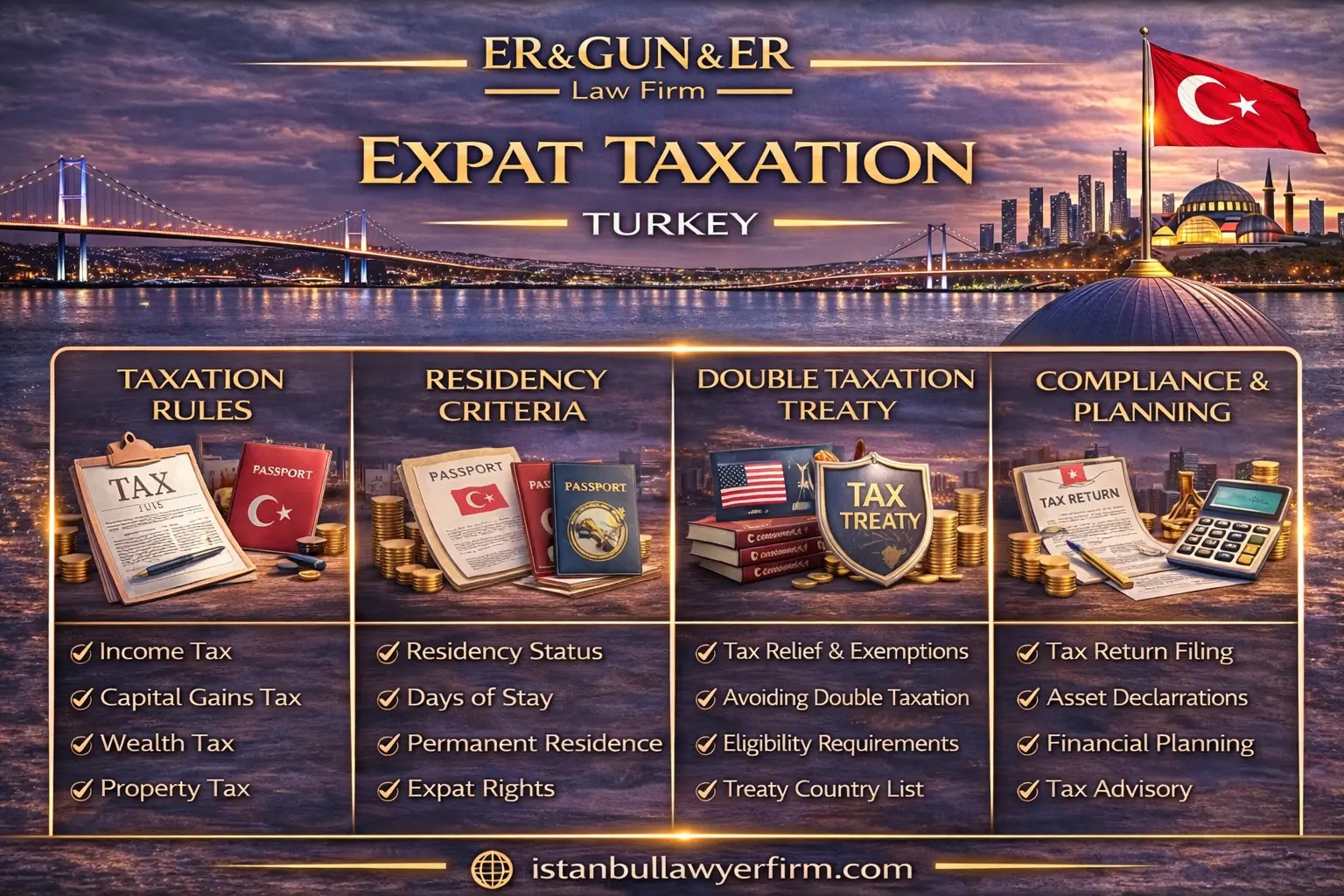

Expat taxation Turkey is not a single rule, because the outcome changes with residency classification, income source, and the documentation trail you can produce. A foreign national can hold a residence permit and still be treated differently for tax purposes if the statutory tests point to a different status. The most common failure in expat files is not a complex treaty issue, but a missing chronology of where the work was performed, where the payer is located, and which bank account received the income. Policy-grade compliance begins by identifying your taxpayer profile, then mapping each income stream to a Turkish charging rule and a reporting channel. Your file must be evidence-led, because authorities and courts decide on documents, not on explanations provided after the fact. In practice, the same income can be treated differently when it is employment, self-employment, or business income, and misclassification is a frequent audit trigger. tax compliance for expatriates in Turkey depends on keeping your residence evidence, contract set, invoices, and bank receipts aligned month by month. If you need bilingual coordination, English speaking lawyer in Turkey support is useful when it keeps terminology consistent between Turkish filings and foreign accountants. practice may vary by authority and year — check current guidance.

Residency status and scope

Residency analysis starts with identifying whether you are treated as a full taxpayer or limited taxpayer under Turkish income tax concepts. For expats, tax residency Turkey foreigners classification is usually determined by objective ties, not by personal preference statements. The first evidence layer is your domicile and habitual living arrangement, including where your family and permanent home are located. The second evidence layer is your physical presence and the presence-based test defined in the Income Tax Law, which should be checked in the official statute text. Use the Mevzuat portal as the baseline source and avoid relying on informal summaries for residency triggers. Where you need the primary law text, consult the Income Tax Law page and read the residency and taxpayer sections together with the scope rules. A clean residency file also includes address registration records, residence permit history, and travel logs that reconcile entry and exit dates. Employment presence should be mapped carefully, because performing services physically from Türkiye can create a domestic source position even when the employer is abroad. Business presence should also be mapped, because management activities and decision making performed in Türkiye can change the analysis. If you are in Türkiye on short stays, keep hotel invoices and flight tickets because they can prove presence patterns when passports are unclear. If you hold a long-term lease, keep the lease and utility subscriptions because they are often treated as strong indicators of permanence. If you are unsure how the residency tests apply to your facts, use a structured checklist like the internal tax residency guide to map indicators before you file. Do not assume that immigration status equals tax status, because the tests and their evidence are different. Residency classification must be decided before you aggregate income, because the scope of taxation follows the residency result. practice may vary by authority and year — check current guidance.

