and the administrative path to asset release. An Istanbul Law Firm that advises on the inheritance and gift tax Turkey framework helps heirs and executors understand the specific framework most important for each estate profile: the taxable event is the acquisition of assets by heirs or beneficiaries rather than the death itself; the declaration is built around an asset-by-asset inventory and valuation rather than a single estate total; each heir is treated as a separate taxpayer lane with their own relationship category, valuation allocation, and allowance calculation; and the declaration must match both the succession file—the inheritance certificate and civil registry records—and the underlying asset ownership records at banks, land registries, and corporate registries. Turkish lawyers advising on inheritance tax framework help heirs understand that a numeric tariff table without the associated valuation basis, relationship classification, and year-specific verification is not operationally useful—because the tariff tells you what percentage to apply but not to what number, which category, or for which year—and that the most common source of inheritance tax processing delays is not the complexity of the tariff calculation but the incomplete or inconsistent documentation of the taxable base whose reconstruction after initial filing creates avoidable follow-up cycles. Practice may vary by authority and year.

An Istanbul Law Firm that advises on the inheritance tax basics for cross-border estates explains that separating civil succession rules from tax computation rules is essential for building a coherent file—because civil succession determines who inherits and in what shares under Turkish succession law and taxes, while the tax computation determines how the taxable base is established for each heir based on the recognized valuation rules and the applicable year's tariff schedule. Turkish lawyers advising on inheritance tax fundamentals help heirs implement the specific file structure most effective for each estate: each heir's profile should include identity documents, address proof, relationship evidence, and any representation authority if a proxy acts; the asset list should be built tab-by-tab with official identifiers copied from source records rather than retyped; the valuation method for each asset class should be documented in a method memo citing the specific valuation reference used; and the declaration narrative should be evidence-led rather than conclusion-driven. An English speaking lawyer in Turkey who advises on inheritance tax file design for cross-border estates provides the bilingual management that keeps the Turkish-side declaration consistent with any foreign-side filings—preventing the asset characterization inconsistencies and share discrepancies that create audit questions in both jurisdictions, and maintaining the master token sheet that ensures the same person's name appears consistently across Turkish and foreign documentation regardless of how many separate translations are prepared. Practice may vary by authority and year.

A Turkish Law Firm that advises on downstream office requirements for inheritance tax compliance explains that many heirs underestimate how tightly the tax compliance process is linked to asset release—because banks typically require documentation showing that the tax declaration process is being addressed before releasing estate account funds, and land registries typically require documentation showing that inheritance tax obligations have been declared before completing title transfer registrations. An English speaking lawyer in Turkey who advises on integrated inheritance tax and asset release planning for foreign nationals helps heirs understand that the tax file and the bank release file and the land registry file should be built simultaneously from the same evidence base rather than sequentially—so that each institution sees consistent heir identities, consistent asset descriptions, and consistent share allocations without the contradictions that arise when different family members assemble separate document packs for different institutions. Practice may vary by authority and year.

Determining the Taxable Base: Asset Inventory, Valuation Methodology and Relationship Categories

A lawyer in Turkey who advises on taxable base determination explains that the taxable base for inheritance and gift tax Turkey is built asset by asset and heir by heir—and that the practical starting point is always the estate inventory whose completeness and accuracy determines whether the declaration can be filed without follow-up requests. An Istanbul Law Firm that advises on estate inventory design for inheritance tax purposes helps executors implement the specific inventory approach most effective for each estate: listing every Turkish asset class—real estate, bank accounts, securities, vehicles, business interests, and receivables—with the official identifier for each asset copied from source records; mapping each asset to its recognized valuation methodology whose result will form the declared value; confirming which assets are located in Turkey for situs analysis; and documenting any liabilities or encumbrances that may be relevant to deductions analysis. Turkish lawyers advising on estate inventory management help heirs understand that the inventory's accuracy is the foundation of the entire declaration—because an asset omitted from the inventory will surface later when banks or registries are accessed and create correction work at that stage rather than at the declaration stage, and because each corrective declaration filed after the initial filing generates a correspondence trail that extends the overall administration timeline. Practice may vary by authority and year.

An Istanbul Law Firm that advises on valuation methodology for inherited property Turkey explains that each asset class has its own recognized valuation reference whose use in the declaration is essential for producing a defensible taxable base. Turkish lawyers advising on valuation methodology help heirs implement the specific approach most appropriate for each asset type: for real estate, using the official valuation reference recognized for tax and registry purposes rather than a market appraisal which may differ from the recognized statutory basis; for bank accounts, obtaining bank-issued balance confirmations showing account ownership and the balance at the relevant reference date; for securities, obtaining custody statements or brokerage confirmations showing holdings and values with visible date headers; and for business interests, preserving share registers and company financials that support the declared value without unsupported formulas. An English speaking lawyer in Turkey who advises on valuation methodology for cross-border estates provides the coordination that ensures Turkish asset values are documented in a format whose terminology and reference basis is consistent with any parallel foreign-side valuation processes—preventing the inconsistencies between Turkish and foreign declared values that create audit risk in both jurisdictions, and confirms that each valuation basis used in the Turkish declaration is supported by an objective exhibit rather than an informal estimate that cannot be verified by a tax office reviewer. Practice may vary by authority and year.

