Source of funds verification is the practical process of proving where the money for a specific transaction came from. In Türkiye, the framework is set by Law No. 5549 on Prevention of Laundering Proceeds of Crime (Suç Gelirlerinin Aklanmasının Önlenmesi Hakkında Kanun) effective 11 October 2006, supplemented by the implementing Tedbirler Yönetmeliği and administered by the Financial Crimes Investigation Board (Mali Suçları Araştırma Kurulu, "MASAK") under the Ministry of Treasury and Finance. Banks, capital markets intermediaries, real estate professionals, notaries, and other obliged entities under Law 5549 are required to identify customers, verify identity, monitor transactions, and report suspicious activity to MASAK. The Turkish Penal Code (Law No. 5237) Article 282 criminalises laundering of proceeds of crime, with imprisonment of three to seven years. Banking supervision under the Banking Law (Law No. 5411) and the BDDK reinforces the AML obligations across the banking sector.

Source of funds verification is not a moral judgment about a customer; it is a documentation exercise linked to risk management. The core question is whether the funds can be traced through a coherent trail that a compliance reviewer can read. This guide addresses source of funds verification in an evidence-led way and reflects KYC requirements as a risk-based workflow. Practice may vary by authority and year — check current guidance. The same transaction can be treated differently across banks; the same client can be assessed differently across periods. The safest approach is to build the file before moving money. ER&GUN&ER Law Firm advises foreign investors, property buyers, citizenship-by-investment applicants, corporate transaction parties, and high-net-worth individuals on source of funds documentation, MASAK compliance positioning, bank dialogue management, and dispute resolution where transfers are held or accounts are restricted.