After residency is classified, the next step is to define the scope of taxation, because full taxpayers are generally assessed on broader income categories than limited taxpayers. The scope question is evidence-driven, because authorities test whether income is connected to Türkiye by looking at work location, payer location, asset location, and bank trails. income tax for expats in Turkey planning therefore starts with a source-of-income map that separates Turkish-source items from foreign-source items. A reliable map records where services were performed, where clients were located, and where contracts were signed and managed. If you work remotely, keep time records and location logs because the same contract can generate different tax outcomes when performed from different countries. If you have mixed residence ties, treat the analysis as a risk matrix rather than as a binary conclusion, because tie-breaker issues may arise under treaties. Do not rely on a single certificate such as a residence card to prove tax position, because the position is built from multiple indicators. Bank accounts are relevant because payment flows show where income was received and which jurisdiction may have withholding or reporting data. When you receive payments into Türkiye, maintain invoices, engagement letters, and bank reference lines so that the payment is linked to the correct income category. When you receive payments abroad, keep foreign bank statements and foreign withholding proofs so that you can reconcile foreign tax outcomes with Turkish reporting where required. If you hold shares or invest through companies, document where management decisions are made because corporate control can affect personal tax narrative. In complex files, lawyer in Turkey review is useful when it tests whether each claimed classification is supported by at least two independent documents. This review should also test whether your narrative is consistent across immigration records, municipal address records, and tax office registrations. A scope analysis should be updated after major life events such as marriage, relocation, or business formation, because those events change the indicator set. practice may vary by authority and year — check current guidance.

Residency and scope are not operational until the taxpayer can interact with the tax administration through the correct identifiers and portals. Turkish tax identification number for foreigners is the practical gateway, because banks, notaries, employers, and many registries ask for it to process transactions. The Revenue Administration provides a digital channel for foreigners to obtain a potential tax number, and the official entry point is the potential tax number application. Keep a PDF or screenshot of the output page as evidence, because later registrations may require proof of how the number was obtained. If you later obtain a residence permit or citizenship, ensure that identifier records are aligned, because mismatched spelling across passports can create account opening delays. If you become an employee, your employer’s payroll systems may also require consistent identifiers for withholding and social security reporting. For self-employment or business registrations, the identifier will be used to open e-filing access and to link invoices to declarations. Use official guidance pages on the Revenue Administration site, such as the GİB portal, for current service descriptions rather than relying on third-party blogs. When you receive your number, document where you used it first, because early uses often reveal mismatches that should be corrected before annual filing. Do not share your identifier and passport scans casually with intermediaries, because data misuse can create new compliance and fraud risks. If a bank requests additional KYC documentation, keep the bank checklist and submission receipts because those documents often become relevant in audit questions about income flows. If you change addresses, update your records consistently across immigration, bank, and tax interfaces, because inconsistent addresses often trigger automated questions. If you are treated as non-resident for Turkish tax purposes, you may still need an identifier to handle withholding processes, property rentals, or one-off filings. The safest approach is to treat identification and registration as part of your evidence strategy, not as a clerical formality. practice may vary by authority and year — check current guidance.

Income categories framework

Once residency is understood, the next disciplined step is to classify each income stream into the correct Turkish income category. Classification is not semantic, because each category has different documentation, withholding, and filing mechanics. The Income Tax Law sets out income categories for individuals, and the safest reference remains the official statute text rather than unofficial tables. A foreign professional who receives payments from abroad must still test whether the activity is performed in Türkiye, because performance location can change classification consequences. A foreign entrepreneur with a Turkish company must separate personal income from corporate income, because mixing them creates both tax and accounting risk. Rental income must be separated from service income, because property usage contracts are treated differently from consulting or management services. Investment income streams must be separated by type, because the treatment of dividends, interest, and funds can differ and is often implemented through withholding. Capital gains must be mapped to the underlying asset and to the holding structure, because the asset type and ownership form can change the tax base narrative. Cross-border payments should always be linked to a contract and an invoice or payslip, because a bare bank transfer is rarely enough in an audit setting. For a practical template on how Turkish tax assessments are built and how authorities test classifications, review the internal income tax assessment guide. This type of template helps expats build a file that answers where the income came from, what activity produced it, and what documentation supports it. Classification should also consider whether the income is regular and continuous, because continuity can affect whether an activity is treated as business-like rather than incidental. If you have multiple streams, map each stream to a separate folder with its own contracts, invoices, and bank receipts, because mixing folders creates contradictions. When documentation is inconsistent, the authority may reclassify income, and reclassification can expand the scope of questions beyond the initial return. practice may vary by authority and year — check current guidance.

In expat files, the most common classification error is treating all foreign-source money as non-taxable without testing source rules and residency scope. A second common error is treating Turkish-source payments as foreign because the payer is abroad, even when services are physically performed in Türkiye. A third error is treating reimbursements, allowances, and per diems as tax-free without checking whether the policy and payroll documentation supports that characterization. The safest remedy is to build a category map that includes contract clauses, job descriptions, and proof of where work was performed. If the income is employment, keep payroll slips and employer letters that show the employer entity and work location. If the income is self-employment, keep engagement letters, invoices, and proof of client acceptance of deliverables. If the income is business income, keep company financial statements and board minutes that show the activity and control structure. If the income is rental, keep the lease, bank receipts, and any withholding documents if a tenant is required to withhold. If the income is investment, keep bank statements that show the instrument type, the payer, and any withheld amounts. Classification also affects how foreign tax paid is treated, because only certain taxes and only certain income links are accepted as creditable in practice. When foreigners operate through mixed personal and corporate structures, an early classification audit by Turkish Law Firm counsel can prevent a later file from becoming an inconsistent hybrid that is hard to defend. The audit should focus on what evidence exists today and what evidence can be created lawfully going forward, not on retroactive wishful reconstruction. If you cannot verify a position from an official source or your own documentation, treat it as uncertain and document the uncertainty in your compliance notes. This approach protects you because a cautious file is easier to correct than a confident file based on assumptions. practice may vary by authority and year — check current guidance.