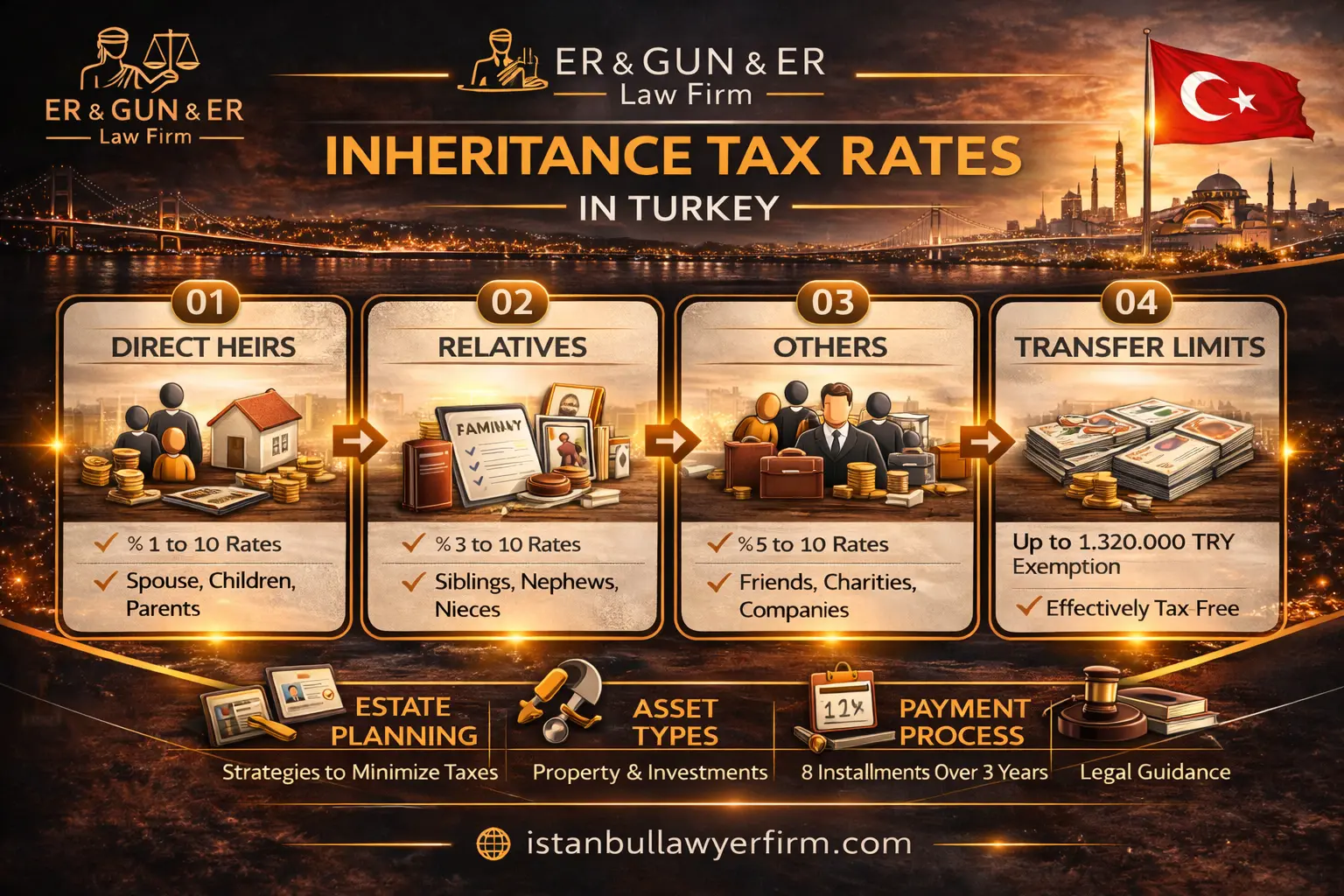

A Turkish Law Firm that advises on relationship categories in inheritance tax proceedings explains that the applicable tariff schedule and the available allowances for a specific year are typically keyed to the legal relationship between the deceased and the heir or between the donor and the donee—and that correctly classifying each relationship is both a substantive legal task and a documentary task whose failure produces an incorrect taxable base regardless of how accurately the assets are valued. An English speaking lawyer in Turkey who advises on relationship classification for foreign heirs implements the specific evidence approach most effective for each heir profile: proving the relationship with official civil status documents—marriage certificates, birth records, adoption documents—rather than family narratives; ensuring that foreign civil documents proving the relationship are apostilled or consularly legalized and provided in certified Turkish translation with consistent name spellings; and creating an heir profile page for each heir that consolidates the identity, address, and relationship evidence in one indexed tab. Practice may vary by authority and year — verify the current applicable tariff schedule and current allowance amounts from primary official sources for the specific year of the transfer before completing any taxable base calculation, since both tariff brackets and allowance amounts applicable to Turkish inheritance and gift tax can be updated on an annual basis and must be confirmed from current official guidance rather than from prior-year summaries. Practice may vary by authority and year.

Residency, Situs Rules and Foreign Heirs: Cross-Border Scope and Documentation

A lawyer in Turkey who advises on residency and situs rules for inheritance tax explains that the scope of Turkish inheritance tax depends on both where assets are located and the residency and nationality status of the deceased and heirs—and that inheritance tax for foreigners in Turkey is commonly experienced as a situs question whose answer determines which assets are within the Turkish tax file's scope and what documentation is required to address the obligation. An Istanbul Law Firm that advises on cross-border inheritance tax scope helps families implement the specific analysis most appropriate for each cross-border profile: identifying the deceased's residence status and the heirs' residence status through official documentation rather than informal statements; confirming which assets are Turkish-situs—real estate registered in Turkey, Turkish bank accounts, and Turkish securities—whose treatment under the Turkish declaration framework must be addressed; and identifying any foreign assets that may require coordination with foreign tax authorities rather than inclusion in the Turkish declaration. Turkish lawyers advising on situs and residency analysis help families understand that a coherent cross-border estate file separates Turkish-situs documentation from foreign-situs documentation while maintaining consistent asset descriptions and heir identities across both sides. Practice may vary by authority and year.

