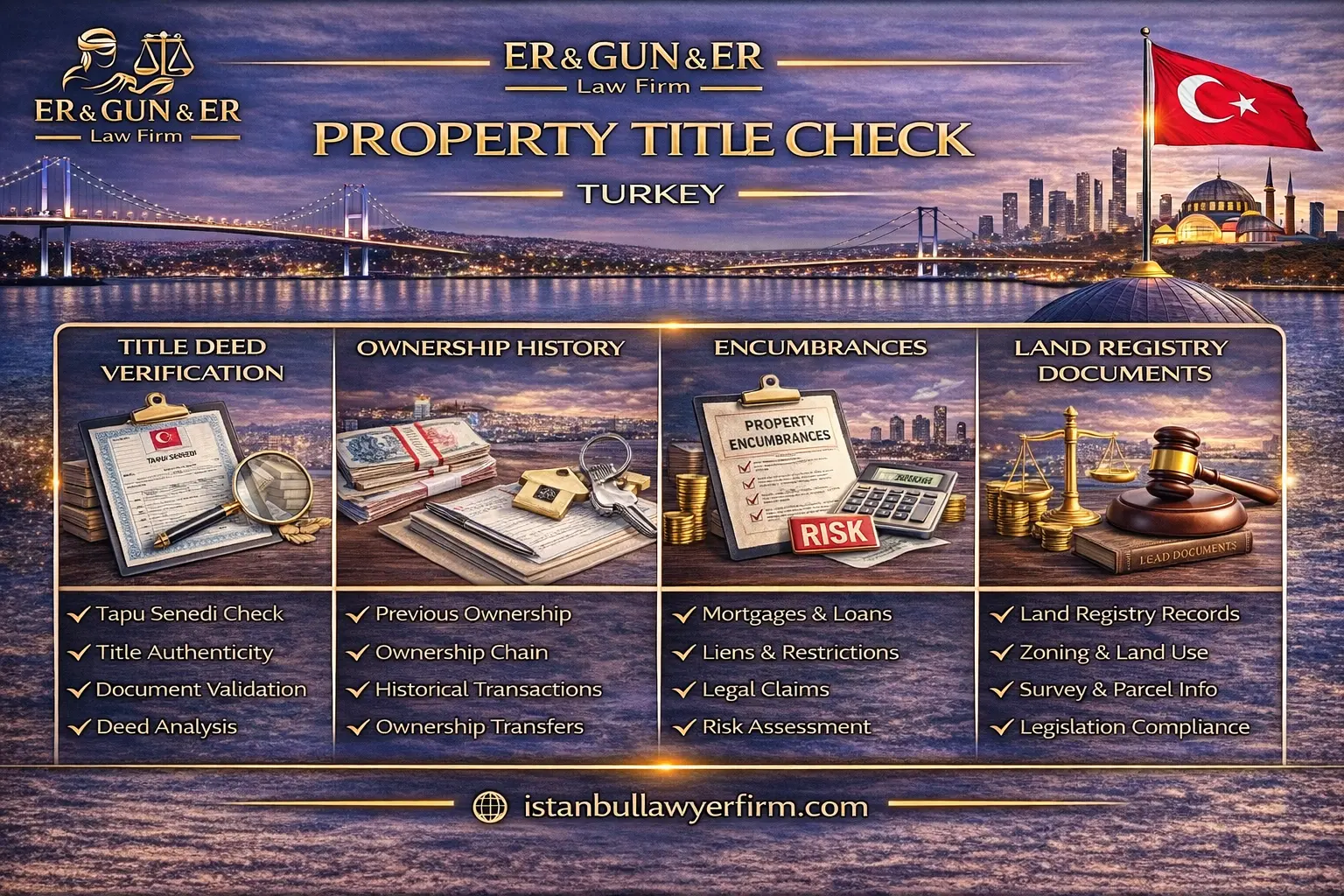

A title deed review is the fastest way to turn a property story into verifiable legal facts. In a cross-border purchase, documents shown by an agent can look complete while the land registry record tells a different story. A disciplined check reduces fraud exposure, prevents closing on the wrong parcel, and limits future disputes about ownership and boundaries. For foreign buyers, the most common failures are incomplete identity verification, missing encumbrance visibility, and reliance on informal assurances instead of certified records. That is why foreign buyer due diligence Turkey should be structured as an evidence project, not as a negotiation ritual. The process also intersects with zoning, occupancy status, and building compliance, which can affect use, resale, and rental strategy. Working with a Turkish Law Firm is most effective when the team controls the document chain and keeps every conclusion tied to a source that can be reproduced later.

Title deed check overview

A proper property title check Turkey begins with identifying the exact land registry record that will be transferred at closing. The goal is to confirm that the seller is the recorded owner and that the property description matches the unit you toured. This starts with pulling the relevant record and comparing parcel, block, and independent section identifiers against the sales file. Foreign buyers should insist that the review is based on official land registry outputs, not on screenshots from messaging apps. The primary institutional reference point is the Land Registry and Cadastre authority because it frames how records are issued and verified. If an agent offers a photocopy of a Tapu, the reviewer should treat it as a lead, not as proof. A lawyer in Turkey will typically create a verification trail that can be shown to a bank, notary, or court if challenged. The review should also capture whether the property is freehold, share-based, or subject to special registry annotations. Where the property is part of a development, the reviewer should confirm how common areas and management obligations are recorded. A safe workflow is to request a clean document set early, then freeze versions so later changes are visible. If the seller presents multiple versions of the same document, the reviewer should record who provided each version and when. This discipline prevents last-minute substitution of a different unit or a different parcel. It also makes later disputes easier to resolve because each conclusion is traceable to a dated record. For a structured explanation of the steps, you can compare your workflow with this title deed verification guide and then adjust it to the specific asset. The key is that every step should be repeatable by an independent reviewer using the same sources.

In title deed check Turkey practice, the reviewer should separate factual verification from legal interpretation to avoid mixed conclusions. Factual verification includes ownership, property identifiers, and recorded annotations that can be confirmed directly from registry outputs. Legal interpretation then evaluates what those annotations mean for transferability, possession, and future enforcement. Foreign buyers often miss this separation because they focus only on whether the seller appears legitimate. The stronger question is whether the record allows a clean transfer that matches the intended use and financing plan. When the buyer is not in Türkiye, communication gaps can cause misunderstandings about what was actually verified. This is where a law firm in Istanbul can add value by controlling the source documents and keeping a written record of each verification point. A good review also checks whether the seller is acting personally or through representation, because that affects document requirements at closing. If the property is marketed as new or recently renovated, the reviewer should flag that marketing does not substitute for registry and municipal checks. Buyers should also request clarity on whether there are co-owners, because co-ownership can complicate signature requirements. If there are co-owners, the review should identify who must sign and whether any spousal consents are needed in the specific scenario. The reviewer should keep conclusions neutral and avoid promising that an office will accept a specific format without confirmation. “practice may vary by authority and year — check current guidance.” For a broader view of how this fits into a foreign purchase workflow, see due diligence for foreign purchasers and then tailor the checklist to the asset class. A disciplined scope statement for the review prevents later arguments about what was included and what was outside the mandate.