A classification map must also consider whether you are filing as an individual taxpayer or through an entity, because filing channels and books differ. Individuals may rely on annual returns and withholding statements, while entities may rely on monthly declarations and statutory books. Even when an accountant prepares filings, the taxpayer remains exposed if the source documents do not exist or are inconsistent. Expat compliance is therefore a coordination exercise between legal analysis, accounting execution, and documentary discipline. For example, a consultant paid from abroad should still keep a Turkish-facing invoice or service record if Turkish rules require it for the activity type. A foreign company with a Turkish branch should keep branch records separate from head office records to avoid mixed-source confusion. A foreign employee on a Turkish payroll should keep an employment file that includes the contract, payroll slips, and employer notifications. A person earning rental income should keep monthly folders that include bank receipts and tenant communications about payment allocation. A person earning investment income should keep broker statements and corporate action notices that explain why payments were received. When a return is filed, store the filed version and the submission receipt, because later disputes often turn on what was actually declared. When an authority asks a question, answer with exhibits and not with narrative alone, because exhibits reduce misunderstandings. If a document does not exist, state that it does not exist and explain what alternative proof exists, because silence invites adverse inferences. Documentation discipline is also a fraud-prevention tool, because intermediaries are less able to manipulate a well-organized record. A coherent category map makes later treaty analysis and foreign tax credit analysis more reliable, because treaty relief depends on the income category. practice may vary by authority and year — check current guidance.

Employment and payroll logic

Employment income is usually the most visible expat income stream because it is tied to payroll, withholding, and social security reporting. payroll tax Turkey expats risk typically arises when the employer assumes that a foreign employee is outside Turkish payroll simply because salary is paid abroad. social security contributions Turkey foreigners can be triggered by the work permit and the actual work performed in Türkiye, so payroll and SGK status must be aligned. The correct first step is to identify the employing entity and the contractual work location, because these facts determine who withholds and who reports. A written employment contract is not only a labor law document but also a tax evidence document, because it fixes role, remuneration structure, and benefit allocation. For contract and file discipline, use the internal employment contract guide as a baseline and ensure the signed version matches payroll practice. Where the employee file is incomplete, disputes often arise later about whether allowances were salary, reimbursement, or expense, and that classification affects tax treatment. A clean employee file should therefore store the contract, job description, payroll slips, and employer correspondence in one chronology. For a practical file framework, review the employee file documentation guide and adapt it to expat onboarding. Social security registration and payroll reporting should be cross-checked against the insurer’s own records, and the starting point for official references is the SGK portal. Employers should avoid paying part of remuneration off-payroll, because off-payroll payments create proof gaps and can trigger audit questions. If the employee works remotely, the contract and payroll files should reflect the remote work structure and the expense reimbursement logic. For remote models, consult remote work compliance guidance and keep wage, expense, and reporting narratives consistent. In practice, coordinated review by a law firm in Istanbul is useful when it tests whether payroll records, bank receipts, and employment documents describe the same remuneration story. practice may vary by authority and year — check current guidance.

Payroll disputes are usually evidence disputes because the authority reads the payslip, the bank transfer, and the contract as one integrated record. If the payslip shows one amount and the bank receipt shows another, the authority will ask for the reason and the supporting document that explains the difference. If the payslip includes allowances, store the policy that governs allowances and store expense receipts where the allowance is reimbursement-like. If the payslip includes bonuses, store the bonus policy and store the approval email that shows why and when the bonus was earned. If the employer provides accommodation, the lease and payment trail may become relevant, so keep the accommodation arrangement documented and consistent. If the employer provides a company car or other benefits, keep benefit policies and usage logs because those facts can become relevant in a tax classification dispute. When an expat is seconded, the secondment letter, the home payroll record, and the Turkish work record must be reconciled to avoid double reporting or under-reporting. A secondment file should also track who bears salary cost and how that cost is recharged between entities, because recharge language often drives audit questions. If the employer is foreign and has no Turkish entity, the classification may shift toward permanent establishment and withholding obligations, so corporate tax counsel should be involved early. Employees should keep their own personal copy of all payslips and employer notices because corporate HR systems are not always accessible after termination. If employment ends, keep termination documents and final payroll statements because those documents often contain settlements and releases that later affect tax narratives. Avoid signing broad settlement texts without understanding how they allocate payments, because allocation affects how amounts are treated in future filings. Where disputes arise, respond with documents, not with general explanations, because document-based responses close gaps faster. Employers should align payroll reporting with bank reference lines to avoid confusion about what a payment represents. practice may vary by authority and year — check current guidance.

Employment tax risk is often created by small inconsistencies that appear harmless during the year but become decisive during an audit. Examples include missing contracts, missing expense receipts, and inconsistent address registrations across payroll and immigration records. If an employee is paid partly from abroad, the employee should keep foreign payslips and foreign bank proofs so the combined remuneration story is provable. If an employer reimburses business travel, keep travel itineraries and invoices because reimbursements are often challenged when documentation is weak. If an employee works partly abroad, keep travel logs because work-location splits are frequently requested when treaty issues are raised. If a foreign employer coordinates with a Turkish payroll provider, confirm in writing which party is responsible for filings and store the service agreement. If the employee receives equity or share-based benefits, document the plan documents and vesting events carefully because the timing and classification can be complex. Do not rely on generic internet tables for equity taxation because treatment depends on plan structure and actual documentation. If an employee is in Türkiye under a work permit, coordinate immigration and payroll narratives so that the declared employer matches the employer in the permit file. Where records are scattered, the insured position becomes harder to defend, because the authority can select the most unfavorable interpretation among inconsistent records. The practical solution is to keep a monthly compliance folder that contains payslips, bank receipts, and employer correspondence for that month. If you cannot reconstruct a month, document the gap and plan corrective documentation going forward rather than inventing a story. In high-value or cross-border employment structures, best lawyer in Turkey level review is useful when it prioritizes evidence integrity and consistency across payroll, tax, and immigration records. This review should also align with treaty analysis and social security coordination, because misalignment across those systems is a common trigger for questions. practice may vary by authority and year — check current guidance.