An Istanbul Law Firm that advises on foreign document requirements for Turkish inheritance tax proceedings explains that foreign heirs and foreign civil events—deaths, marriages, births—that occurred outside Turkey create a specific documentation challenge: Turkish offices require the relevant foreign records to be made usable through apostille or consular legalization followed by certified Turkish translation—and that starting this pipeline early is the single most effective action for preventing timeline delays in cross-border estates. Turkish lawyers advising on foreign document preparation help heirs implement the specific pipeline approach most effective for each document type: confirming the applicable legalization method—apostille or consular—based on the issuing country; obtaining the long-form certified copy from the issuing authority rather than a short extract that omits seals and identifiers; keeping the source document, legalization pages, translation, and notary declaration as a single indexed bundle; and applying a master token sheet that defines how each name and date appears in Turkish across all translations. An English speaking lawyer in Turkey who manages the foreign document pipeline for cross-border inheritance tax proceedings provides the systematic tracking that converts the pipeline from a conceptual plan into an executed archive—preventing the missing-page rejections and name drift that are the most common preventable causes of delay. Practice may vary by authority and year.

A Turkish Law Firm that advises on double taxation inheritance Turkey concerns explains that when two or more countries assert taxing rights over the same transfer—most commonly when the deceased was resident or domiciled in a foreign country while also holding Turkish-situs assets—the double taxation exposure must be managed through careful documentation rather than assumed to be resolved by treaty. An English speaking lawyer in Turkey who advises on double taxation management for cross-border estates implements the specific coordination approach most effective for each cross-border profile: identifying which jurisdictions assert taxing rights through legal analysis of each country's applicable framework; building a master asset inventory that uses consistent asset descriptions in both the Turkish declaration and any foreign filings to prevent the characterization inconsistencies that trigger audit questions; and preserving foreign assessment documents and payment receipts in certified translation as the documentary basis for any credit or relief claim available under applicable instruments. Practice may vary by authority and year.

Filing the Inheritance Tax Declaration: Document Pack Design and Completeness Audit

A lawyer in Turkey who advises on the inheritance tax declaration Turkey process explains that the declaration should be treated as an indexed evidence pack rather than a form with unsupported numbers—and that the quality of this pack, including its internal consistency and completeness, determines whether the filing proceeds smoothly or generates a sequence of follow-up requests from the tax administration. An Istanbul Law Firm that advises on declaration pack design for inheritance tax filings helps executors implement the specific filing approach most effective for each estate profile: beginning the pack with the inheritance certificate and heir identity documents that establish who the heirs are and their shares; building each subsequent section around the asset tabs whose valuation proofs link to the inventory; including relationship evidence for each heir that confirms the classification applicable to their tariff computation; adding any deduction documentation for recognized liabilities or costs supported by objective exhibits; and including a cover memo that states the factual timeline in neutral terms and points to the key exhibits by number. Turkish lawyers advising on declaration pack design help executors understand that the declaration narrative should be evidence-led—meaning each assertion about an asset, a value, or a relationship is supported by the exhibit it references—rather than conclusion-led, because unsupported conclusions invite the clarification requests that extend the filing process. Practice may vary by authority and year.