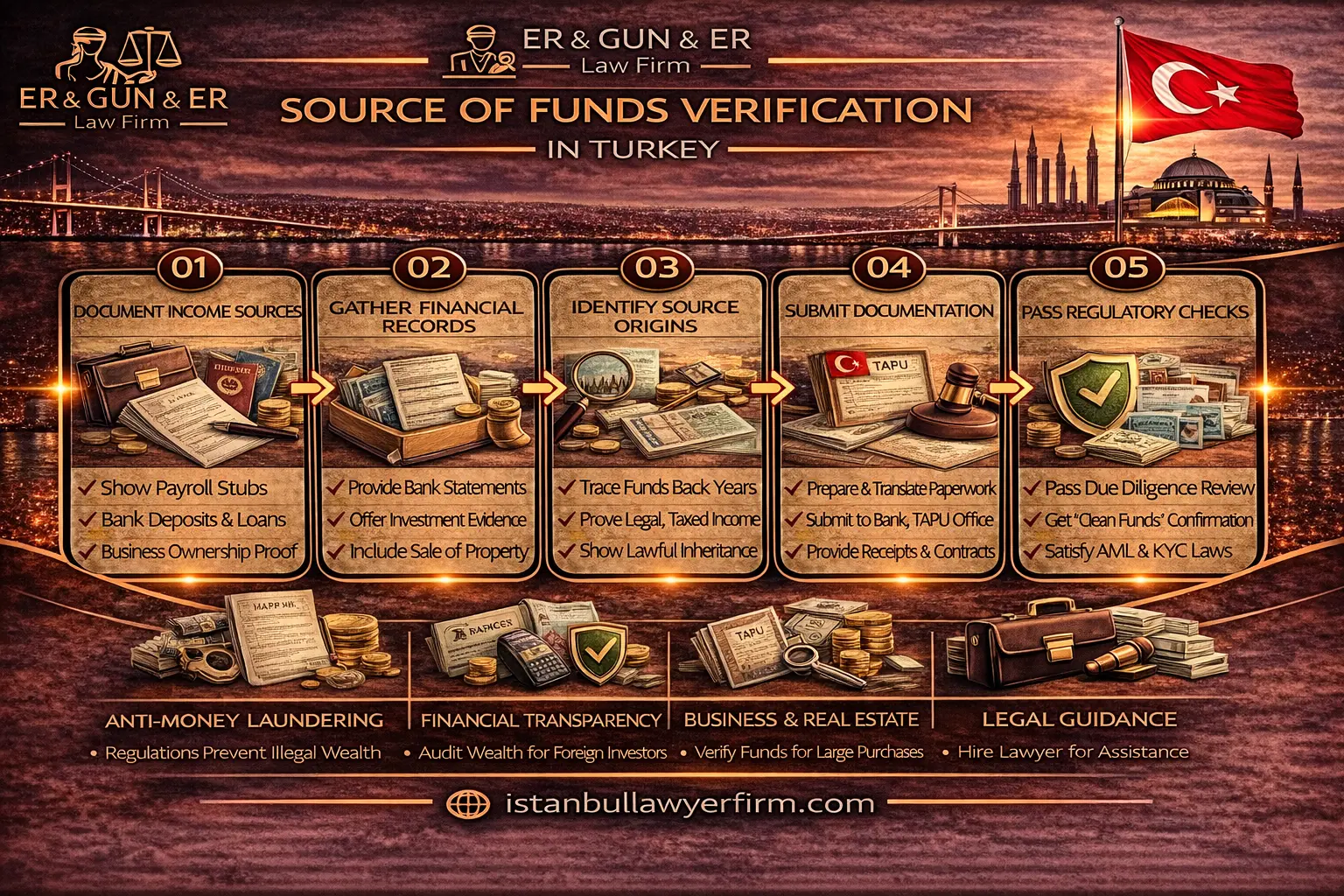

What Source of Funds Means

Source of funds (fonun kaynağı) means the immediate origin of the money used for one transaction. It asks what account the money left from, what account received it, what instrument moved the money, and why the amount matches the deal. It asks whether the sender is the customer, whether an intermediary is involved, whether the intermediary has authority, whether the narrative matches records, whether records predate the transaction, whether the record trail is continuous, whether the trail is legible, whether translations are consistent, and whether the bank can keep copies. This is the practical content of the proof of funds bank request, and it sits within the broader AML compliance framework under Law 5549 and the MASAK regulations. Practice may vary by authority and year — check current guidance.

Source of funds is narrower than overall financial background. It is not the full life story of wealth; it is the specific funding chain for a single transaction. It can be salary savings, but must be traceable. It can be a business dividend, but must be documented. It can be an asset sale, but must be evidenced. It can be a loan, but must be provable. It can be a gift, but must be recorded. It can be an inheritance, but must be supported. The bank checks consistency with the customer profile, unusual routes and intermediaries, cross-border corridors and origin countries, plausibility of the source, whether funds were cleanly banked or originated as cash, and whether the documentary trail predates the transaction. A clean file avoids repeated questions; a structured file reduces delays.

In practice, the strongest files look like a timeline. The timeline starts with the generating event — wages, sale, dividend, loan, gift, inheritance — supported by official documents. The timeline then shows deposits and transfers, account statements for the relevant period, the exact outgoing transfer instruction, the receiving bank credit advice, conversion steps if currency changed, and the final payment to seller or escrow. The timeline includes translations for key documents and a short narrative memo citing exhibit numbers. The memo avoids emotional language and unsupported claims. Practice may vary by authority and year — check current guidance. The objective is a reviewer-proof pack with one index and one chronology.

Why Banks Require Verification

Banks require verification to manage money laundering risk under Law 5549 and the MASAK Tedbirler Yönetmeliği, alongside sanctions and fraud risk under Decree No. 32 on the Protection of the Value of Turkish Currency and the BDDK regulatory framework. Banks must understand the customer transaction purpose, identify whether a transaction is unusual relative to the customer profile, collect and retain records, apply customer due diligence (CDD) processes, apply enhanced due diligence (EDD) for higher-risk profiles, and file suspicious transaction reports (şüpheli işlem bildirimi) to MASAK in defined scenarios. This is the structural backbone of MASAK reporting requirements and bank compliance documentation. Practice may vary by authority and year — check current guidance. Banks differ in internal policies, risk appetite, and document preferences; the safe approach is to expect questions and prepare early.

Verification also protects the client from later freezes. A bank can pause an incoming transfer when the story is unclear, pause an outgoing payment when documents are missing, require additional information mid-transaction, request translated and certified copies, ask for updated statements closer to execution, ask for the same proof again for a later transfer, ask for third-party contracts behind the payment, ask for corporate documents behind a company payment, ask for tax filings as context evidence, ask for employment records as context evidence, ask for explanation of cash deposits, and ask for explanation of multiple accounts. Good planning reduces business disruption and reduces stress at closing.

Verification is also demanded by counterparties in deals. Sellers want comfort that payment will clear; developers want comfort that funds are bankable; lawyers want comfort that closing will not collapse. Real estate closings are time-sensitive in practice (Land Registry appointments operate on fixed windows); corporate closings also involve fixed signing windows. The right time to build the pack is before signing, the right time to translate is before banking questions arrive, and the right time to reconcile statements is before transfer orders. If the bank asks a new question, answer with exhibits, not with narratives alone. Keep the narrative consistent across channels. Practice may vary by authority and year — check current guidance. If you plan to open accounts remotely, see remote account opening guidance.

Source of Wealth Distinction

Source of wealth (servetin kaynağı) is the broader story of how a person accumulated assets. It is different from the funding chain for one payment. Banks may request both in higher-risk profiles under enhanced due diligence requirements, particularly for politically exposed persons (PEPs) under MASAK guidance, for large investments, and for repeated transfers. The file should keep wealth narrative separate from funds narrative. Wealth narrative can include career history and business ownership; inheritance history and asset appreciation; long-term savings patterns. Funds narrative must still show the specific chain for this deal. Practice may vary by authority and year — check current guidance. A wealth memo should be short and factual; a funds memo should be specific and exhibit-driven; the two memos should not contradict each other.

Wealth narrative should be supported by anchor documents. For employment wealth, use employment confirmations and tax summaries. For business wealth, use financial statements and dividend evidence. For asset appreciation, use sale contracts and registry proofs. For inheritance, use probate (veraset ilamı) and distribution proofs. For gifts, use donor evidence and banking trails. Keep the time horizon clear in the memo; do not imply certainty beyond documents; do not present estimates as facts. A reviewer will test consistency across documents, plausibility against transaction size, whether the narrative predates the deal, and whether documents match names and dates.