Self-employment income issues

Self-employment disputes arise when foreigners deliver services into Türkiye or from Türkiye without clarifying whether the activity is treated as independent professional work or business activity. The first step is to define the contracting model, because a service contract, a consultancy arrangement, and a business sale are not treated the same for tax and reporting. If you invoice Turkish clients, your invoices, contracts, and bank receipts must align so that the authority can trace each payment to a specific service period. If you invoice foreign clients while working physically in Türkiye, you must still test whether Turkish-source rules apply based on where the service is performed. If you operate regularly, consider whether you need a Turkish business structure or registration rather than treating each invoice as a one-off. Choosing a structure requires understanding liability, governance, and tax interface, and the internal company types guide provides a practical overview of the main forms. Structure choice should also consider whether you will hire employees, because payroll and SGK compliance can trigger additional reporting layers. Foreign consultants often confuse business registration with a residence permit, but those are different systems with different evidence requirements. Self-employment income must be supported by a contract file that shows scope, pricing, deliverables, and acceptance, because informal messages are weak evidence. Payment receipts should include reference lines that match invoices, because mismatched references are a common audit trigger. If you receive cash, create a signed receipt and deposit cash into a bank account promptly to avoid proof gaps. If you use platforms or intermediaries, keep platform statements and fees records because authorities often test gross versus net receipts. In complex files, Turkish lawyers typically focus on mapping where the value was created and ensuring that the documentary chain supports that map. This mapping is also the foundation for treaty analysis and foreign tax credit positions later, because treaty relief depends on the income category and source. practice may vary by authority and year — check current guidance.

Many expats run foreign companies while physically working from Türkiye, and the risk is that operational reality can create a Turkish tax footprint even when the company is registered abroad. The analysis starts with whether there is a fixed place of business, a dependent agent pattern, or management activity in Türkiye that can be characterized as a taxable presence. Do not rely on generic internet definitions of permanent establishment, because the analysis depends on facts and on treaty interaction with domestic rules. If you plan a formal branch, you must align corporate resolutions, tax registrations, and bookkeeping with Turkish requirements rather than improvising after signing client contracts. A practical overview of branch formation steps and documentary expectations is provided in the branch office guide. Where a branch is not appropriate, a local subsidiary may be considered, but that decision should be made together with tax and liability planning. If you sell digitally into Türkiye, you must map where customers are, where payment is processed, and whether local invoicing obligations apply. E-commerce and platform-based revenue often generates multiple fee layers, so documentation must show gross receipts, platform commissions, and net remittances. For platform-based structures, consult foreign e-commerce tax guidance to understand the compliance logic without assuming thresholds. In self-employment disputes, the authority often tests whether the activity is continuous and organized, which can shift the income category and filing model. If you use a Turkish address for bank accounts or invoicing, ensure that your address registrations are consistent, because inconsistent addresses trigger questions. If you hire contractors in Türkiye, keep contracts and payment proofs because those payments can create withholding and reporting obligations for the paying entity. In practice, Istanbul Law Firm coordination is valuable when it aligns corporate structuring, invoicing practice, and treaty narrative so that each document points to the same conclusion. This coordination also prevents a common error where the expat treats company income as personal income, then later tries to reverse the characterization under audit pressure. practice may vary by authority and year — check current guidance.

Self-employment files are often selected for review when bank inflows are high but the taxpayer record does not show a consistent invoicing narrative. The best defense is to keep an engagement folder for each client that includes contract, scope changes, deliverables, and acceptance evidence. For each payment, store the invoice and the bank receipt in the same folder and ensure the reference line matches the invoice number or period. If you are paid by platforms, store platform statements and settlement reports so the authority can see the gross-to-net reconciliation. If you incur business expenses, store invoices and payment proofs, because expenses are often challenged when they are not tied to business activity clearly. If you work from shared offices or coworking spaces, store membership contracts and invoices because they show the place-of-business narrative. If you travel frequently, store travel itineraries because they support your work-location mapping and help rebut incorrect residence assumptions. If you claim that income is foreign-source, preserve proof that services were performed outside Türkiye, such as flight records, hotel invoices, and meeting logs. If you claim treaty relief, ensure the treaty analysis is consistent with your domestic classification and with your foreign filings, because inconsistency is a common audit trigger. If you issue invoices in a foreign system, keep the invoice copies and their translations if needed, so the Turkish file is readable and complete. If you use a Turkish bank account, keep monthly statements and annotate each incoming transfer with the corresponding invoice reference. If you keep accounts in foreign banks, preserve those statements as well, because authorities often test total inflows against declared income. A disciplined self-employment file also supports personal immigration applications, because income proofs are often requested for residence and work permit renewals. Avoid retroactive reconstruction after the authority requests documents, because late-created documents are easier to attack than contemporaneous records. practice may vary by authority and year — check current guidance.

Rental income documentation

Rental income is a frequent Turkish tax touchpoint for expats because it leaves visible bank trails and third-party records. The first control is to confirm who is the legal landlord in the title record and who signed the lease. If ownership is shared, your file must show who receives rent and how it is allocated. The lease should state the rent amount, currency, payment date logic, and which bank account is the payment account. For rental income tax Turkey expats compliance, bank transfers are safer than cash because they create an independent timestamp. Each payment should carry a clear reference line that links the month to the property address or contract number. If you use an agent or property manager, store the management agreement and the remittance statements as part of the same monthly folder. If the tenant pays utilities or common expenses, record in writing whether those payments are rent substitutes or reimbursements. Ambiguous reimbursements are a common audit trigger because they inflate or deflate the declared base without explanation. A practical discipline is to keep the lease, bank statement page, and any receipt in one monthly PDF set. The internal rental income tax guide provides a useful checklist for how those exhibits should be organized. Where invoices are part of the file, the internal invoice conditions overview helps align the tenant-facing documents with your bank trail. Official practical guidance is also published by the Revenue Administration on the GİB portal, and you should keep printouts of any guidance you rely on. If you rely on administrative guidebooks, archive the version and date because guidance wording can change over time. practice may vary by authority and year — check current guidance.