An Istanbul Law Firm that advises on pre-filing completeness audits for inheritance tax declarations explains that running a structured completeness check before submission consistently reduces the number of post-filing follow-up requests—because most follow-up requests arise from the same preventable deficiencies: missing valuation exhibits for specific asset lines; share allocations in the declaration that differ from the inheritance certificate; name spellings in the translated foreign documents that differ from the Turkish-side identity records; and scope inconsistencies where assets visible at banks or registries are absent from the declaration. Turkish lawyers advising on pre-filing audits help executors implement the specific check most effective for each estate: confirming that every asset line has a valuation proof exhibit; confirming that heir shares in the declaration exactly match the inheritance certificate; confirming that all names and identifiers are consistent across identity documents and declaration fields through the master token sheet; and confirming that foreign documents have been legalized and translated with consistent token application. An English speaking lawyer in Turkey who conducts pre-filing audits for cross-border inheritance tax declarations provides the bilingual consistency check that confirms the Turkish declaration and any parallel foreign filings are using the same asset descriptions and heir identifications—preventing the contradictions that create audit questions in both jurisdictions. Practice may vary by authority and year.

A Turkish Law Firm that advises on post-filing follow-up management for inheritance tax declarations explains that after submission the case becomes a follow-up management exercise—and that treating each tax administration request as a formal ticket with an indexed supplement response is significantly more efficient than treating it as an open-ended inquiry. An English speaking lawyer in Turkey who manages post-filing follow-up for cross-border inheritance tax declarations implements the specific response approach most effective for each request type: building the supplement response as a compact indexed pack that addresses the specific request rather than re-submitting the entire declaration; including a short cover memo that states which request is being addressed and which exhibits respond to which element; and preserving the original request and the complete response as dated exhibits in the file so later bank and registry requests asking for evidence that the tax process is being managed can be answered promptly. Practice may vary by authority and year.

Payment, Installment Management and Bank and Registry Release

A lawyer in Turkey who advises on inheritance tax payment Turkey explains that payment management should be treated as a receipt-and-reference workflow linked to the official assessment or declaration record rather than as a calculation exercise—and that the specific payment amounts, schedules, and installment arrangements applicable to any inheritance tax obligation must be verified from the official assessment or instruction document for the specific case rather than from general summaries whose figures may reflect a different year or different circumstances. An Istanbul Law Firm that advises on inheritance tax payment management helps heirs implement the specific payment approach most effective for each payment situation: storing the official payment instructions or assessment communications as the primary reference documents; preserving every payment receipt including reference numbers, dates, and payer identity; maintaining a payment reconciliation memo that links each receipt to the relevant part of the assessment by exhibit reference; and keeping separate payment tabs per heir where multiple heirs pay separately or in different countries. Turkish lawyers advising on inheritance tax payment management help heirs understand that payment receipts are not only the evidence that a legal obligation has been satisfied but also a key exhibit in the bank release and land registry release packs that each institution will require. Practice may vary by authority and year — verify current payment procedures, current installment arrangements, and current confirmation formats with qualified counsel and from primary official sources before initiating any inheritance tax payment.

An Istanbul Law Firm that advises on bank and land registry release coordination explains that the practical challenge of inheritance tax payment is frequently not the payment itself but the sequencing of documentation that demonstrates to banks and registries that the tax compliance process has been addressed—and that preparing the bank release pack and the land registry pack before these institutions ask for it consistently produces faster asset access than assembling documents in response to institution-specific requests. Turkish lawyers advising on bank and registry release pack preparation help heirs implement the specific pack approach most effective for each institution type: for banks, including the declaration submission proof, any tax office assessment or acknowledgment, payment receipts, the inheritance certificate, and heir identity documents in a compact indexed order whose completeness the bank can verify against its own internal checklist; and for land registries, coordinating the inheritance tax documentation with the title transfer requirements and ensuring that the heir share allocations in the tax file match the inheritance certificate shares that the registry will use for the new registration. An English speaking lawyer in Turkey who coordinates bank and registry release for foreign heir estates provides the representative services that enable foreign heirs abroad to access estate accounts and complete title registrations without being physically present at each institution. Practice may vary by authority and year.