A tapu check Turkey should not be treated as a single document glance, because the Tapu is only the visible summary of a deeper registry record. The buyer should confirm that the summary matches the underlying parcel and independent section data. The check should confirm the title type, the recorded share, and whether the seller’s share is sufficient to transfer the promised unit. If the property is part of a site, the check should confirm how common areas and management rights are recorded. The check should also confirm whether the property is recorded as residential, commercial, land, or another category in the registry context. Category matters because some intended uses can create additional municipal licensing or zoning constraints. Buyers should also ask whether there were recent transfers, because rapid transfers can be a fraud indicator even when documents look clean. If there were rapid transfers, the reviewer should request the supporting sale documents and trace the narrative to objective evidence. The check should confirm whether the property is subject to any pre-emption rights recorded in the registry. It should also confirm whether the property is under any restriction that prevents transfer to certain persons or entities. If the buyer is purchasing through a company, the check should confirm how ownership will be recorded and who will sign at closing. If the buyer is purchasing personally, the check should confirm how identity will be verified and whether translation support is needed at the registry appointment. The reviewer should document every record reviewed and store it with the transaction file. That archive becomes critical if a dispute later arises about what was known at signing. A careful tapu review is therefore both a legal verification and an evidence preservation step.

What the Tapu proves

The Tapu proves what is recorded in the land registry at the time the record is issued, not what is promised in marketing materials. It is therefore a snapshot that must be read together with the underlying land registry records Turkey that support it. The legal framework for registry operations is anchored in Land Registry Law 2644 and related implementing practice. A buyer should focus on the core fields that define the property and the owner rather than on decorative features of the document. Those core fields typically include the parcel identifiers, the independent section number where relevant, and the registered ownership share. The Tapu also reflects certain annotations that can affect transferability, including recorded mortgages and restrictions. It does not, by itself, prove zoning compliance, occupancy permission, or construction conformity. That is why a Tapu review must be combined with municipal and building compliance checks in a complete due diligence file. Foreign buyers should also understand that the Tapu does not replace a properly drafted contract that allocates risks and remedies. If the seller presents a Tapu that is inconsistent with the property shown, the transaction should pause until the mismatch is resolved. If the Tapu shows shared ownership, the buyer should identify every person whose signature may be needed at closing. A best lawyer in Turkey approach is to treat every field on the Tapu as a verification question that must be answered with a source document. The buyer should also confirm whether the Tapu is issued from the correct directorate and whether the issue date is recent enough for the transaction. The issue date matters because annotations can change, and a stale copy may hide a newly registered encumbrance. The Tapu is therefore a starting point for verification, not the end point.

Title deed due diligence Turkey is strongest when it connects registry data to the substantive ownership rules that govern transfer and third-party protection. Ownership effects and property rights concepts are structured under the Turkish Civil Code which frames how rights are acquired and asserted. A buyer should understand the difference between being promised possession and acquiring a registrable right that will be protected against third parties. This distinction becomes critical when disputes arise after payment but before registration. The Tapu proves registration, but it does not automatically prove that the seller has the contractual authority to sell in every scenario. The due diligence reviewer should therefore treat the Tapu as one component within a broader legal package. That package includes the draft sale contract, the identity file, and the evidence pack supporting each representation. A central risk for foreign buyers is assuming that the registry appointment alone will correct contractual weaknesses. The registry appointment records the transfer, but it does not rewrite private obligations that were drafted poorly. This is why Turkish lawyers often insist on reviewing both the registry record and the contract logic in one continuous workflow. When a buyer wants a deeper legal background on property rights and transaction structure, real estate law overview can help anchor expectations before drafting begins. The reviewer should also identify whether the transaction is a sale of a completed unit, a sale of a share, or a sale of land for construction. Each structure raises different risk controls, and those controls should be reflected in the contract and evidence pack. If the buyer is financing the purchase, the reviewer should anticipate the bank’s documentation expectations and align the file early. A coherent due diligence narrative reduces surprises and improves enforceability if a dispute later occurs.

A Tapu document also needs to be read with attention to how information is presented and what is omitted. The document can show registered rights and certain annotations, but it may not display the full history of prior transfers in a way a buyer expects. If the buyer wants to understand the underlying legal vocabulary, reviewing the primary legal texts on the official Mevzuat portal is safer than relying on translated summaries. The vocabulary matters because some annotations sound minor but can affect transfer, financing, or future enforcement. The reviewer should also consider how to obtain certified copies and how to store them, because later disputes often turn on what was shown at signing. If the seller is represented by a company, corporate signatory documents and board resolutions may be needed alongside the Tapu. If the seller is an individual, marital status and co-ownership questions may matter depending on the fact pattern. The Tapu does not substitute for checking whether a seller is under insolvency, guardianship, or other legal disability that affects authority. Where such issues are suspected, the reviewer should request supporting documents rather than relying on verbal assurances. The file should include an audit trail showing who provided each document and the date it was received. If a document is later replaced, the prior version should be kept so the change is visible. This archive approach helps the buyer prove good faith diligence and helps counsel diagnose contradictions quickly. It also protects against pressure tactics in which the buyer is asked to sign before reviewing the updated record. “practice may vary by authority and year — check current guidance.” A Tapu that is treated as a compliance object rather than a brochure makes the transaction materially safer.

Ownership and identity checks

Ownership verification begins with proving that the seller in the contract is the same person or entity recorded in the registry. This step is the core of title deed verification Turkey foreigners because identity mismatches are a common fraud gateway. The reviewer should compare passport or identity data against the registry owner information and against the contract signature block. If the seller uses a different spelling across documents, the reviewer should request a formal explanation document that links the identities. If the seller is a company, the reviewer should verify the company registration details and the current authorized signatories. Authority should be confirmed with up-to-date corporate documents rather than with old scans reused from prior deals. Foreign buyers should also verify that the property shown is not recorded under a different owner within the same family or group. If the seller is married or co-owning, signature requirements can change depending on the exact ownership structure. The reviewer should avoid assumptions and should request documentary proof for any claimed authority. An English speaking lawyer in Turkey can reduce misunderstandings by ensuring that identity documents and translations match the registry terms used in the file. Translation quality matters because a single mistranslated name component can create an apparent mismatch. The buyer should also confirm whether the seller’s identity document is current and valid for use in the closing process. If a seller relies on a foreign identity document, the buyer should confirm that the closing authority will accept the document format. “practice may vary by authority and year — check current guidance.” A clean identity match is the first line of defense against impersonation and unauthorized sale attempts.

Identity checks should be designed to defeat simple fraud tactics like forged passports and substituted signatories. A buyer should ask to see the original identity document and should not rely on a scanned copy alone. If the buyer is not present, the buyer’s representative should record what was seen and keep certified copies where lawful. If the seller claims that the registry record contains an older name format, the seller should provide official proof of the name change. Where the seller is a company, the file should include a current trade registry extract and a signature circular that matches the signing person. If a signatory is acting under a board decision, the board decision should be included and should identify the property and transaction scope. If the property is co-owned, each co-owner’s identity and authority must be verified to avoid partial transfer problems. The reviewer should confirm whether there are minors, guardianship orders, or court decisions affecting the seller’s capacity. Capacity issues should be treated as legal blockers until proven otherwise with formal documents. The buyer should also verify that the seller’s contact channels are consistent and not suddenly changed close to signing. Sudden changes in bank accounts, email domains, or phone numbers are practical red flags that should trigger additional verification. Verification should include confirming the seller’s address and comparing it with any address information shown in registry correspondence. If a broker is involved, the buyer should document the broker’s mandate and avoid paying funds to an unverified intermediary. A disciplined file records every verification step so that later disputes can be answered with evidence rather than recollection. The objective is to ensure that the party receiving the buyer’s money is the same party that can legally transfer the registered right.