Documentation issues usually arise when rent is collected in mixed currencies or through mixed channels and the file cannot explain the reconciliation. Keep one master rent ledger that matches the bank statement totals and that shows any months of vacancy explicitly. If the property is vacant, store evidence of vacancy such as utility readings, listing screenshots, and agent messages, because silent gaps look like unreported cash rent. If the tenant paid a deposit, store the deposit receipt separately from rent receipts so the deposit is not misread as rent. If the lease is amended, store the signed amendment and do not rely on chat messages as the amendment record. If the tenant is a company, store the tenant’s company details and the authorized signatory pages because they help explain payment references and invoice requests. If rent is paid via international transfer, store SWIFT confirmations and value dates so timing disputes do not arise later. Where you use e-documents, your recordkeeping obligations are usually anchored in the Tax Procedure Law framework, which can be checked on the Tax Procedure Law text. Do not treat document format as purely technical, because format determines whether a record is accepted as proof in an audit or dispute. Rental taxation rules are also grounded in the Income Tax Law, and the safest reference is the Income Tax Law text. If you are unsure which declaration channel applies to your facts, use official step descriptions in the GİB publications rather than relying on brokers. A current example of official explanatory material is the Revenue Administration guidebooks served through its document system, such as the taxpayer guidebook. When you cite a guidebook internally, keep a note showing which page you relied on and what document in your file supports the same point. If the property is short-term rented through platforms, keep platform payout statements and guest identity records because reconciliation is tighter in practice. practice may vary by authority and year — check current guidance.

Rental files become cross-border when the landlord is paid from abroad, uses a foreign bank, or remits rent proceeds out of Türkiye. Banks often ask how the inflows relate to leases, and they expect a clean set of exhibits rather than long stories. If you plan to move proceeds abroad, build a package that includes the lease, bank receipts, and any tax filing outputs tied to the period. Do not assume a bank will accept a single screenshot of a lease, because banks often request signed pages and identification of the tenant. If you use a property manager, require monthly reconciliations that show gross rent, expenses paid, and net remittance. A management compliance lens is explained in the property management law guide, and the same discipline helps in tax and banking questions. If the tenant pays in cash, insist on a detailed signed receipt and deposit the cash promptly, because cash without deposits creates a proof trap. If the tenant pays from a third-party account, document the relationship and request a written explanation to prevent mischaracterization. Where banks ask for source narratives, keep a standardized response pack and avoid improvising different explanations to different institutions. The internal source of funds verification guide is useful for structuring those packs in a way that survives compliance review. If the property is co-owned, align the bank inflows with the co-ownership arrangement and keep proof of transfers between co-owners where they occur. If you have expenses paid by the manager, keep invoices and approvals, because expenses are often used to challenge net rent figures in disputes. If you are audited later, the same pack will be used, so treat bank compliance outputs as part of your long-term tax archive. Avoid mixing personal transfers and rental transfers in one account without labels, because unlabeled transfers invite classification questions. practice may vary by authority and year — check current guidance.

Investment income overview

Investment income for expats is often taxed through withholding channels, which means your evidence is usually a broker statement and a bank credit advice. The first control is to identify whether you are treated as resident or non-resident for the specific income stream, because the scope can differ by status. dividend tax Turkey non-residents questions usually require you to identify the payer, the instrument, and whether a treaty relief claim is intended. interest income tax Turkey non-residents issues often hinge on whether the payment is bank interest, bond-like interest, or a contractual interest element inside a broader transaction. Each instrument type should be documented with a statement showing the gross amount, any withholding, and the net amount credited. Where you invest through a Turkish company, separate personal investment income from corporate income and avoid using personal accounts for corporate flows. The internal corporate tax guide helps clarify why distribution documentation must match company books. Investment income classification is grounded in the Income Tax Law categories, and you should keep the controlling clause pages from the official law text in your archive. If you receive foreign investment income while resident, keep foreign broker statements and foreign withholding certificates to support later credit analysis. If you receive Turkish investment income while non-resident, keep withholding statements because those statements often explain whether further filing is expected. Do not assume that a withholding statement is sufficient without checking whether the income is final-taxed or reportable under your profile. If the investment is held in a foreign platform, preserve onboarding records and periodic statements so the authority can see continuity and ownership. If you are paid in foreign currency, preserve the bank’s credit advice and exchange record, because valuation disputes often start from missing conversion evidence. Use the Revenue Administration site the GİB portal to verify current administrative explanations before you rely on any investor forum advice. practice may vary by authority and year — check current guidance.

Investment documentation should be built as an annual folder with subfolders for each broker and each bank. Keep account opening forms, KYC questionnaires, and risk profile acknowledgments because they often explain why an account was classified in a specific way. If you open a Turkish account while abroad, preserve the representation documents and the bank checklist that the bank provided. A practical workflow for remote onboarding is described in remote bank account guidance, and it can be used as a compliance checklist. Do not treat the bank checklist as optional, because missing items later make it harder to explain inflows during an audit. Preserve broker contract notes and corporate action notices because they explain why distributions were paid on a certain date. If you receive reinvested distributions, store the reinvestment statement, because reinvestment can make cash flow appear smaller than taxable base in some systems. If you receive distributions into a settlement account and then sweep them, preserve the sweep instruction record so the trail remains clear. If you hold multiple currencies, preserve the bank’s conversion advices and avoid self-made conversion tables without supporting bank data. When an investment is sold, preserve the trade confirmation, because trade confirmations define transaction date and quantity precisely. Where custodians provide annual summaries, store them, but also store the underlying monthly statements because summaries can omit detail. If you use a nominee or an intermediary, document the nominee relationship clearly, because nominee structures create ownership proof questions. If an authority asks for your investment origin story, respond with the same standardized pack each time, because inconsistent narratives trigger deeper review. Avoid mixing investment transfers with personal transfers without reference lines, because unlabeled transfers are difficult to classify later. practice may vary by authority and year — check current guidance.