A Turkish Law Firm that advises on installment arrangements for inheritance tax obligations explains that installment payment options, where available under the applicable rules for the relevant year, still require the same documentation discipline as lump-sum payment—because each installment must be paid on the schedule reflected in the official documents and each payment must be receipted and preserved. An English speaking lawyer in Turkey who manages installment payment compliance for cross-border inheritance tax cases implements the specific compliance approach most effective for each multi-installment situation: recording the installment schedule as it appears in the official documents rather than from memory; maintaining a payment calendar as an internal tool based on official records; preserving proof of each installment payment in a dedicated receipts tab; and coordinating the installment timeline with the estate's bank access strategy so that heirs have the liquidity needed for each payment. The best lawyer in Turkey for inheritance tax matters for cross-border estates combines knowledge of the Turkish inheritance and gift tax framework, Turkish private international law applicable to cross-border estates, double taxation coordination, valuation methodology for each asset class, declaration filing and follow-up management, payment and installment compliance, bank and registry release procedures, and deductions and allowances analysis with the English-language communication that enables foreign heirs to manage their Turkish inheritance tax obligations effectively. Practice may vary by authority and year.

Double Taxation Concerns and Cross-Border Estate Coordination

A lawyer in Turkey who advises on double taxation inheritance Turkey concerns explains that when two or more countries assert taxing rights over the same transfer, the practical management approach is documentary rather than abstract—because any credit or relief mechanism available under an applicable treaty or domestic credit rule depends on specific documentary evidence of the tax paid in the other jurisdiction. An Istanbul Law Firm that advises on double taxation management for cross-border estates implements the specific coordination approach most effective for each multi-jurisdiction configuration: creating a cross-border asset inventory that uses consistent asset descriptions in both the Turkish declaration and any foreign filings; obtaining foreign tax assessments and payment receipts in certified Turkish translation as the evidentiary foundation for any applicable credit or relief claim; maintaining a cross-border timeline that records when each jurisdiction's declaration was filed and when assessments and payments were completed; and coordinating with foreign counsel to ensure that asset characterization and heir identification are consistent across all jurisdictions. Turkish lawyers advising on double taxation management help heirs understand that claiming credit or relief under an applicable bilateral instrument requires affirmative documentary action rather than passive assumption—and that failing to assemble the required foreign documentation prevents the credit mechanism from being applied even when it would otherwise be available. Practice may vary by authority and year.

An Istanbul Law Firm that advises on cross-border estate file coordination explains that the master asset inventory is the most important single document for managing cross-border inheritance tax coherently—because if Turkish and foreign filings characterize the same assets differently, describe heirs by different names, or allocate shares inconsistently, both tax administrations will generate follow-up questions whose resolution requires additional documentation in both jurisdictions simultaneously. Turkish lawyers advising on cross-border file coordination help heirs implement the specific master inventory approach most effective for each multi-jurisdiction estate: building one indexed asset list with consistent asset descriptions, then adapting the presentation format and valuation basis for each jurisdiction rather than creating separate inventories for each country; applying the same token sheet for name spellings in all translations so the same person is identified consistently in Turkish and foreign documentation; and maintaining a change log that records any correction to the inventory and propagates it to all jurisdictions' documentation. An English speaking lawyer in Turkey who coordinates cross-border inheritance tax filings for foreign nationals provides the liaison function that keeps Turkish and foreign counsel working from the same master inventory and the same heir identification—preventing the divergences that create parallel audit processes in different countries simultaneously. Practice may vary by authority and year.

A Turkish Law Firm that advises on the practical sequencing of cross-border inheritance tax steps explains that the order in which documentation is assembled and filings are completed across jurisdictions affects both the overall timeline and the risk of inconsistencies between Turkish and foreign documentation. An English speaking lawyer in Turkey who advises on cross-border inheritance tax sequencing implements the specific approach most effective for each estate: obtaining the core succession documents—death certificate, inheritance certificate, and asset proofs—in a form usable in both Turkish and foreign proceedings; filing the Turkish declaration within the applicable Turkish statutory deadline regardless of whether foreign proceedings are complete; coordinating the timing of foreign filings with the Turkish filing so that asset characterization decisions are made consistently; and preserving the complete evidence archive in a format that supports both any foreign audit of Turkish-declared values and any Turkish audit of foreign-declared values. Practice may vary by authority and year.