Buyer identity checks are also part of due diligence because the registry process can require clear buyer identification at closing. Foreign buyers should ensure their passports and tax numbers are consistent across all documents used in the transaction. If the buyer is buying through a company, the company’s incorporation documents and signatory authorities should be prepared in advance. If the buyer plans to use an interpreter, the interpreter’s role should be defined so the buyer understands each declaration signed at closing. The buyer should also ensure that the purchase contract uses the same spelling as the passport, including any middle names. If the buyer’s name is written differently in a bank account, the buyer should prepare bank confirmation evidence to avoid payment proof disputes later. The buyer should avoid sending sensitive identity scans to unverified persons, because identity misuse can create fraud exposure beyond the property file. When identity documents are shared, the buyer should use secure channels and should record to whom each copy was sent. If a buyer grants a power of attorney for closing, the power of attorney must match the buyer identity data exactly. A mismatch in name spelling can become a delay point that is avoidable with early checks. The buyer should also confirm whether the property is subject to foreign ownership restrictions in the specific region and parcel type. If restrictions exist, the buyer should request written confirmation of the applicable rule from the relevant authority rather than rely on hearsay. Where the buyer is relying on a remote purchase, the file should include a clear audit trail for every step. This audit trail supports dispute prevention because it reduces arguments about who said what and when. Clean identity documentation is therefore a risk control tool, not merely an administrative formality.

Encumbrances and mortgages

An encumbrance check Turkey title deed focuses on whether third-party rights limit the buyer’s ability to use, finance, or resell the property. Encumbrances can be contractual, statutory, or court-driven, and the registry record is the first place to confirm what is recorded. The reviewer should distinguish between items that block transfer and items that survive transfer and bind the buyer. A buyer should not assume that an encumbrance will be cleared automatically at closing without an explicit clearing plan. If a mortgage is recorded, the buyer should confirm whether the sale will proceed with release or with assumption, and the contract should reflect that choice. If an annotation is unclear, the reviewer should request clarification from the seller and seek supporting documents that explain the annotation. Supporting documents may include bank letters, court orders, or prior settlement documents, depending on the source of the encumbrance. The buyer should also confirm whether the encumbrance relates to the whole property or only to a share. Share-based encumbrances can create hidden complexity because the buyer may end up co-owning with an encumbrance still attached to another share. The contract should allocate the risk of non-clearance and define remedies if the encumbrance is not removed. The reviewer should avoid promising that clearance will occur within a fixed period because institutional steps can vary. “practice may vary by authority and year — check current guidance.” If the buyer pays before clearance, the buyer should ensure the payment is structured with strong contractual protection. If the buyer closes with an encumbrance still recorded, the buyer should understand that enforcement may later be directed against the property. Encumbrance review is therefore a central risk control, not a minor technical step.

A mortgage lien check Turkey property should confirm the creditor identity, the scope of the secured obligation, and whether any release conditions are documented. A recorded mortgage can be a routine financing tool, but it becomes a buyer risk if clearance is uncertain or disputed. The buyer should ask whether the loan is still active and whether the seller has requested a payoff statement. If the seller provides a payoff statement, the buyer should verify its authenticity and confirm that it relates to the correct registry record. The buyer should also understand whether the mortgage secures a specific amount or a floating obligation, because scope affects risk. If the mortgage is linked to a commercial facility, the buyer should check whether there are cross-collateral arrangements affecting multiple properties. Cross-collateral arrangements can create surprise claims even after the buyer believes a single property is clear. If a bank requires payment to a specific account, the buyer should treat bank account verification as part of the anti-fraud workflow. The sale contract should state whether the mortgage will be released before transfer or simultaneously, and how evidence of release will be obtained. If simultaneous release is planned, the buyer should coordinate with bank representatives and ensure that written confirmation is produced. The buyer should not rely on verbal statements that the mortgage will be removed, because verbal statements are hard to enforce. If the seller cannot clear the mortgage, the buyer should reassess whether the price and risk allocation remain acceptable. A buyer should also confirm whether there are multiple mortgages, because second-degree mortgages may remain even if the first is released. A careful reviewer will document each mortgage entry and request supporting documents for each one. This documentation supports both negotiation leverage and future dispute prevention.

Encumbrance findings should be translated into a decision memo that the buyer can use to choose between clearing, price adjustment, or walking away. The memo should state which encumbrances are confirmed by registry records and which are alleged but not documented. For confirmed encumbrances, the memo should state what evidence is still missing to confirm clearance mechanics. For alleged encumbrances, the memo should state what additional records must be requested to validate the claim. The memo should also propose contract clauses that allocate responsibility for clearance and specify the proof required. If the buyer is paying a deposit, the deposit clause should be linked to clearance milestones and documented evidence. Where bank involvement is expected, the buyer should ensure that communications are in writing and that representative identities are verified. An Istanbul Law Firm approach typically emphasizes that clearing documents must be obtained from the source institution and stored in the transaction archive. That archive should include dated registry outputs, bank letters, and any signed acknowledgments relevant to release. If a dispute later arises, these documents allow counsel to show that the buyer acted with diligence and relied on verifiable records. The buyer should also consider how encumbrance clearance interacts with tax declarations and payment evidence. A buyer who ignores these interactions may face a situation where the registry transfer is complete but the financial trail is disputed. Encumbrance work is therefore linked to contract drafting, payment planning, and fraud prevention. The safest approach is to keep each risk category in a separate section of the due diligence file while maintaining one coherent narrative. When the file is coherent, the buyer can negotiate confidently without relying on hope or informal assurances.

Liens and attachments

Liens and court attachments are the encumbrances that most often surprise buyers because they may be registered shortly before closing. They can arise from personal debts of the seller, commercial disputes, or enforcement proceedings that have nothing to do with the property itself. A buyer must confirm whether any attachment blocks transfer or whether it allows transfer but continues to burden the property after purchase. The first task is to obtain an official record showing the current annotations and to confirm that the record date is close to signing. The second task is to ask the seller for the underlying decision or enforcement file reference that created the attachment. Without the underlying basis, a buyer cannot judge whether removal is realistic or merely promised. Even when removal is promised, the contract must state who removes it, what evidence proves removal, and what happens if it is not removed. If the seller proposes to clear the attachment on the closing day, the buyer should require a controlled sequence so payment is not released before clearance is proven. Where a buyer pays a deposit, the deposit clause should be tied to documentary proof rather than verbal assurances. Attachments can also be share-specific, which means the buyer may acquire a share while another share remains restricted. Share-specific restrictions can create long-term co-ownership problems that are expensive to unwind. A clean due diligence file therefore checks not only the property but also the seller’s status and the chain of authority behind the sale. If the seller is a company, the buyer should test whether the attachment relates to corporate debts that can trigger broader enforcement pressure. Experienced Turkish lawyers treat attachments as a stop-sign until a written clearance plan exists. The safest posture is to assume the attachment will remain until the buyer sees a source document confirming its removal.