Investment compliance is often tested indirectly through banking reviews, because large inflows trigger questions even when no tax audit has started. The safest approach is to keep your investment archive aligned with your residency narrative so that income flows match your declared status. If you are resident, you should be able to explain how foreign distributions were taxed abroad and how they were treated in your Turkish file. If you are non-resident, you should be able to explain why Turkish-source investment income was handled at source and whether any filing remained. If you claim treaty relief, your treaty file must match your investment file, because a treaty claim without statements is weak. Avoid relying on informal portfolio screenshots, because authorities expect statements produced by regulated institutions. If you receive investment income through a Turkish company, ensure company minutes and distribution approvals exist, because missing corporate minutes invite reclassification questions. If you hold shares in foreign companies but manage decisions from Türkiye, consider whether management activity creates other tax questions beyond personal investment income. Cross-border structuring questions should be analyzed carefully and documented, and the internal international tax advisory overview provides a high-level framework for that analysis. Keep your correspondence with accountants and advisers in one folder, because those emails often show what position was taken and why. When you update your portfolio, update your evidence pack rather than leaving old statements as the only record. If you change brokers, preserve closing statements and transfer statements so the continuity of holdings can be proven. If you receive distributions through foreign platforms, preserve the platform’s tax statements, but treat them as supplementary rather than as proof of Turkish treatment. Compliance is easier when you treat every distribution and sale as a documented event with a confirmation and a bank credit advice. practice may vary by authority and year — check current guidance.

Capital gains fundamentals

Capital gains are often misunderstood by expats because the taxable event is the disposal, not the cash transfer, and documentation must capture the disposal precisely. capital gains tax Turkey foreign investors analysis starts with identifying the asset type, because real estate, shares, and other assets can follow different charging mechanics. For real estate, the land registry record and sale contract are the anchor documents, and every later calculation depends on those records. For shares, the trade confirmation and broker statement are the anchor documents, and internal corporate approvals can also matter where shares are in private companies. The first practical control is to store acquisition documents, because you cannot defend a gain calculation if you cannot prove acquisition cost and acquisition date. The second control is to store disposal documents, because a disposal without a trade confirmation or a registry extract is easy to dispute in an audit. The third control is to store cost-increasing invoices such as documented improvements, because those invoices are often the only proof that the cost base changed. Do not rely on informal price estimates, because only documented transaction values can be defended when the authority asks for proof. If you sold a property, keep bank receipts and notary or registry receipts, because those receipts show timing and the party who paid. For a practical orientation on property-related tax documentation, the internal real estate taxes overview highlights which records are usually requested. If you sold securities through a Turkish intermediary, store annual statements and trade-level statements because annual statements can omit trade detail. If you sold foreign securities, store foreign broker statements and foreign tax forms because later foreign tax credit analysis depends on them. If you reinvested proceeds, store the reinvestment confirmation because cash disappearance can be misread as unreported income without context. Treat each disposal as a tax event and build a folder that can be produced to the authority without reconstruction. practice may vary by authority and year — check current guidance.

Gain calculations become disputed when foreign currency is involved and the file cannot show which exchange rate was used and why. The safest approach is to keep the bank’s credit advice and the bank’s conversion record for the exact day of settlement. If you paid acquisition costs in multiple tranches, keep each bank receipt and link it to the acquisition document in a short note. If you paid brokerage or legal fees, keep invoices and bank payments because these costs are often part of the factual base in disputes. If you renovated, keep contractor contracts, invoices, and photo records that show the work, because invoices without context are easier to attack. If you acquired through inheritance or gift, keep the succession or donation file because the acquisition basis must be provable even if no price was paid. If you acquired through a company, keep company share transfer documents and board approvals because ownership and acquisition date can be contested. If you use valuation reports, store the full report and the appraiser identification, because valuation is persuasive only when traceable. Do not assume that a valuation equals a tax base, because valuation is only one evidence item and charging rules may refer to other bases. Keep a consistent ledger that ties acquisition to disposal, because a gap between the two invites the authority to apply adverse assumptions. If you sold to a related party, document the commercial rationale and preserve comparable market evidence to reduce transfer pricing-like suspicion. If you sold to an unrelated party, preserve negotiations and signed offers, because those records show that the price was not fabricated after the fact. If the asset is in a foreign jurisdiction, keep foreign closing documents and certified translations so the Turkish file is readable. If the asset is in Türkiye but you are abroad, keep representation documents and registry appointment receipts because timing is often disputed. practice may vary by authority and year — check current guidance.

Capital gains disputes often become cross-border when the selling state and the residence state both claim taxing rights. Your defense depends on showing where you were resident for the relevant period and how you documented that residence position. If your residence position changed during the holding period, document the timeline because a fragmented timeline is a common audit trigger. Do not assume that a foreign tax paid automatically relieves Turkish exposure, because relief depends on procedure and documentation. Even where relief is available, you must keep foreign assessment and payment proofs in a form that the Turkish authority can read and verify. If a foreign broker issues a year-end tax statement, store it but also store the trade confirmations because year-end statements may summarize aggressively. If the asset is sold through an escrow structure, store the escrow agreement and release letters because cash timing affects withholding narratives. If the proceeds are remitted to Türkiye, banks may request source documents, so your sale file should be ready for bank compliance checks. If the proceeds are remitted abroad, foreign banks may request Turkish filings, so store your Turkish filing outputs and correspondence. If you hold assets through a foreign company, consider whether the sale is a corporate sale rather than a personal sale, because mislabeling creates filing errors. If you hold assets through a Turkish company, coordinate personal and corporate records because inconsistent narratives create audit risk. Preserve all communications with advisers about residence and disposal timing, because adviser communications often show that you acted in good faith. Avoid changing your characterization of the transaction after the fact, because shifting narratives are easily detected by reconciliation checks. If you anticipate a dispute, keep a litigation-ready chronology that ties each document to a date and an event. practice may vary by authority and year — check current guidance.