Wealth requests often arise when the client profile is complex: multi-country residence, multiple business entities, politically exposed connections, unusual cash activity, crypto conversion patterns, recent large windfalls, third-party funding. In these profiles, a structured file matters more than persuasive language. Counsel can help build a coherent narrative, avoid over-disclosure, align translations and certifications, and coordinate with counterparties. In complex files, structured exhibit packaging reduces friction at the bank's compliance desk substantially more than rhetorical positioning.

Risk-Based KYC Approach

Risk-based KYC means banks calibrate diligence to risk, in line with the MASAK Tedbirler Yönetmeliği's risk classification framework. Low-risk profiles may face lighter questions; higher-risk profiles face deeper questions. Risk can arise from country corridors (FATF higher-risk jurisdiction lists, sanctions exposure), transaction type, sector and product, cash intensity, third-party involvement, unusual behavior patterns, rapid movement of funds, opaque corporate structures, crypto conversions, and inconsistent documentation. Practice may vary by authority and year — check current guidance. Risk scoring is internal and not fully visible; clients should plan for enhanced diligence, treat questions as normal compliance, and answer with documents rather than emotion.

Risk-based KYC is also iterative over time. A bank can accept a file today and ask more tomorrow as the customer's activity pattern changes risk perception, as bank internal policy changes, or as MASAK guidance shifts expectations. The safest habit is to keep a reusable compliance folder containing identity and address proofs, core wealth anchors, translated corporate papers if needed, an index and chronology template, bank communication logs, receipts and confirmations, and a change log for updated documents. This is a practical evidence trail that reduces repeated scrambling.

Risk-based KYC also means the same evidence can be reused across deal types. A property deal can reuse salary proof; a company investment can reuse dividend proof; a citizenship-related investment can reuse asset sale proof; cross-border wiring can reuse the same bank statements. The file should therefore be modular by source type, by currency corridor, and by counterparty. The transaction memo should be separate from the wealth memo; the bank memo should be separate from the counterparty memo. This modular structure is what makes compliance scalable. For currency evidence discipline, see foreign currency purchase document guidance.

Typical Document Expectations

Typical document expectations are not a static checklist, because different banks and risk profiles produce different requests under the MASAK risk-based framework. The safest approach is to think in categories of proof, not in a single list. One category is identity and address evidence to anchor the file. One category is the generating event that created the funds — salary, sale, dividend, loan, gift, inheritance. One category is the banking trail showing funds moving through accounts. One category is the transaction contract explaining why the payment exists and why the amount matches. One category is currency conversion evidence when funds changed currency in the chain. One category is any notarized or certified steps when documents are foreign or when counterparties require formality. Practice may vary by authority and year — check current guidance.

The practical method is to build an evidence pack that can answer the first three "why" questions: why is this customer sending this amount, why did this money arrive in the customer's account, and why is the payment route structured this way. If the file can answer these questions with exhibits, most follow-up questions shrink. The file should include account statements showing the credit and the debit relevant to the transaction (not an entire year unless requested), the contract that explains the transaction, the identity link between the customer and the generating source, and the timing logic showing that funds were received before they were sent. The file should avoid circular transfers that look like layering, fragmented small transfers that obscure origin, and narrative memos that contradict statements.

Document expectations also change by transaction type. For a property purchase, the file must show the buyer's funding chain and the purchase context. For corporate investment, the file must show the investor's funding chain and the corporate context. For citizenship-related investment, the file must show the investor's funding chain and consistency with the declared investor profile under the Turkish Citizenship by Investment programme. For transaction-driven discipline, many clients also build a parallel due diligence file; real estate due diligence helps structure what counterparties commonly ask in property deals. The bank file should remain distinct and focused on money origin and movement.

Salary and Employment Income

Salary funding is often the simplest story but it still needs a traceable chain. Banks typically want to see that the payer is a real employer, that the income is consistent over time, that the customer's account shows deposits matching the narrative, that savings accumulation is plausible relative to living expenses, and that the outgoing transfer matches the accumulated balance. Practice may vary by authority and year — check current guidance. A salary file should start with an employment confirmation identifying employer, role, and period. The file should then include payroll evidence or pay slips showing deposits (only relevant months unless asked for more), bank statements showing those deposits arriving with dates and reference lines visible, a savings memo explaining accumulation factually, tax filings or official income declarations where they exist, and a conversion note if salary is in one currency and the deal is in another, with bank conversion receipts.

Employment income also intersects with cross-border transfers because many foreign employees are paid abroad and then fund Turkey transactions. The file must show foreign account statements as well, at least around the relevant transfer period, and must show the wire instructions. If foreign documents are used, plan translation where needed and keep a token sheet for names and employer identity. Employer identity should be consistent across payroll and bank statements; mismatched abbreviations trigger follow-up. Bonuses or one-off payments should be presented as separate events with separate exhibits; large one-offs raise questions. Avoid labelling a bonus as "gift" or "loan" inconsistently across documents because inconsistency is a red flag. Practice may vary by authority and year — check current guidance.