A lien review should also consider whether the property is caught in an inheritance or succession event that changes who can discharge the burden. If the recorded owner has died, the land registry will not treat an informal family agreement as authority to sell or clear liens. Buyers should confirm whether a succession file exists and whether the heirs have completed the steps needed to act on behalf of the estate. This risk is often overlooked in remote transactions where documents are exchanged digitally and the buyer never meets the actual stakeholders. A practical warning sign is when the seller explains the situation through stories but cannot provide an official document that ties the lien to a solvable procedure. If the lien is linked to an enforcement file, the buyer should request a written payoff or release statement from the relevant creditor. If the creditor is a public body or a court-driven enforcement office, the buyer should expect formal paperwork and should not rely on screenshots. Where the buyer needs an overview of succession-related registry risks, this tapu checks after death note helps frame what to verify. The buyer should also verify that any promised release will be registered, because an unregistered release may not protect the buyer against third parties. If the seller insists that clearance is automatic after payment, the buyer should treat that claim as unproven until the record shows the annotation removed. In practice, clearance workflows depend on the creditor and the local office that processes the removal request. practice may vary by authority and year — check current guidance. A law firm in Istanbul will usually insist that the buyer keeps dated registry outputs before and after clearance so the change is documented. That record becomes evidence if a dispute arises about whether the sale was conditioned on clearing the lien. A controlled sequence is the best way to prevent the buyer from paying into uncertainty.

Attachments can become harder to resolve when the transaction involves foreign heirs or cross-border succession disputes. Heirs may disagree on sale authority, and an attachment may be placed precisely to freeze the asset until those disputes are resolved. If a buyer sees rapid changes in the seller narrative, the buyer should consider the possibility of title deed fraud Turkey and pause until the file is verified. A buyer should request the inheritance documentation that proves who can sign and who can give valid release instructions. If the seller uses an intermediary to communicate, the buyer should insist on direct verification of the signing parties. Foreign buyers should be cautious about paying any funds before seeing a coherent authority chain that can be reproduced. Where succession is international, the documentation set often requires careful legalization and translation so that Turkish offices can rely on it. If the buyer needs context on cross-border succession risk, this foreign heirs inheritance overview explains common documentation pressure points. The contract should state that any attachment must be cleared by registration, not merely by promise. The contract should also state who bears the cost and effort of clearance without naming fixed fees or timelines. If the seller cannot produce source documents, the buyer should treat the transaction as high risk regardless of the discount offered. A prudent approach is to require that the seller’s clearance evidence is obtained from the issuing authority and archived in the deal file. A Istanbul Law Firm workflow typically requires a written clearance plan signed by the seller before funds are released. This reduces the chance that the buyer becomes the new owner of an asset that cannot be used or sold. When liens and attachments are addressed with evidence discipline, the rest of the due diligence becomes more predictable.

Easements and restrictions

Easements are registered rights that give someone else a use entitlement over the property, even if the buyer becomes the owner. Common examples include rights of way, utility corridors, access rights, and certain usage rights linked to neighboring parcels. Because they are registered, they usually survive transfer and bind the buyer without any need for a new agreement. A buyer should therefore read each easement entry as a limitation on full control and should ask what activity it permits. The safest approach is to request the underlying deed or agreement that created the easement and to confirm its geographic scope. If the easement affects access, the buyer should physically inspect the access route and compare it with what is recorded. If the easement affects utilities, the buyer should confirm whether maintenance responsibilities are allocated to the property owner. Some restrictions are recorded as annotations that limit certain transfers or uses, and those annotations must be interpreted with the issuing basis. A buyer should confirm whether any restriction requires consent from a third party or an institution before transfer. If consent is required, the transaction should not proceed until the consent document is obtained in verifiable form. Restrictions may also arise from management plan rules in multi-unit properties, which can affect rental, renovation, and common area use. Because management plans can be complex, the buyer should request the current plan and confirm it matches the unit being sold. A buyer should also confirm whether the property is subject to any protected area or cultural heritage restrictions that affect renovation. A lawyer in Turkey will usually translate these entries into practical consequences so the buyer knows what is actually limited. When easements are understood early, the buyer can decide whether the limitation is acceptable or deal-breaking.

Foreign buyers often misunderstand easements because the registry vocabulary does not map directly onto the terms used in other countries. A translation that is technically correct can still be misleading if it fails to explain the practical effect on access and usage. The buyer should insist on a translation that preserves the formal wording while also providing an explanation of operational impact. If the easement grants access to a neighbor, the buyer should confirm whether the neighbor’s access is occasional or continuous. If the easement is linked to a utility provider, the buyer should confirm whether future construction could be limited by the corridor. Some restrictions appear as annotations that look minor but can block financing because banks treat them as transfer risks. If the buyer intends to finance, the buyer should ask the bank what restrictions it considers unacceptable and align the due diligence accordingly. Where a restriction requires institutional approval, the buyer should not assume that approval is routine or guaranteed. The buyer should request written guidance from the relevant institution and attach that guidance to the transaction file. In practice, interpretation can vary between offices and between different types of property. practice may vary by authority and year — check current guidance. Foreign buyers should also confirm whether a restriction affects renting the unit to third parties or using it for short-term stays. If the buyer plans a rental strategy, restrictions should be reviewed as part of the long-term plan, not only for closing. An English speaking lawyer in Turkey can help ensure that foreign buyers understand the registry terms without relying on informal translations. Clarity at this stage prevents disputes where the buyer later claims they were not told about a registered limitation.

Easements and restrictions should be summarized in the due diligence report with direct quotes from the registry output to avoid later reinterpretation. The report should state whether each entry is confirmed by an underlying deed or whether the basis is missing and must be obtained. If the basis is missing, the buyer should treat the entry as a risk until the issuing document is located and reviewed. If the entry is acceptable, the buyer should still ensure that the purchase agreement contains an accurate disclosure clause that matches the record. Disclosure is important because sellers sometimes describe easements as temporary when they are actually permanent. If the seller promises removal, the contract should state that removal must be registered and evidenced by a dated registry output. If the buyer accepts the easement, the buyer should ensure the price reflects the limitation and that future buyers can be informed easily. If the property is part of a site, the buyer should also request the management plan and confirm whether it creates use restrictions beyond the registry. Management plan restrictions can affect renovations, signage, and even pet rules, and these can matter for foreign owners who plan occasional use. The buyer should keep a single archive of the management plan, registry output, and any supporting easement deeds. This archive supports future resale because the buyer can demonstrate transparent disclosure to a later purchaser. It also supports dispute defense if a neighbor later claims a broader right than what was recorded. A disciplined Turkish Law Firm workflow will connect each restriction to a proposed risk control or contract clause. That workflow reduces the chance that a buyer signs a contract with hidden limitations that later restrict use. When restrictions are documented with precision, negotiation becomes rational rather than emotional.

Zoning and usage status

Zoning is where many transactions fail after closing because the buyer discovers the intended use is not compatible with the plan status. A zoning check Turkey property should therefore be treated as a core due diligence stream, not as a last-minute question. The buyer should confirm the current zoning designation, permitted functions, and any plan notes that restrict construction or use. Plan notes can impose hidden limits such as height restrictions, set-back obligations, or density rules that affect redevelopment value. If the unit is in a mixed-use building, the buyer should confirm whether the independent section is registered as residential or commercial in the municipal context. Misalignment between actual use and permitted use can create fines, closure risk, or future resale issues, even if the title is clean. The buyer should also check whether the property sits in an area subject to special planning regimes, such as protected zones or strategic areas. If special regimes exist, the buyer should request official confirmation rather than rely on the seller’s interpretation. Foreign buyers should be especially cautious because they may not be familiar with Turkish municipal processes and terminology. If the buyer is purchasing as an investment, zoning compatibility affects rental strategy, tenant profile, and long-term appreciation. Zoning also affects whether banks will lend, because lenders may treat nonconforming use as a collateral risk. A good due diligence file records the documents used for zoning conclusions and stores them with the transaction archive. If the zoning status is unclear, the buyer should pause the signing process until clarity is obtained from the competent authority. A best lawyer in Turkey approach is to connect zoning conclusions to specific contractual protections and closing conditions. This approach prevents buyers from discovering zoning problems only after payment and registration.