Deductions, Allowances, Gifts and Lifetime Transfer Planning

A lawyer in Turkey who advises on inheritance tax exemptions Turkey and deductions explains that each claimed deduction or allowance must be tied to a specific exhibit supporting both its legal basis and its factual existence—and that the phrase "inheritance tax exemptions Turkey" is best understood as a category of year-specific, relationship-specific, and evidence-dependent adjustments whose application to any specific estate requires verification from primary official sources for the relevant year rather than from general descriptions. An Istanbul Law Firm that advises on deductions and allowances management helps executors implement the specific approach most appropriate for each estate: identifying candidate deductions—documented liabilities, recognized estate administration costs, and applicable relationship allowances—through primary guidance verification; tying each candidate to a specific exhibit such as a debt agreement, court document, or official notice; separating estate-level deductions from heir-level allowances to prevent confusion and double-counting; and documenting in a deductions memo which adjustments are claimed, what legal basis applies, and which exhibit supports each one. Turkish lawyers advising on deductions management help executors understand that unsupported deduction claims are among the most common triggers for tax administration follow-up—and that a conservative, evidence-led approach to deductions consistently produces smoother declaration processing than maximizing claimed adjustments without documentation. Practice may vary by authority and year.

An Istanbul Law Firm that advises on gift tax rates Turkey and lifetime transfer planning explains that the inheritance and gift tax framework covers lifetime transfers as well as transfers by death—and that gifts and inter vivos transfers require a separate evidence file whose tax implications run parallel to but distinct from the inheritance tax file. Turkish lawyers advising on lifetime transfer documentation help clients implement the specific evidence approach most effective for each transfer type: proving the gift intention and the actual transfer completion through official transfer records—land registry transaction records for real estate gifts, bank transfer confirmations for cash gifts, and share ledger entries for company interest gifts; proving the donor-donee relationship with official civil status documents; proving the transferred asset's value using the recognized valuation reference for the relevant asset class; and keeping the gift file in a separate tab cross-referenced to the main estate file through the token sheet so that consistent identities and consistent asset descriptions connect both files. An English speaking lawyer in Turkey who advises on integrated lifetime transfer and inheritance planning for foreign nationals provides the coordinated planning that ensures lifetime transfers are documented in a way that is consistent with the eventual estate narrative—preventing the inconsistencies between how assets are described during lifetime and how they are described at inheritance that create audit questions. Practice may vary by authority and year.

A Turkish Law Firm that advises on the interaction between lifetime transfers and inheritance tax planning explains that heirs sometimes challenge lifetime gifts under civil law reserved share rules whose outcome can affect the inheritance tax narrative even though it does not change the tax method—and that maintaining clean, objective documentation for every lifetime transfer is the most effective protection against both civil challenges and tax audit questions. An English speaking lawyer in Turkey who advises on lifetime transfer evidence management for foreign nationals implements the specific archive approach most effective for each transfer type: preserving the complete transfer record—official transfer documents, bank receipts for any consideration, independent valuation evidence, and any capacity or independence context notes—as a dated exhibit set; maintaining a lifetime transfer register that lists all significant transfers with dates and proofs; and coordinating lifetime transfer documentation with the broader estate planning file so that the eventual inheritance declaration can incorporate the transfer history coherently. Practice may vary by authority and year — verify current applicable tariff schedules, current allowance amounts, and current deductible items from primary official sources for the specific year of any transfer before completing any taxable base calculation or filing.

A Turkish Law Firm that advises on the interaction between deductions and the declaration timeline explains that the decision to include a specific deduction should be made before the initial filing rather than added through a supplementary amendment—because each amendment to a filed declaration creates additional administrative correspondence whose volume can make the overall process less efficient than a well-prepared initial filing. An English speaking lawyer in Turkey who advises on deductions strategy for cross-border inheritance tax filings helps executors implement the specific approach that balances deduction completeness with declaration timeliness: filing within the deadline with all documented deductions; identifying any deductions whose evidence is pending and planning to obtain that evidence for any permitted amendments; and maintaining the deductions memo as a versioned document whose change history explains why specific items were included or excluded. Practice may vary by authority and year.

Probate Integration, Real Estate and Bank Account Compliance

A lawyer in Turkey who advises on the integration of inheritance tax with the probate process Turkey explains that the tax file cannot be reliably built until the succession position is officially established through the inheritance certificate—and that treating the probate process and the tax declaration as a single integrated file production exercise rather than two separate sequential processes is the approach that produces the fewest delays and the most consistent evidence across all institutional submissions. An Istanbul Law Firm that advises on integrated probate and inheritance tax file management helps executors implement the specific integration approach most effective for each estate: building the inheritance certificate application and the asset inventory simultaneously so that shares and asset descriptions are consistent from the beginning; using the issued inheritance certificate's heir list and share table as the direct input to the tax declaration's heir allocation; and preparing certified copies of the inheritance certificate in quantities sufficient for simultaneous submission to the tax office, each relevant bank, and the land registry rather than obtaining copies sequentially as each institution requests them. Turkish lawyers advising on probate and tax integration help executors understand that the token sheet applied to civil registry names in the probate file must be the same token sheet applied in the tax declaration and in the bank and registry submission packs—because a name spelling difference between the inheritance certificate and the bank declaration is treated by the bank as an identity discrepancy regardless of its obvious origin. Practice may vary by authority and year.