Salary files are often rejected not because salary is untrusted but because the pack is poorly structured. Poor packs lack visible dates and amounts, use screenshots without headers, mix different accounts without explanation, use redactions that remove essential identifiers, or include narratives that contradict statements. The cure is to standardise the pack: employment confirmation, pay evidence, bank statement excerpts, and outgoing transfer proof. Include a short table-like narrative in prose describing month-by-month accumulation. If the customer saved over many years, show that the account balance grew steadily rather than appearing suddenly. If it appeared suddenly, explain the event and move to the correct lane (asset sale or loan). For clients who need bilingual files consistent across jurisdictions, structured token discipline reduces friction.

Business Income Evidence

Business income evidence is more complex because it can be generated through multiple channels and can involve multiple entities. Banks often ask who owns the business and how income flows to the individual, whether income is declared and documented under Turkish corporate tax (Law No. 5520) and personal income tax (Law No. 193), whether the company's activity matches the volume of funds, and whether distributions are formal or informal. Practice may vary by authority and year — check current guidance. A business file should start with corporate identity documents showing legal existence and ownership, then financial evidence such as audited statements, management accounts, or tax filings where available, then the distribution mechanism (dividends, profit distributions, salary, shareholder loans) clearly labelled and consistent, then bank statements linking business accounts to personal accounts through transfers that match the stated mechanism.

Business income is often challenged when the company structure is opaque or when the beneficial owner is unclear. The file should include a beneficial ownership memo consistent with corporate records, particularly the ultimate beneficial owner (UBO) declarations under MASAK's beneficial ownership transparency requirements. If multiple companies exist, include an ownership chart and identify which entity generated the funds used for the deal. Include bank account identifiers for each entity and show the transfer path from entity to individual to transaction counterparty. If funds came through intermediary accounts, justify the route and provide authority and contract evidence. If the business operates abroad, include foreign corporate records and plan translation; keep a consistent token sheet across all documents.

Business evidence is also a timing discipline. Banks often ask whether the distribution was recent and why. If sudden and large, show the triggering event such as a dividend decision or asset sale, and provide the corporate resolution evidence. Avoid post-dating documents to fit a narrative — that is a serious red flag. Preserve the original dates and explain how they align with the deal timeline. Keep the narrative consistent with tax filings where those exist; inconsistency between corporate filings and bank narrative invites deeper review. For corporate formation context, see foreign investor company law and company formation overview.

Sale of Assets Evidence

Sale proceeds are a common funding source because they create a clean event that can be documented, but they still require continuity from sale contract to credited funds to outgoing payment. The first control is to identify the asset sold and prove ownership before sale. The second is to prove the sale transaction with a signed agreement or official record stating parties, date, and consideration. The third is to show the payment route for proceeds, preferably through banking channels rather than cash. The fourth is to show the credit in the seller's account with a statement excerpt including date and reference. The fifth is to show that the credited proceeds were not materially mixed with unrelated cash deposits. The sixth is to show any tax declaration or official receipt where it exists and is relevant. The seventh is to show conversion steps if proceeds were in a different currency. The eighth is to show the outgoing transfer instruction for the Turkish deal and the matching debit. Practice may vary by authority and year — check current guidance.

Asset sales can be real estate sales, securities sales, business sales, or other disposals; each category has its own proof style. A real estate sale has registry evidence linkable to title history. A securities sale has broker statements and trade confirmations. A company sale has share purchase documents, closing statements, and payment receipts. The common failure point is a narrative that says "I sold X" but cannot show proceeds arriving in the account that funded the Turkish payment. Other failures: proceeds paid in cash or to a third party (breaks continuity), proceeds in multiple fragments without explanation (looks like layering). The cure is a proceeds reconciliation memo tying contract consideration to credited amounts by date and reference. For currency conversion history, see foreign currency purchase document guidance.

Asset sale evidence is frequently used for real estate purchases in Turkey, which is why real estate purchase proof of funds files often start from a sale story. The right structure is to show ownership of the sold asset, sale agreement, proceeds credit, conversion, and final payment to the Turkish seller. If the target purchase is also real estate, anticipate that counterparties and banks may ask for both source-of-funds and property due diligence materials simultaneously. Keep these packs separate but consistent. The due diligence lane can use real estate due diligence; the title verification lane can use title deed check.

Gifts and Inheritance Trails

Gift funding is higher-risk in compliance review because it introduces third-party funds and intent questions. The file must prove both the donor's capacity to give and the path of funds. The first control is to identify the donor, the relationship to the recipient, and why the gift exists. The second is to show the donor's source of funds or wealth for the gifted amount, at least at a level that makes the gift plausible. The third is to show the donor's bank statement excerpt proving the debit. The fourth is to show the recipient's statement excerpt proving receipt. The fifth is to show any gift deed (bağış sözleşmesi under Code of Obligations Articles 285-298) or declaration where used, with language consistent with the bank narrative. The sixth is to ensure consistency with foreign exchange rules under Decree No. 32 where cross-border transfers occur. Practice may vary by authority and year — check current guidance. Gift tax obligations under the Inheritance and Gift Tax Law (Law No. 7338) may apply depending on amount and relationship; align reporting with funding evidence.