The legal backbone for zoning and construction permissions is rooted in statutory and regulatory frameworks that municipalities apply in practice. For baseline legal reference, buyers can consult Zoning Law 3194 and then confirm how the relevant municipality implements the rules. A buyer should not assume that a building constructed years ago is automatically compliant today, because compliance is assessed against permits and recorded approvals. The due diligence file should therefore include building permit and plan approval documents where available, not only a verbal statement that permits exist. If the property is a unit in a large project, the buyer should request project-level permit data and compare it with the unit being sold. If the seller offers only partial documents, the buyer should treat that as a signal that further verification is needed. Municipal offices may have different document issuance practices and different turnaround depending on workload and local policy. practice may vary by authority and year — check current guidance. The buyer should also consider whether there are pending plan changes or litigation that could affect the area’s future development rights. If plan changes are rumored, the buyer should request written confirmation or official plan extracts rather than rely on neighborhood talk. Where the property is purchased for redevelopment, the buyer should check whether parcel-based limitations exist that block the intended construction. If a consultant provides a zoning opinion, the buyer should ask for the source extracts that support the opinion and store them with the file. A court or bank will rely on source documents, not on an unsigned opinion statement. Clear zoning evidence improves negotiation leverage because the buyer can price risk rather than argue about it. It also reduces future disputes with tenants and neighbors because use boundaries are understood from the start.

Usage status should be checked at both registry and municipal levels because the same space can be described differently across systems. A buyer should verify whether the unit is recorded as residential, office, shop, storage, or another category in the relevant records. If the unit is used as short-term accommodation, the buyer should confirm whether that use is permitted under the building’s management plan and local rules. If the unit is used as an office, the buyer should check whether the building and unit configuration supports that use without unauthorized alterations. Where the seller has made internal modifications, the buyer should assess whether those modifications require permits or approvals. Unauthorized modifications can create inspection risk and can complicate insurance claims after an incident. The due diligence file should therefore include a physical inspection narrative supported by photographs and document references, even when the title is clean. If the buyer is not in Türkiye, the buyer should require a trusted representative to attend the inspection and document the findings consistently. Foreign buyers should also ask whether the building has any outstanding compliance issues noted by the municipality or management. Where compliance issues exist, the buyer should request official letters or meeting minutes rather than accept informal statements. The contract should allocate responsibility for any pre-closing compliance remediation and should define how evidence of remediation will be proven. If remediation is planned, closing conditions should be written so the buyer can refuse closing if the condition is not met. The buyer should avoid closing on the assumption that issues can be fixed easily after registration. A disciplined zoning and usage review turns hidden operational risks into negotiable contract terms. That conversion is the practical reason zoning checks are central to safe purchasing.

Occupancy permit risks

Occupancy permission is a risk category that buyers often ignore because the property looks finished and lived-in. The term iskan occupancy permit Turkey refers to the administrative status that indicates a building is approved for use under the relevant permit framework. A buyer should confirm whether the building has an occupancy permission and whether the unit is covered by that permission. If the building lacks occupancy permission, the buyer should treat the situation as a material risk that can affect utilities, resale, and insurance. Some buildings operate with temporary arrangements, but those arrangements do not always translate into a clean legal status for future transfers. The buyer should request the occupancy-related documentation from the seller and verify it against municipal records where possible. If the seller offers only informal letters, the buyer should seek clarification from the competent municipal unit. The risk is not only administrative, because disputes can arise when lenders or insurers require proof of compliant occupancy. Occupancy status also intersects with tenant relations, because tenants may complain if services are interrupted due to compliance disputes. For investment purchases, occupancy uncertainty can reduce rental stability and can affect how the property is valued by the market. If the property is in a new project, the buyer should confirm whether occupancy permission is issued for the whole project or only for phases. Phased projects can create confusion about which blocks or towers are fully approved. If approvals are phased, the buyer should require a document that clearly identifies the unit’s block and approval status. The contract should allocate the risk of missing occupancy status and should allow the buyer to walk away if the risk is not resolved. A buyer who treats occupancy status as a verifiable condition reduces the chance of post-closing surprises.

Occupancy issues become particularly visible when the buyer intends to rent the property immediately after purchase. If a tenant later disputes habitability or service continuity, the buyer may face operational disputes even when the title is clean. This is why buyers should connect occupancy status to their rental plan and to their contract risk allocation. Where the buyer is planning a long-term rental strategy, this property rental law overview helps frame how disputes arise from building status and documentation. A buyer should also confirm whether utility subscriptions can be opened without additional compliance steps in the specific building. If subscriptions are already in place, the buyer should confirm whether transfer of subscriptions is routine or requires special approvals. Where the seller claims that utilities are permanent, the buyer should request documentary proof rather than accept a verbal statement. If the building is missing occupancy permission, the buyer should assess whether any remediation is planned and whether that plan has documentary support. Remediation plans that depend on multiple owners can fail when consensus is not reached, which leaves the buyer exposed. A prudent file therefore checks the owners’ association or management records to see whether occupancy issues are actively discussed. If management minutes show ongoing disputes, the buyer should treat that as a risk factor and negotiate accordingly. In practice, municipal approaches to occupancy documentation can differ, and buyers should verify the current process with the relevant office. practice may vary by authority and year — check current guidance. The buyer should also consider the insurance angle, because insurers may ask for proof of compliant building status after a claim. A documented occupancy review supports both tenant stability and dispute defense if problems surface later.

Occupancy permit risk should be summarized as a separate section in the due diligence report so the buyer cannot miss it. The section should state what document was reviewed, who issued it, and what dates and identifiers it contains. If no document was provided, the section should state that the status is unverified and explain the practical consequences. If the seller promises to obtain or complete occupancy documentation, the promise should be converted into a closing condition with clear evidence requirements. The evidence requirement should include a dated official document and not a broker letter or a screenshot. If the buyer still wants to proceed despite uncertainty, the buyer should consider structuring payment and closing steps to minimize exposure. Exposure is highest when the buyer pays a large portion before the legal status is verified. A controlled approach is to defer irreversible steps until the key administrative risk is clarified. The contract should also address what happens if the buyer later discovers that the building status blocks the intended use. Remedies should be realistic and evidence-based, because broad remedies without proof triggers create more disputes. Where the seller is part of a developer group, the buyer should confirm who is responsible for municipal follow-up and how that responsibility is documented. If multiple owners must cooperate, the buyer should treat the issue as a collective action risk rather than a simple seller promise. Foreign buyers should ask their representative to obtain written statements from the relevant municipal unit where possible. This documentation can later be used to explain the risk position to lenders, insurers, or future purchasers. A disciplined occupancy review turns a hidden administrative issue into a managed transaction decision.