Withholding and reporting

Withholding is the administrative mechanism that shifts payment timing and reporting burden from the taxpayer to the payer in many common scenarios. For expats, the key question is whether a payment is fully settled through withholding or whether an additional declaration is expected. Turkey tax return for foreigners planning should therefore start by identifying which income items were withheld and which were not withheld. Employers, banks, and corporate payers may withhold, but the legal basis depends on the income type and the payer’s status. The claimant should keep withholding slips and monthly summaries because those documents are often the only official proof that withholding occurred. If a payer issues a statement without a clear period, request clarification in writing and store the clarification with the statement. Where withholding is applied, your bank receipt should match the net amount and your statement should show the gross-to-net relationship. If the statement is missing, request it early, because reconstructing withholding later is difficult and often disputed. The Revenue Administration portal at GİB is the safest starting point for current administrative explanations of withholding channels. The statutory basis for categorization remains in the Income Tax Law, which you should consult on Mevzuat rather than relying on informal charts. If you receive a payment from abroad for services performed in Türkiye, withholding may be absent, and the absence does not mean the income is non-taxable. In those cases, your own invoice and bank trail become the primary proof of the taxable event and the primary input for filing. If you receive a payment from Türkiye for services performed abroad, classification can be complex and should be documented with contracts and travel logs. Keep your reporting narrative consistent between your personal return, your employer’s payroll file, and your bank source-of-funds explanations. practice may vary by authority and year — check current guidance.

Reporting disputes often begin when withholding statements and bank inflows do not reconcile to the same income story. The authority reads the reconciliation first and asks legal questions only after the reconciliation makes sense. If you are asked to explain a mismatch, respond with the three core exhibits, which are the contract, the invoice or payslip, and the bank statement page. If a payer made a mistake in reference lines, obtain a written correction from the payer rather than trying to explain verbally. If you discover a filing error, document how it occurred and correct it through the proper channel rather than ignoring it. A correction without a written rationale is often viewed as suspicious, while a correction with a documented rationale is easier to defend. If the authority issues an assessment, your response must be annex-driven and must focus on the specific mismatch that triggered the assessment. For a structured approach to dispute response, the internal tax objection workflow shows how objections are framed in practice. Objections should avoid asserting universal deadlines or procedural steps, because the correct route depends on the type of notice and the taxpayer status. You should preserve the envelope or electronic service proof of any notice, because service proof often determines procedural options. If you are a foreign taxpayer, ensure your address and contact data are updated, because misdirected notices create avoidable risk. If your payroll is handled by a third party, require periodic reconciliation reports so that you discover mismatches early rather than at year-end. If your income is multi-currency, store conversion proofs, because conversion disputes are a common source of reconciliation gaps. Do not rely on a single bank account narrative if you use multiple accounts, and keep a mapping document that links accounts to income streams. practice may vary by authority and year — check current guidance.

Reporting is ultimately a recordkeeping discipline, because the authority tests whether your story can be reconstructed from your documents. Store withholding slips, bank receipts, and any employer or payer statements in the same month folder so that reconciliation is immediate. If you file electronically, store the filed return PDF and the submission receipt, because portal screens disappear and cannot be relied on later. If you are represented by an accountant, keep the power-of-attorney or engagement letter so that submission authority is provable. If you change accountants, keep handover minutes and ensure the new accountant receives the full archive so the narrative does not reset. Where you need a statutory anchor for document retention and proof logic, consult the Tax Procedure Law and align your file format with the concepts it uses. Do not assume that scanning after the year-end is enough, because contemporaneous preservation is more credible than reconstructed archives. When you receive a new income stream, update your category map immediately so you do not misclassify the first payments. If you receive mixed income, keep separate folders and separate bank reference lines so later you can answer category questions quickly. If you are asked by a bank to explain a transfer, answer with exhibits and do not provide a new narrative that differs from your filed position. If you are asked by a landlord or employer for tax documentation, provide the same filed documents that you would show the authority, not informal summaries. If you are paid in crypto or similar assets, treat the documentation as especially sensitive and do not claim specific tax treatment without verified official guidance. Where an official position is unclear, state that it cannot be verified from an authoritative source and document your conservative treatment in internal notes. A robust reporting archive reduces stress because it allows you to answer questions with a fixed document pack rather than with memory. practice may vary by authority and year — check current guidance.

Treaty relief mechanisms

Treaty relief is the disciplined method for preventing double tax on the same base. The starting point is identifying whether the relevant double taxation treaty Turkey exists for your home jurisdiction. You should verify treaty coverage from an official list and keep a copy in your file. A practical official reference is the Revenue Administration treaty list PDF at the treaty list. Treaty relief is not automatic, because the payer will usually require documentary proof of your treaty position. The core proof is your residence status for treaty purposes, supported by an official certificate and consistent factual ties. tax treaty residency certificate Turkey practice is usually document-driven, and a weak certificate file can block relief at source. You should also review the Revenue Administration treaty guidance page at the treaty guidance page and keep a printout of the version you relied on. Treaty residence tests can differ from domestic residence tests, so your file should show why your treaty residence conclusion is defensible. If you have homes in two countries, document where the stable home is available and where the center of vital interests is located. If you have multiple employment locations, document where the services were performed and how your contracts allocate duties. If you claim treaty relief on business profits, document whether you have a fixed base or permanent establishment indicators in Türkiye. If you claim treaty relief on passive income, document the payer and the instrument so the correct treaty article is selected. If the treaty has been updated by protocol, verify the current text and do not rely on old summaries. For an internal explanation of how treaty files are structured, use double taxation treaty guidance as a cross-check for file completeness. practice may vary by authority and year — check current guidance.