Inheritance funding can be more defensible because it is a formal event under the Turkish Civil Code (Law No. 4721) Articles 495 et seq. and the Inheritance and Gift Tax Law (Law No. 7338), but it still requires a traceable trail from estate distribution to the recipient's account. The first control is to show the inheritance event proof such as the inheritance certificate (veraset ilamı) issued by the magistrate court (sulh hukuk mahkemesi) or by the notary under the streamlined procedure introduced by Law No. 6217. The second is to show that the recipient was an heir or beneficiary under the proof. The third is to show the payment route, ideally through bank transfers with clear reference lines. If the inheritance is foreign, include apostille and translation bundles where needed and maintain a token sheet to prevent spelling drift. If installments, reconcile installment credits to the distribution statement. If long ago, explain how it remained available for this transaction.

Gifts and inheritances are also often accompanied by notarised declarations or family agreements. Notarisation can help document intent, but it does not replace a banking trail. Banks primarily want to see the money move through accounts with continuity. A notarised deed without a corresponding bank transfer leaves the key question unanswered. Conversely, a bank transfer without a plausible donor profile triggers questions. Combine donor profile proof and transfer proof in one coherent pack. Anticipate that banks may ask for donor identification documents and address proofs. Avoid inconsistent terms — "loan" in one document and "gift" in another is a red flag. If a gift is actually a loan, move to the loan lane.

Loans and Financing Proofs

Loan funding can be acceptable, but banks scrutinise it because it can be used to disguise layering unless documented properly. The first control is to prove lender identity and relationship to borrower, whether bank lender or private lender. The second is to prove the loan agreement with clear terms, signed by the correct parties, in a form consistent with the jurisdictions involved. The third is to prove drawdown — actual transfer of loan funds into the borrower's account, shown in statements. The fourth is to prove that the borrower then used those funds for the Turkish transaction, shown in outgoing transfer proofs. The fifth is to show repayment ability or repayment plan when requested. Practice may vary by authority and year — check current guidance. Avoid cash disbursements (break traceability); avoid circular flows where the borrower repays the lender immediately from the same funds (looks like self-funding); avoid multiple intermediaries unless each is evidenced and authorised; show that the lender's own source is plausible (especially private loans).

Private loans can be more challenging because banks may request additional context to understand the lender and the legitimacy of the funding. The file should be ready to provide lender identity documents and evidence that the lender had capacity to lend, such as bank statements or income evidence. If the loan is secured, provide security documents. If the loan is provided by a company, include corporate authority evidence such as board approvals or signatory authority documents. If the loan is provided through an offshore vehicle, expect enhanced scrutiny and prepare beneficial ownership documentation. If the loan is provided by a Turkish bank under the standard banking facility framework regulated by the BDDK under the Banking Law (No. 5411), include the loan agreement and bank disbursement proofs.

Loans also intersect with foreign money transfer documentation when loan funds are drawn abroad and transferred to Turkey under Decree No. 32 capital movement rules. The file should show the inbound wire documentation, including sender name, origin bank, and reference. If currency conversion occurs, include conversion receipts or bank advices. If the borrower is using the loan for a citizenship-related investment, keep the loan lane coherent and avoid mixing it with the gift lane (inconsistent labelling is a red flag). If the borrower is a company, coordinate the loan file with company documents; corporate context aligns with foreign investor company law and company formation overview.

Crypto and Digital Assets

Crypto funding is scrutinised because it can break the traditional banking audit trail, so the file must translate blockchain activity into bank-readable evidence. Many banks treat crypto-related inflows as higher-risk by default under the MASAK risk-based framework, particularly following the Central Bank's Regulation on Disuse of Crypto-Assets in Payments (effective 30 April 2021) and the Capital Markets Board's regulatory framework for crypto-asset service providers under Law No. 7518 amendments to the Capital Markets Law (effective 2 July 2024). The first control is to identify the exact wallet or exchange account that generated the funds and prove control of that account by the customer. The second is to map the acquisition route — where the crypto was bought and how fiat entered the crypto ecosystem. The third is to preserve exchange statements, trade confirmations, and withdrawal receipts showing dates, amounts, and counterparties. The fourth is to preserve bank statements showing the original fiat deposits used to buy crypto — "crypto profits" without fiat entry proof is weak.

The fifth control is to document the conversion step from crypto to fiat, including the exchange payout record and the receiving bank credit advice. The sixth is to document any intermediate stablecoin use as a factual step. The seventh is to avoid using anonymous mixing tools or privacy-enhancing routes that cannot be explained in a bank file (these are red flags). The eighth is to avoid third-party wallet funding unless there is a documented relationship and a coherent authority explanation. The ninth is to keep a transaction hash appendix as internal support but present the bank-facing memo in plain language with exhibits. The tenth is to keep a valuation memo for timing using exchange rates from the exchange statements. The eleventh is to ensure that the crypto trail ends in a regulated bank account before the Turkish deal payment. Practice may vary by authority and year — check current guidance.

Crypto files usually fail because they start in the middle of the story. A client shows a wallet balance and expects acceptance, but the bank wants the origin of the fiat that became crypto. Other failures: showing exchange gains but not exchange deposit source; showing a withdrawal but not the bank credit with matching reference; using multiple exchanges without a coherent explanation; using peer-to-peer trades without a defensible counterparty trail; assuming a blockchain explorer screenshot is enough; presenting a narrative that contradicts timestamps on exchange exports; redacting too aggressively; omitting tax filings if the bank explicitly requests them; mixing crypto proceeds with unrelated cash deposits. The discipline uses one chronology, one index, and primary exports. When crypto is used in a property or investment transaction, define the start point as the first fiat source and the end point as the final payment from a bank account to the counterparty.