Building compliance red flags

Building compliance is separate from ownership but it can still destroy the value of a clean title. Buyers often focus on the Tapu and miss that municipal files determine whether the building can lawfully be used as advertised. A cautious approach treats building permits, architectural approvals, and occupancy status as evidence that must match the physical reality. In title deed due diligence Turkey work, you should compare what is built on site to what is authorized on paper. The first red flag is a unit layout that differs materially from approved plans, because later enforcement can require reversal. The second red flag is a building that was expanded, enclosed, or merged without clear permission traces in the file. The third red flag is a project marketed as residential while municipal usage records indicate a different category. A zoning check Turkey property should therefore be paired with a file review of permits and amendments, not only plan labels. If you cannot obtain source documents, you should assume the risk is unresolved and price it or walk away. Site management often holds copies of permits, but those copies must be verified against official sources to avoid outdated versions. Developers may show glossy compliance reports, yet they are not substitutes for official documents that can be produced in a dispute. A buyer should also check whether there are pending municipal orders, inspection reports, or notices that indicate unresolved compliance issues. These orders can affect utilities, renovation, and insurance even if transfer is technically possible. A lawyer in Turkey will usually document each compliance item as verified, unverified, or adverse with a source reference. That classification turns the negotiation into an evidence conversation rather than an argument about opinions.

Another compliance layer is whether the building status aligns with how the unit is described in the land registry and in the sale contract. If the registry shows an independent section but the physical unit was later subdivided informally, the buyer may inherit an unusable configuration. If the registry shows a share in a parcel rather than a clear independent section, the buyer should ask what exactly will be possessed and transferred. The safe approach is to reconcile land registry records Turkey with municipal plan and permit records before any payment is released. A real estate lawyer Turkey title check should include a site visit that compares physical boundaries, entrances, and common areas with documents. If the building has common facilities, the management plan and common area allocations should be checked for restrictions on use and alterations. If the unit has a terrace, storage area, or parking slot, the buyer should confirm whether it is legally part of the independent section or only a usage right. Unregistered usage promises are common in sales marketing, and they often fail when management changes or disputes arise. The buyer should also confirm whether the building is subject to any litigation that challenges permits or construction compliance. Litigation can exist even when residents are living normally, because enforcement can be delayed for years and then become sudden. A prudent reviewer will ask for written confirmation of any known disputes and will keep the answers in the transaction archive. If the seller refuses to disclose, that refusal should be treated as a risk signal and reflected in the contract representations. These steps do not guarantee that an authority will never raise an issue, but they materially improve defensibility. A best lawyer in Turkey approach is to insist that every compliance conclusion is supported by a document that can be reproduced later. This discipline protects the buyer when a future purchaser or a bank asks why the asset should be treated as clean.

Occupancy and completion status is a recurring red flag category because it affects how authorities treat the building in inspections and in utilities. Buyers should confirm whether the building has the relevant occupancy approval and whether the unit is covered by it. If iskan occupancy permit Turkey status is missing, you should expect additional questions from lenders, insurers, and tenants. A missing occupancy status can also indicate that certain permit conditions were not satisfied, such as infrastructure or common area completion. Even when the building is occupied, a later inspection can trigger remedies that are expensive and disruptive. Where a building was altered after completion, the alteration may require a new permit or may be treated as an unauthorized change. Unauthorized changes can also affect fire safety and structural compliance, which raises exposure beyond the transaction itself. A zoning check Turkey property should therefore be re-confirmed when the building appears to contain extra floors, closed balconies, or merged units. If the seller claims that issues are routine and easily solved, the buyer should request written proof of the pending process rather than accept reassurance. If no proof is provided, the buyer should treat the issue as unresolved and reflect it in pricing and contractual conditions. “practice may vary by authority and year — check current guidance.” This variability is exactly why the due diligence file should record which office issued which document and on what date. The buyer should also keep photographic evidence of the physical condition at the time of signing to support later comparisons. If the buyer intends to rent, the buyer should consider how compliance uncertainties can be used by tenants as leverage in disputes. Building compliance red flags are therefore not theoretical issues, but commercial risk drivers that must be managed before closing.

Seller authority verification

Seller authority verification starts with the question of who has the legal power to sign and transfer the registered right. Buyers often assume the person negotiating is the owner, but negotiation authority is not transfer authority. The first step is to match the proposed contract party to the recorded owner shown in land registry records Turkey. If the seller is an individual, capacity issues such as guardianship, restrictions, or representation must be checked through documents, not assumptions. If the seller is a company, the buyer must check the authorized signatories and whether a specific corporate approval is required for the sale. The buyer should also confirm whether the property is jointly owned, because joint ownership can require multiple signatures at closing. If there are multiple co-owners, the buyer should confirm whether each co-owner will attend or provide lawful representation. If the seller is married, the buyer should avoid making assumptions about spousal rights and should verify whether any consent requirement applies in the specific structure. A property purchase agreement Turkey review should therefore include a section that lists every required signer and the evidence for each signer. This signer map should be agreed before deposits are paid to avoid later pressure tactics at the closing desk. A buyer should also check whether the seller is acting under an inheritance situation, because heirs may not yet have a finalized authority chain. If authority depends on court decisions, the buyer should obtain certified copies and confirm they are final and applicable to the property. If authority depends on administrative approvals, the buyer should obtain those approvals in writing and store them in the transaction archive. The reviewer should keep the seller’s declarations and documents aligned, because inconsistency is a red flag in fraud cases. Authority verification is not a courtesy check, but a core condition of a defensible transfer.

Company sellers require extra attention because signatory authority can change and because internal approvals can be overlooked. The buyer should obtain current corporate documentation that shows who can bind the company and under what limits. If the property is a core asset, the buyer should ask whether a board decision is needed and request the decision if applicable. If the signatory is a manager or director, the buyer should check whether their term is current and whether there are restrictions on asset disposals. If the company is part of a group, the buyer should check whether the group uses a holding structure that requires additional consents. A title deed check Turkey is incomplete if it verifies only the registry owner name but ignores corporate authority documents that enable signature. The buyer should also confirm whether the company is under liquidation, restructuring, or enforcement pressure that could disrupt closing. These status questions must be answered with documents such as official extracts and signed approvals, not with verbal assurances. When corporate documents are in a foreign language, translations should be controlled and identity links should be maintained consistently. “practice may vary by authority and year — check current guidance.” Because of variability, a Turkish Law Firm will typically verify with the issuing sources and document the verification steps in writing. The buyer should also ensure that the contract signature block matches the signatory’s exact legal name and title shown in the authority documents. If the signatory signs with an abbreviated title, that mismatch can later be used to challenge validity in disputes. The safest approach is to prepare a complete signing pack and review it before the registry appointment is booked. Authority verification at this stage prevents last-minute cancellations and reduces the risk of paying funds to a party that cannot legally transfer.