An Istanbul Law Firm that advises on real estate inheritance tax Turkey compliance explains that Turkish real estate is the asset class most likely to require coordination between the inheritance tax file and the land registry file—and that coordinating these two files from the beginning, rather than sequentially, prevents the situation where the land registry identifies a valuation or share discrepancy with the tax declaration after the registration appointment. Turkish lawyers advising on real estate inheritance tax compliance help heirs implement the specific approach most effective for each property situation: using the parcel identifier copied from the current title deed record rather than retyped in the asset inventory; confirming any encumbrances, annotations, or restrictions that affect both the valuation narrative and the transfer step; obtaining the recognized valuation reference for the property and documenting the basis in the valuation memo; and coordinating the inheritance tax payment documentation with the land registry's requirements for title transfer so that both are ready simultaneously. An English speaking lawyer in Turkey who advises on real estate inheritance tax compliance for foreign nationals manages the complete property succession file—from valuation documentation through tax declaration through land registry registration—as a coordinated sequence whose each step produces exhibits used in the next step. Practice may vary by authority and year.

A Turkish Law Firm that advises on bank account inheritance Turkey tax compliance explains that the bank account lane is where heirs most frequently experience the practical link between inheritance tax compliance and asset access—because Turkish banks typically require evidence that the inheritance declaration process is being addressed before they will provide account balance information or authorize fund transfers, and because heirs often need access to estate account funds to cover the costs of the administration including the tax obligation itself. An English speaking lawyer in Turkey who advises on bank account inheritance tax compliance for foreign nationals implements the specific approach most effective for each bank situation: preparing a bank release pack that combines the inheritance certificate, the tax declaration submission proof, any tax office acknowledgment or assessment, heir identity documents, and the specific bank's required checklist items in a compact indexed order; maintaining a bank communication log that records every interaction with dates, officer names, requests made, and documents provided; and coordinating the bank release timeline with the installment payment schedule so that account access does not create a liquidity problem that prevents timely tax payments. Practice may vary by authority and year — verify current Turkish inheritance tax declaration deadlines, current payment requirements, and current institutional documentation standards with qualified counsel before taking any action in the estate administration.

Frequently Asked Questions

- What determines inheritance tax rates in Turkey? Turkish inheritance tax rates are determined by a tariff schedule and allowance framework that depends on the year of the transfer, the legal relationship between the deceased and the heir, and the taxable base established through recognized asset valuation. Rates and allowances must be verified from primary official sources for the specific year of the transfer. Practice may vary by authority and year.

- How is the taxable base for Turkish inheritance tax calculated? The taxable base is built asset by asset using the valuation methodology recognized for each asset class under Turkish tax law—which may differ from market values. Real estate uses statutory valuation references; bank accounts use bank-issued balance confirmations; securities use custody statements with visible date headers. Recognized deductions and allowances verified for the relevant year are then applied to determine the final taxable base per heir. Practice may vary by authority and year.

- Do foreign nationals pay inheritance tax in Turkey? Yes. Turkish inheritance tax applies to Turkish-situs assets—including Turkish real estate and Turkish bank accounts—regardless of whether the heirs are Turkish or foreign nationals. The situs of each asset determines scope. Foreign heirs must prepare foreign documents through legalization and translation to participate in the declaration process. Practice may vary by authority and year.

- How should the inheritance tax declaration be filed? The inheritance tax declaration should be filed as an indexed evidence pack whose structure includes the inheritance certificate, heir identity documents, asset-by-asset valuation proofs, relationship classification evidence, and any supported deduction documentation. The declared values and shares must match the inheritance certificate and the underlying asset records. Pre-filing completeness audits consistently reduce post-filing follow-up requests. Practice may vary by authority and year.

- What documents do banks require before releasing estate accounts? Turkish banks typically require the inheritance certificate, inheritance tax declaration submission proof, any tax office assessment or acknowledgment, and heir identity documents before providing account information or authorizing fund releases. The specific combination of documents required by each bank may differ. Preparing a complete, indexed bank release pack before the bank interaction is consistently more efficient than assembling documents in response to bank requests. Practice may vary by authority and year.

- Are there inheritance tax exemptions or deductions available in Turkey? The Turkish inheritance and gift tax framework provides allowances and deductions that depend on the year, the relationship category, and the nature of the transfer. The specific allowance amounts and deductible items must be verified from primary official sources for the relevant year. Each claimed deduction must be supported by an objective exhibit demonstrating both the legal basis and the factual existence of the adjustment. Practice may vary by authority and year.