Cross-Border Transfers Trails

Cross-border transfers are often the point where a clean source story becomes fragmented. The file must show the complete corridor from origin bank to Turkey bank under Decree No. 32 capital movement rules. The first control is to show the outgoing instruction from the origin bank, including sender name, origin account, beneficiary name, and purpose. The second is to show the origin bank debit on a statement excerpt matching the instruction. The third is to show any intermediary bank messages where the corridor routes through correspondent banks. The fourth is to show the receiving Turkish bank credit advice or statement credit matching sender, amount, and date. The fifth is to show currency conversion documentation if conversion occurred during or after transfer, using bank confirmations rather than assumed rates. The sixth is to show why funds were routed in that way, especially if multiple hops exist. The seventh is to ensure that sender identity matches the claimed source — third-party senders are enhanced-risk in many bank policies. Practice may vary by authority and year — check current guidance.

Cross-border failures often happen when the file is incomplete in the middle. A client shows the Turkish bank credit but cannot show the origin debit. Or shows an origin debit but cannot show the Turkish credit. Or shows both but cannot explain why the sender name differs. Or shows the transfer but cannot show the generating event that funded the origin account. Or shows multiple transfers but cannot reconcile totals to the purchase price. Or shows conversions but cannot show bank-issued conversion receipts. A family member sender called "my money" without documented gift or loan structure is treated as third-party funding. A corporate sender for a personal purchase needs corporate authority. Screenshots without headers and references are often rejected as insufficient. The cure is a corridor reconciliation memo tying each step by date, amount, and reference.

Cross-border trails are also influenced by local foreign exchange compliance under Decree No. 32. Some transactions require additional documentation for conversion and settlement; the file should keep those documents aligned with the transfer story. Foreign currency purchase documentation is useful as a process map. Conversion evidence should be cross-referenced to the same chronology. The bank may ask "why Turkey" — answer with the transaction contract, not narrative. Include the purchase agreement or investment agreement as the purpose anchor; avoid attaching unrelated documents. If the transfer is part of a series, note it as series transfers can be interpreted as business activity and trigger different KYC questions. Preserve all bank communications as exhibits.

Real Estate Transaction Needs

Real estate purchases are the most common high-intent use case for source of funds in Turkey because buyers must pay through banks (cash payment for real estate has been restricted under Tax Procedure Law General Communiqué No. 459 for transactions above defined thresholds) and counterparties are sensitive to failed closings. The first control is to align the payment plan with the title transfer (tapu devri) timeline at the Land Registry (Tapu Müdürlüğü) — appointments operate on fixed windows and bank holds can collapse them. The second is to build the funding pack early and test it with the bank before funds are sent to the seller. The third is to ensure the funding pack links to the specific property and deal terms, using the contract as the purpose anchor. The fourth is to ensure the pack includes the last-mile proof: the bank debit from buyer account to seller account, matching the contract amount.

The fifth control is to ensure the pack includes any currency conversion proof if the purchase is funded in foreign currency but paid in Turkish lira (the standard for Land Registry transfer pricing), using bank receipts. The sixth is to avoid third-party funding routes unless documented as gift or loan with full trails. The seventh is to ensure the pack includes buyer identity and address proofs consistent with the bank's KYC file. The eighth is to coordinate the funding pack with property due diligence. The ninth is to coordinate with the title deed check process. Practice may vary by authority and year — check current guidance. The tenth is to avoid asserting "the bank will approve" — banks can request more proof at any time. The property diligence lane can use real estate due diligence; the title verification lane can use title deed check.

In property deals connected to residency or citizenship pathways under the Turkish Citizenship Law (Law No. 5901) Article 12 and Regulation (the USD 400,000 real estate investment threshold introduced by Presidential Decree in May 2022), scrutiny can increase because the transaction is high profile and often cross-border. The evidence logic remains the same: generating event, banking continuity, matched payment, readable exhibits. The file should follow the bank's written checklist and the Ministry of Interior's General Directorate of Civil Registration and Citizenship Affairs (Nüfus ve Vatandaşlık İşleri Genel Müdürlüğü) checklist for the citizenship application, storing each as an exhibit. Keep a separate source-of-wealth memo and a separate source-of-funds memo. Include a post-payment verification step preserving the bank receipt and the seller credit confirmation.

Corporate Transactions Needs

Corporate transactions require a combined individual and corporate KYC posture because banks assess beneficial ownership, governance, and control in addition to the money trail under MASAK's UBO transparency framework and TTK provisions on share transfers (TTK Articles 489-501 for joint-stock companies, Articles 595-598 for limited liability companies). The first control is to identify the transaction type — share purchase, capital increase, shareholder loan, or asset purchase — and keep the contract as the purpose anchor. The second is to identify the payer (individual, Turkish company, foreign company), as payer identity drives evidence needs. The third is to produce corporate identity evidence (Trade Registry extract, MERSİS records) and authority evidence (signatory circular, board resolution) for the paying entity. The fourth is to show beneficial ownership in a simple, factual chart matching corporate records and the UBO declaration filed with MASAK. Practice may vary by authority and year — check current guidance.