Seller authority should also be tested against the practical closing scenario, because authority documents must be accepted by the registry office on the day of transfer. A buyer should confirm that identity documents are valid and that translation support is arranged if the buyer or seller is not fluent in Turkish. If the seller relies on a representative, the buyer should obtain the representative’s identity document and link it to the representation instrument. If multiple parties must sign, the buyer should confirm how the signatures will be coordinated and whether any party is abroad. If a party is abroad, the buyer should confirm whether representation documents will be issued through a notary or a consular channel. The buyer should also confirm whether the seller has any pending disputes with tenants or occupants that could affect possession after purchase. If possession is not delivered, the buyer may face additional litigation even with a clean title transfer. For investment purchases, the authority review should therefore include a practical possession plan and a record of current occupancy. This is part of foreign buyer due diligence Turkey because foreign buyers often cannot manage post-closing disputes from abroad. A law firm in Istanbul can coordinate these checks by keeping a single controlled file that includes authority documents, possession evidence, and disclosure statements. The buyer should insist that all disclosures are written and attached to the contract so they are enforceable. If the seller refuses written disclosures, the buyer should treat that refusal as a signal and adjust price or walk away. Authority verification should end with a written summary that lists the documents reviewed and the remaining uncertainties if any. That summary becomes part of the due diligence report and can be used to justify contractual conditions and payment sequencing. When authority is verified methodically, the closing meeting becomes a formality rather than a last-minute risk event.

Power of attorney risks

Powers of attorney are common in real estate transfers, but they are also a primary fraud vector when buyers are remote. A power of attorney real estate Turkey risk begins with scope, because a narrow instrument may not authorize a sale or may not authorize price and payment terms. The buyer should confirm that the instrument explicitly covers sale, registry signatures, and receipt of consideration where relevant. The buyer should also confirm whether the instrument permits the agent to appoint sub-agents, because sub-delegation can increase fraud risk. If sub-delegation is allowed, the buyer should require disclosure of every sub-agent and should verify their identities. The buyer should confirm the issue date and whether the instrument is still valid for use in the intended transaction. Revocation risk should be evaluated because a principal can revoke and a buyer may not learn of revocation until closing fails. The buyer should ask for evidence that the instrument has not been revoked and should verify through lawful channels where possible. The buyer should also check whether the instrument is limited to a specific property or whether it is overly broad. Overly broad instruments can be used to sell multiple assets and are often seen in title deed fraud Turkey patterns. If the principal is elderly or vulnerable, the buyer should treat capacity and coercion risk as material and request additional verification. The buyer should also confirm whether the power of attorney includes restrictions on price, payment method, or counterparty. If restrictions exist, the contract must mirror them or the transaction can be challenged later. The buyer should not rely on a scanned copy alone and should obtain certified copies and translation support where needed. A rigorous power of attorney review is not an obstacle, but a necessary control that protects both buyer and legitimate sellers.

Authenticity verification is the second pillar, because forged instruments can look convincing to non-experts. The buyer should confirm whether the instrument was issued by a Turkish notary, a foreign notary, or a consular office. The buyer should then confirm whether legalization or apostille steps were completed in a way the Turkish registry office will accept. The buyer should confirm that translations are sworn and that the translator preserved the notarial seals and the signature block wording. If the instrument was issued abroad, the buyer should verify the identity verification method used by the issuing authority. The buyer should also verify that the agent’s signature matches the identity documents presented at closing. If an agent presents a different identity document from what is referenced in the instrument, the buyer should pause until the mismatch is resolved. “practice may vary by authority and year — check current guidance.” Because of this variability, Turkish lawyers often verify both the form and the practical acceptability of the instrument before booking the closing appointment. A tapu check Turkey should therefore include the representation file as a mandatory exhibit, not as an optional attachment. The buyer should also ask whether the principal is reachable for verification and whether a confirmation call is feasible. A confirmation call does not replace legal verification, but it can expose obvious impersonation attempts. If the principal refuses any verification while insisting on quick payment, the buyer should treat that as a high-risk indicator. The buyer should also ensure that the instrument authorizes the agent to sign the specific sale contract, not only to sign at the registry. When authenticity and scope are verified, representation becomes a convenience tool rather than a risk multiplier.

Practical risk control also requires a payment protocol that does not allow the agent to redirect funds without verified authority. The buyer should insist that any bank account receiving purchase funds is in the name of the recorded seller or is otherwise justified by documented authority. If the seller insists that payment must go to the agent, the buyer should require explicit written authority and confirm that the authority is still valid. Where possible, the buyer should structure payments to occur simultaneously with registry transfer so that money is not released into uncertainty. If a deposit is needed, the deposit should be limited and tied to a condition that can be evidenced, such as provision of a certified power of attorney. The buyer should also require the contract to state that any misrepresentation about authority is a material breach with clear remedies. Remedies should be drafted to be enforceable without relying on vague fairness arguments. If the buyer is a foreigner, the file should be prepared so that title deed verification Turkey foreigners standards can be demonstrated later to banks and authorities. The buyer should also ensure that the agent’s communications are preserved, because messaging records can become evidence in fraud disputes. The buyer should not allow the agent to collect original documents without providing receipts and copies. If original documents must be shared for appointment booking, the buyer should use secure channels and keep a record of who received what. The buyer should also confirm that the agent has not presented the same power of attorney to multiple buyers for the same unit. If any duplication is suspected, the buyer should request a written seller confirmation and should consider suspending negotiations. Representation can be legitimate, but it must be verified with the same rigor as ownership itself. When these controls are applied, powers of attorney support efficient transactions rather than enabling fraud.

Payment trail and FX rules

Payment planning is part of due diligence because many property disputes start with an unprovable payment story. A buyer should design the payment trail so that every transfer can be linked to the contract and to the exact property. The concept of payment proof property Turkey means you must be able to show who paid, who received, when it was paid, and why it was paid. If the buyer pays in tranches, each tranche should reference a contractual milestone and should be supported by bank records. Cash payments create evidentiary fragility and increase fraud risk, especially when the buyer is not present at closing. Buyers should prefer bank transfers that show sender, receiver, and reference text that matches the contract file. The contract should also state what constitutes valid payment proof so that the seller cannot later deny receipt without evidence. If the seller requests payment to a third party, the buyer should treat that request as a risk event requiring documented justification. If the seller changes bank accounts close to closing, the buyer should verify the change independently and not rely on forwarded messages. For foreign buyer due diligence Turkey, payment controls are essential because remote buyers are targeted by account substitution fraud. The buyer should keep a single payment folder that stores bank confirmations, SWIFT messages where relevant, and correspondence about payment instructions. The buyer should also align payment steps with the registry appointment schedule to reduce the time between payment and registration. If payment must occur before registration, the buyer should include protective clauses that condition payment on objective documentation. The buyer should avoid making payments based on promises that a document will be obtained later, because those promises are hard to enforce. A clean payment trail is a risk control that supports both fraud prevention and later tax and banking explanations.

Foreign currency flows add another layer because banks and authorities may expect documentation that explains the source and purpose of funds. Buyers should understand that FX documentation requirements can change and can differ depending on banking practice and transaction structure. “practice may vary by authority and year — check current guidance.” A prudent buyer will therefore align the payment plan with current banking documentation expectations before committing to a fixed closing date. The buyer should avoid sending funds through informal intermediaries or exchange offices without clear documentary support. If the buyer converts currency for the purchase, the conversion record should be stored with the transaction file as part of payment proof property Turkey. Where the transaction involves formal FX documentation, the buyer can review foreign currency documentation context to understand how evidence is typically organized. The contract should state the currency, the payment method, and the reference language to be used in transfers. If a seller insists on receiving funds in a different currency from the contract currency, the buyer should require an amendment and keep it in the file. The buyer should also confirm whether the seller’s bank account can receive the incoming currency without delays or returns. Returns can create timing stress that fraudsters exploit by pushing the buyer to send replacement payments quickly. An English speaking lawyer in Turkey can help foreign buyers align contract wording with the practical documentation that banks will produce. The buyer should also ensure that any escrow or holding arrangements are described in writing and are not based on informal trust. Payment instructions should be confirmed through at least two independent channels to reduce the risk of email compromise. When FX and payment evidence is prepared early, closing becomes a controlled execution step rather than a hurried improvisation.