- What is the gift tax treatment for lifetime transfers in Turkey? The Turkish inheritance and gift tax framework covers certain lifetime transfers as well as transfers by death. Gift tax obligations are triggered at the time of transfer and require separate documentation including proof of transfer completion, donor-donee relationship evidence, and recognized asset valuation. Gift tax tariffs and allowances must be verified from primary official sources for the year of the transfer. Practice may vary by authority and year.

- How is double taxation managed when the same transfer is taxed in two countries? Double taxation in cross-border estates requires identifying which jurisdictions assert taxing rights, building a master asset inventory with consistent descriptions used in all jurisdictions' filings, obtaining foreign assessment and payment documentation in certified translation as the evidential basis for any available credit or relief, and coordinating timing between Turkish and foreign filings. Whether credit or relief is available depends on applicable bilateral instruments and domestic rules whose current applicability must be verified. Practice may vary by authority and year.

- What valuation methodology applies to inherited real estate in Turkey? Inherited Turkish real estate is valued using the official valuation reference recognized for Turkish tax and registry purposes, which may differ from market value or formal appraisals. The declared value should be documented through the applicable official source rather than an informal estimate. Parcel identifiers and property descriptions should be copied from the current title deed record to prevent identification errors. Practice may vary by authority and year.

- What is the Turkish probate process and how does it relate to inheritance tax? The Turkish probate process establishes heirship and share allocations through the inheritance certificate—veraset ilamı—issued by the Turkish Peace Court or notary. The inheritance certificate's share table directly feeds the inheritance tax declaration's heir allocation. Building the probate file and the tax declaration file simultaneously using the same asset descriptions and the same identity token sheet produces the most coherent combined evidence base. Practice may vary by authority and year.

- How should inheritance tax be coordinated with land registry title transfer? Land registry title transfer for inherited Turkish real estate requires inheritance tax documentation—typically declaration submission proof and tax compliance evidence—alongside the inheritance certificate and identity documents. Coordinating the tax file and the registry submission from the beginning, using consistent parcel identifiers and heir share allocations in both files, prevents the valuation or share discrepancies that create registry follow-up requests. Practice may vary by authority and year.

- What foreign documents are needed for Turkish inheritance tax proceedings? Foreign civil records—death certificates, marriage records, birth certificates—used in Turkish inheritance tax proceedings must typically be apostilled or consularly legalized and provided in certified Turkish translation. A master token sheet should be applied across all translations to ensure consistent name spellings. The source document, legalization pages, translation, and notary declaration should be kept as a single indexed bundle. Practice may vary by authority and year.

- Can inheritance tax obligations be paid in installments in Turkey? Installment payment arrangements may be available for Turkish inheritance tax obligations where the applicable rules for the relevant year permit them. The specific availability, schedule, and conditions for any installment arrangement must be verified from the official assessment or instructions for the specific case. Each installment payment must be receipted and preserved as a primary exhibit for downstream bank and registry release submissions. Practice may vary by authority and year.

- How does residency affect Turkish inheritance tax obligations for foreign heirs? Turkish inheritance tax applies to Turkish-situs assets regardless of whether the heir is resident in Turkey. The heir's residence status may affect communication procedures, address proof requirements for the declaration, and whether foreign tax credits are available under applicable bilateral instruments. Each heir's residency status should be documented through official records rather than informal statements. Practice may vary by authority and year.

- Does ER&GUN&ER Law Firm provide legal services for inheritance tax matters in Turkey? Yes. ER&GUN&ER Law Firm provides legal services for inheritance tax matters in Turkey including asset inventory design and valuation methodology advisory, relationship classification and allowance analysis, declaration pack preparation and pre-filing completeness audit, post-filing follow-up management, bank release pack coordination, land registry release coordination, payment and installment management, double taxation documentation and coordination, lifetime transfer and gift tax advisory, cross-border estate file coordination, foreign document legalization and translation management, and integrated probate and tax file management—with English-language client communication and bilingual documentation throughout each engagement.

Author: Mirkan Topcu is an attorney registered with the Istanbul Bar Association (Istanbul 1st Bar), Bar Registration No: 67874. His practice focuses on cross-border and high-stakes matters where evidence discipline, procedural accuracy, and risk control are decisive.

He advises individuals and companies across Immigration and Residency, Real Estate Law, Tax Law, and cross-border documentation matters where procedural accuracy and evidence discipline are decisive.

Education: Istanbul University Faculty of Law (2018); Galatasaray University, LL.M. (2022). LinkedIn: Profile. Istanbul Bar Association: Official website.