Corporate files commonly fail when authority is unclear or inconsistent. A company pays but no one can show who authorised the payment. A company pays but beneficial ownership is unclear, so the bank pauses. A company pays but contract names do not match the registry names due to spelling drift or outdated titles. A company pays but funds came from an unrelated third party without a loan or capital injection record. A company pays but the bank cannot see the business rationale. The cure is to keep the corporate evidence pack clean and indexed: company identity, signatory authority, beneficial ownership, transaction contract, funding chain, payment proof. Corporate context aligns with foreign investor company law and company formation overview.

Corporate transactions also intersect with inheritance and succession planning because ownership can change due to death, and beneficiaries may later need to prove ownership transitions. If corporate ownership changes due to inheritance, banks may request additional proofs such as inheritance certificates and corporate resolutions. The estate planning overview at inheritance planning can help align document readiness. The corporate compliance file should include a succession note identifying who controls corporate documents, where originals are stored, and how signatory authority will be updated. Corporate deals are sensitive to reputational risk, so counterparties may apply their own KYC and request a similar source-of-funds pack.

Red Flags and Pitfalls

Red flags are patterns that cause banks to escalate diligence under the MASAK Tedbirler Yönetmeliği's risk indicators and the bank's internal risk policy. The practical goal is to remove avoidable red flags by designing a clean trail. The standard red flags include: third-party funding without a documented gift or loan file; heavy cash deposits with no generating event evidence; circular transfers that look like layering; fragmented transfers designed to obscure totals; inconsistent narratives across different documents; mismatched names and dates across translations and statements; missing origin debit evidence for an inbound transfer; missing destination credit evidence for an outbound transfer; a contract amount that does not match the payment amount with no explanation; an abrupt large balance increase without a documented triggering event; crypto proceeds without fiat entry and exit documentation; corporate payments without corporate authority proofs; using multiple intermediaries without contractual authority; presenting only screenshots without headers and reference lines; refusing to provide core documents while insisting the bank should accept it. Practice may vary by authority and year — check current guidance.

Pitfalls also include over-sharing the wrong material. Dumping an entire tax return can confuse the reviewer if it does not match the transaction story. Sending unrelated contracts can increase questions and expand scope. Sending inconsistent translations can create identity doubts. The safe approach is targeted disclosure: only what supports the specific claim, in a coherent order. Other pitfalls: under-sharing (narrative without primary documents triggers immediate follow-up); late preparation (building the file after the transfer is held removes leverage); assuming one bank's acceptance means another bank will accept (banks differ in internal risk policy); using aggressive language in communications (compliance teams become defensive); allowing multiple family members or staff to answer the bank separately (creates contradictions). The cure is one spokesperson, one custodian, one index, one chronology, and (for cross-border files) one token sheet and one translation bundle.

Red flags also arise when the compliance file does not match the transaction reality. If a property purchase is funded by a company but the memo says "personal savings," the file contradicts itself. If a gift is actually a loan but is described as a gift, the file contradicts itself. If an inheritance distribution is used but no probate proof is attached, the file looks incomplete. The solution is to keep the narrative memo anchored to exhibits and avoid legal conclusions beyond what exhibits support. The memo should use a simple structure: origin event, banking trail, transaction payment. The memo should also state what could not be obtained yet and what is being requested, rather than pretending completeness. The memo should define whether funds are from one source or multiple sources and show the reconciliation if multiple. A disciplined red flag review reduces the chance of frozen funds and MASAK suspicious transaction reports being filed against the customer's account.

Compliance File Roadmap

A compliance file roadmap is the repeatable internal system that makes source-of-funds work predictable, even when bank requests vary. The first step is to open a master folder with an index document and a chronology document. The second is to capture identity and address proofs reusable across banks. The third is to open a claim register listing the funding source chosen for the transaction. The fourth is to gather the generating event documents. The fifth is to gather the banking trail documents. The sixth is to gather transaction documents (purchase agreements, invoices) in a targeted way. The seventh is to gather currency conversion proofs where currency changes occur. The eighth is to draft a short narrative memo citing exhibit numbers. The ninth is to run a consistency check (names, dates, amounts, direction of funds). The tenth is to run a red flag check and cure avoidable issues before funds move. The eleventh is to store a bank communication log. The twelfth is to apply version control. The thirteenth is to apply privacy controls under KVKK (Law No. 6698). The fourteenth is to keep packs modular for future reuse. The fifteenth is to run a post-transaction archive step. Practice may vary by authority and year — check current guidance.

The roadmap should also be mapped to transaction types so teams do not improvise during closings. For property purchases, include property due diligence and title verification cross-references without mixing the packs. For corporate investments, include corporate authority and beneficial ownership tabs. For cross-border wires, include the corridor file. For crypto, include fiat entry, exchange trades, crypto exit, and bank credit. For inheritance and gifts, include donor or estate proof and the bank trail. For loans, include agreement, drawdown, and application. The roadmap should be trained into staff routines and aligned with data retention policies under both Law 5549's record-keeping requirements and the Tax Procedure Law (Law No. 213). The roadmap should include a one-spokesperson rule and a bank-specific appendix storing each bank's checklist and preferred format.