Buyers who are not resident in Türkiye should also plan the banking logistics so payments can be executed safely and on time. If a buyer needs a Turkish account, remote preparation may be possible depending on the bank and the buyer profile. The buyer can review remote account opening considerations to understand what documents are typically requested. Bank onboarding should be started early because missing documents can trigger last-minute pressure to use third-party accounts. Third-party accounts are a common fraud channel and create later proof disputes, so they should be avoided unless fully documented and justified. The contract should also define the timing of payment relative to signing and registry transfer, and the buyer should follow that sequence strictly. If the seller requests a change in timing, the buyer should document the change formally and re-verify bank details. Payment proof property Turkey should include not only the transfer confirmation but also the contract clause that the payment satisfies. Buyers should also consider that taxes and declarations can require consistent documentation, especially when funds move across borders. For a practical overview of tax touchpoints in purchases, real estate taxes overview can help frame the evidence you should keep. The buyer should keep copies of contract versions, bank confirmations, and any seller payment acknowledgments in a single archive. If the buyer expects to rent the property later, preserving this financial archive also supports future questions about income and expense documentation. An Istanbul Law Firm style workflow typically treats the payment folder as a litigation-ready exhibit that must remain coherent. This does not guarantee that disputes will never arise, but it makes disputes easier to resolve because evidence is organized. A controlled payment trail also reduces the chance that a fraud attempt succeeds through urgency and confusion.

Due diligence report structure

A due diligence report must start with an executive summary that states what was checked and what was not checked. It should identify the exact parcel and independent section data so the reader can match the report to the registry file without interpretation. It should then list the sources reviewed, including dated registry outputs, seller-provided documents, and municipal extracts where available. Each source should be described with its date and origin so later disputes cannot claim the report relied on unknown material. The next section should address ownership, identity, and authority as separate findings rather than mixing them into one conclusion. After that, the report should address encumbrances, attachments, and restrictions with the exact wording of the annotation where possible. The report should state whether each annotation blocks transfer, survives transfer, or requires third-party action, but it should avoid promising a clearance timeline. Zoning and building status should be captured as a separate risk line that distinguishes registry status from municipal compliance status. Occupancy permission should be treated as its own finding because it affects financing, rental strategy, and insurability. When an issue is unverified, the report should say unverified and specify the missing document rather than infer the answer. A buyer-focused report should also include a proposed contract protection for each material risk so the report is actionable. Where payments are contemplated, the report should describe an evidence-based payment protocol that keeps funds tied to verifiable milestones. If the buyer is foreign, the report should note translation and interpretation needs for closing so declarations are understood. A report prepared through a Turkish Law Firm should be written so that a bank, notary, or court can follow it without needing verbal explanation. The report should end with a decision section that clearly states whether to proceed, renegotiate, or pause pending documents.

The evidentiary annexes should be organized to mirror the report sections so the reader can jump from a conclusion to the supporting page quickly. Registry outputs should be saved in the same form they were received, including page headers and issue dates. If the seller provides copies, the report should mark them as seller-provided and should state whether an official counterpart was obtained. Where municipal documents are used, the report should name the municipality department or portal used, and it should preserve the extract as an exhibit. If the transaction includes a company seller, the report should attach the signatory documents and the approval decision relied on for authority. If the seller uses representation, the report should attach the power of attorney and explain the scope and any limits that were identified. If any discrepancy exists between documents, the report should quote the discrepancy and describe the risk rather than trying to reconcile it creatively. The report should avoid numerical promises about timing, because administrative workflows fluctuate and the buyer may rely on the number as a guarantee. “practice may vary by authority and year — check current guidance.” Where a question depends on an office’s practice, the report should state the verification step needed, such as obtaining a written response or a stamped extract. A cautious reviewer will also log every call and email in a separate communication sheet that can be produced later if needed. The report should include a clear instruction that no funds should be released to unverified accounts, even if pressure is applied. It should also include a reminder that the final condition is the updated registry record after closing, not the pre-closing copy. In practice, a lawyer in Turkey will draft the report language to be defensible under cross-examination rather than impressive to a sales team. That defensibility comes from stating facts, naming sources, and describing missing evidence without filling gaps with assumptions.

A good report should also include a closing conditions section that lists which documents must be produced before the buyer signs or pays. Those conditions should be written in objective terms, such as a dated registry extract showing removal of a specific annotation. If a condition cannot be met, the report should describe alternative structures, such as postponing closing or revising the price allocation. The report should also recommend how the buyer stores originals and translations so the post-closing file remains coherent. Post-closing storage matters because later resale, financing, or inheritance planning often depends on the same documents. The report should explain how the buyer can confirm that utilities and management records are transferred without treating those steps as guaranteed. If the buyer plans to rent, the report should advise that tenancy documentation should be separate from the purchase file but cross-referenced. For foreign buyers, the report should also advise on securing certified translations of key documents for use abroad if needed. The report should treat any unresolved risk as a live risk and should avoid language that implies it will disappear automatically. The report should also recommend a second check immediately before the registry appointment because last-minute annotations can appear. This second check is not a distrust signal, but a standard fraud prevention technique in high-value transactions. If the seller refuses the second check, the report should flag that refusal as a risk indicator. The report should keep the buyer’s decision-making rational by tying each risk to a practical consequence and a proposed control. When the buyer follows the report structure, the transaction becomes a controlled process rather than an emotional negotiation. The output should be a file that the buyer can hand to another professional and receive the same conclusions from the same sources.

Fraud patterns and prevention

Fraud in property transactions usually begins with urgency and information asymmetry rather than with sophisticated paperwork. A common pattern is the substituted unit, where the buyer tours one unit but is asked to sign for a different independent section in the registry. Another pattern is the impersonated owner, where a forged identity document is used to support a fake representation story. A third pattern is account substitution, where the buyer receives a new bank account instruction shortly before closing through a compromised email. Buyers should treat sudden changes in bank details, meeting location, or intermediaries as red flags that require independent verification. The term title deed fraud Turkey covers these patterns because the exploit is usually the gap between what the buyer believes and what the registry will record. Buyers who want a deeper risk taxonomy can review fraud pattern guidance and then test each risk against the current file. Fraud also appears as double-sale attempts, where a seller negotiates with multiple buyers and tries to collect deposits quickly. Another fraud variant uses a broad power of attorney to sell assets rapidly before revocation is discovered. Some schemes rely on fake municipal documents that claim compliance or occupancy status without official provenance. The most effective defense is to standardize verification steps and refuse to proceed when a source document cannot be authenticated. A buyer should also confirm that the broker’s mandate is real and that the broker is not merely a messenger for an unverified seller. When foreign buyers are targeted, the fraud often relies on language barriers and on the buyer’s reluctance to slow down the deal. A law firm in Istanbul should therefore design the process to remove speed pressure and replace it with verifiable steps. Fraud prevention is not pessimism, but a routine control that protects legitimate sellers as well as buyers.