The roadmap should end with a realistic governance principle: do not move money until the file is defensible. That principle prevents the most expensive problem — a held transfer during a fixed closing window. The file should be tested internally by a reviewer who did not build it, because fresh review detects contradictions. The file should be tested for three-minute readability, token consistency, single source per paragraph, and cross-lane consistency where the same documents are used for tax reporting or title transfer. The estate reporting lane can be coordinated using estate tax reporting when inheritance proceeds are part of the funding chain, but the source-of-funds memo should remain focused on the transaction at hand. A disciplined roadmap satisfies banks and MASAK expectations without over-disclosing and without inventing numbers or timelines.

Frequently Asked Questions

- What law governs AML and source of funds in Turkey? Law No. 5549 on Prevention of Laundering Proceeds of Crime (effective 11 October 2006), the implementing Tedbirler Yönetmeliği, and the supervision of MASAK (Mali Suçları Araştırma Kurulu) under the Ministry of Treasury and Finance. Law 5237 (Penal Code) Article 282 criminalises money laundering with imprisonment of three to seven years.

- What is MASAK? The Financial Crimes Investigation Board, the Turkish financial intelligence unit responsible for receiving, analysing, and disseminating suspicious transaction reports under Law 5549, and for issuing implementing guidance to obliged entities including banks.

- What is the difference between source of funds and source of wealth? Source of funds is the funding chain for one transaction; source of wealth is the broader story of asset accumulation. Banks may request both for higher-risk profiles.

- What documents prove source of funds? Identity and address proofs, generating event documents (employment confirmation, sale contract, dividend resolution, inheritance certificate, gift deed, loan agreement), bank statements showing credits and debits, transaction contracts, and currency conversion receipts.

- Is risk-based KYC the same across banks? No. Banks calibrate diligence to their internal risk policy within the MASAK framework. Low-risk profiles face lighter questions; higher-risk profiles face deeper questions including enhanced due diligence.

- What triggers a suspicious transaction report? Patterns inconsistent with the customer profile, transactions without economic or legal rationale, structuring to avoid reporting, and other indicators set out in MASAK guidance. The customer is not informed of the report (tipping-off prohibition under Law 5549).

- Can crypto fund a Turkish transaction? The trail must show fiat entry (bank to exchange), exchange activity, fiat exit (exchange to bank), and the final bank payment to the counterparty. The Central Bank's 30 April 2021 regulation prohibits crypto-asset use in payments; CMB framework under Law 7518 amendments regulates crypto-asset service providers.

- What about cross-border transfers? Show origin bank debit, transfer instruction (with sender, beneficiary, purpose), intermediary bank advice if applicable, Turkish bank credit, and currency conversion under Decree No. 32. Sender identity must match the claimed source.

- What is required for citizenship-by-investment source of funds? The same evidence logic applies: generating event, banking continuity, matched payment, readable exhibits. The Ministry of Interior's General Directorate of Civil Registration and Citizenship Affairs publishes specific documentary requirements for citizenship applications under Law 5901 Article 12.

- Are gifts and inheritances subject to tax? The Inheritance and Gift Tax Law (Law No. 7338) imposes graduated tax on transfers; the source-of-funds documentation should align with any tax declarations made.

- What about cash payments for property? Cash payment for real estate above Tax Procedure Law thresholds (currently subject to Tax Procedure Law General Communiqué No. 459 limits) requires reporting. Banking channels are the standard.

- How long do banks keep records? Under Law 5549 Article 8, obliged entities must retain customer identification, transaction records, and supporting documents for at least 8 years from the transaction or relationship end.

- What is beneficial ownership? The natural person or persons who ultimately own or control a customer or the natural person on whose behalf a transaction is being conducted. UBO declarations are required under MASAK guidance.

- Can I appeal a held transfer or restricted account? Yes. The first step is dialogue with the bank's compliance function with a documentary submission addressing specific concerns. If unresolved, complaint to BDDK (banking conduct), administrative court action against the bank's decision, or — where MASAK action is involved — challenge under the Administrative Procedure Law (Law No. 2577) may be available.

- Where does ER&GUN&ER Law Firm support source of funds matters? Pre-transaction file design; bank dialogue management; MASAK compliance positioning; UBO documentation; cross-border transfer documentation under Decree No. 32; citizenship-by-investment source of funds files; corporate KYC for transaction parties; and dispute resolution where transfers are held or accounts are restricted.

Author: Mirkan Topcu is an attorney registered with the Istanbul Bar Association (Istanbul 1st Bar), Bar Registration No: 67874. His practice focuses on cross-border and high-stakes matters where evidence discipline, procedural accuracy, and risk control are decisive.

He advises foreign investors, property buyers, citizenship-by-investment applicants, corporate transaction parties, and high-net-worth individuals across Source of Funds Documentation, MASAK Compliance Positioning, Bank KYC/AML Dialogue, Cross-Border Transfer Documentation under Decree No. 32, Citizenship-by-Investment Files, Corporate Transaction KYC, and dispute resolution where transfers are held or accounts are restricted.

Education: Istanbul University Faculty of Law (2018); Galatasaray University, LL.M. (2022). LinkedIn: Profile. Istanbul Bar Association: Official website.