Treaty relief must be integrated into domestic compliance because domestic law determines the charging rule before the treaty limits it. The correct approach is to identify the domestic tax exposure first, then apply the treaty allocation rule to that exposure. This prevents a common mistake where taxpayers quote a treaty article but ignore the domestic classification of the payment. If the payment is misclassified, the treaty article applied may be wrong and relief can be denied. Your contract, invoice wording, and bank remittance narrative should describe the same income category. If the payer is a Turkish withholding agent, the payer will often require a clear certificate pack before applying a reduced treaty rate. If the payer applies domestic withholding due to missing documents, post-payment relief may require additional steps that are more burdensome than pre-payment compliance. The payer may also ask whether you are the beneficial owner of the income, and your file should be ready to answer that with corporate and banking evidence. If you are paid through an intermediary, document the intermediary function and whether it is a conduit, because conduit narratives are often tested under scrutiny. If the treaty file is weak, the payer may refuse treaty relief even when the treaty exists, because payer-side audit risk is real. This is why the best practice is to build the certificate pack early and to renew it when facts change. Where income is recurring, create a standing treaty file and update it with each renewal, because stale certificates can trigger denial. If you are an expat employee, treaty relief may depend on work location and employer presence, so your travel logs and payroll file must align. If you are a consultant, treaty relief may depend on where the services were performed and whether you have a fixed base, so your timesheets and client acceptance records matter. If you are a landlord, treaty relief may depend on the treaty’s immovable property article and domestic classification, so your lease file should be consistent and complete. If you are an investor, treaty relief may depend on the income category, so broker statements should specify the type of income clearly. Do not describe treaty relief as guaranteed, because the payer can deny relief when documents are incomplete or inconsistent. practice may vary by authority and year — check current guidance.

A treaty file must also be coordinated with your foreign filings because foreign authorities test consistency and may request the same documents. If you claim residence in Türkiye for treaty purposes, your foreign filings should not claim full residence in another jurisdiction without a tie-breaker explanation. If you claim residence outside Türkiye, your Turkish filings should not describe you as fully resident without a reconciliation note. In dual-resident situations, keep a tie-breaker memo that maps facts to the treaty tests and attaches supporting exhibits. When you obtain a residence certificate, store the application, the issuance, and the delivery proof because authorities may ask for the complete chain. If the certificate is issued in another country, keep the original and a certified translation for Turkish-facing use. If your treaty relief is claimed for withholding, keep the payer correspondence because it shows whether relief was applied or denied. If relief was denied, preserve the denial reasoning because it affects your later refund or credit planning. If your income includes multiple jurisdictions, build a matrix that shows which treaty applies to which income stream and which documents support each stream. Avoid treating one certificate as universal across all years because residence facts and certificate validity can change. If you move between countries during the year, document the timeline because treaties often allocate residence based on facts that may vary during the year. If your spouse and children stay in one country while you travel, document that tie because it can be decisive in tie-breaker analysis. If you operate a foreign company from Türkiye, document governance and decision-making location because the treaty narrative may be attacked through management and control evidence. For complex cross-border planning, Istanbul Law Firm coordination can help keep the treaty memo consistent with contracts, invoices, and bank narratives. For expats who need bilingual file discipline, English speaking lawyer in Turkey support is most useful when it reduces translation drift across documents. For recurring withholding files, Turkish Law Firm review can reduce the risk that a single inconsistent invoice triggers denial across the entire year. practice may vary by authority and year — check current guidance.

Foreign tax credit method

Foreign tax credit is the domestic mechanism used when foreign tax has already been paid on income that is also in scope in Türkiye. The phrase foreign tax credit Turkey should be treated as a document rule, because credit claims fail most often due to missing official proof. Start by proving that the income is the same income in both jurisdictions, using identical dates, payer names, and instrument descriptions. Then prove that foreign tax was actually paid, using official assessment and payment evidence rather than private calculations. Bank receipts alone rarely prove tax payment if the foreign authority also issues an assessment or confirmation statement. If foreign withholding occurred, keep the withholding certificate and the related bank credit advice so gross-to-net is provable. If the foreign tax is paid via a separate payment, keep the payment receipt and the payment reference that links it to the income period. If the foreign system issues digital tax certificates, preserve the certificate in its original format and store the verification method where possible. If the credit is claimed for employment, keep foreign payslips and foreign year-end summaries that show the tax deducted. If the credit is claimed for business income, keep the foreign return and foreign assessment notice, because business tax computations are often tested closely. If the credit is claimed for investment income, keep broker statements that show the instrument type and the withheld tax category. If the credit is claimed for rental income, keep the foreign property file and foreign tax assessment in a format that can be translated and verified. Do not claim a credit for amounts you cannot support with official proof, because unsupported credits are an audit trigger. The safest statutory basis for documentary discipline remains official law texts, and you should anchor your domestic file through the Mevzuat portal at Mevzuat. practice may vary by authority and year — check current guidance.

Credit computation disputes usually begin when the Turkish file cannot reconcile foreign tax to the Turkish income classification. If the Turkish file classifies income as one category but the foreign file classifies it differently, the authority may question whether the credit is matched correctly. This is why classification consistency across jurisdictions is a practical risk control and not an academic point. If you are claiming credit for dividends, keep proof that the payer is the dividend payer and keep proof that the withheld tax relates to that dividend. If you are claiming credit for interest, keep proof that the payment is interest and not a service fee or a capital repayment component. In that context, dividend tax Turkey non-residents and interest income tax Turkey non-residents workstreams should be documented with instrument-level statements, not only with bank totals. If you receive multiple distributions in one month, do not lump them, and keep separate statements for each distribution event. If you receive a composite payment from a platform, request a breakdown because composite payments are hard to reconcile in audits. If your foreign jurisdiction issues consolidated annual certificates, keep the consolidated certificate but also keep the monthly statements, because monthly statements help match Turkish filing periods. If the foreign tax is refunded later, keep the refund notice, because refunds affect credit narratives and may require adjustments. If you have foreign tax paid by a company on your behalf, document why and how, because third-party paid taxes are heavily scrutinized. If you use an accountant, require the accountant to produce a reconciliation memo and store it with the return so your narrative is stable. Avoid relying on informal advice that a credit is always available, because availability depends on the type of tax and the evidence. In complex cases, Turkish lawyers often recommend preparing a credit memo that identifies each foreign tax item and attaches the supporting official proofs. This memo should be written in a way that a Turkish auditor can read without learning foreign tax law. practice may vary by authority and year — check current guidance.

Foreign tax credit positions also need to be consistent with treaty positions, because treaty relief may shift taxing rights and therefore shift credit logic. If the treaty assigns primary taxing rights to the residence state and the source state still withheld tax, your file must show whether that withholding is creditable or refundable and why. If the treaty assigns taxing rights to the source state, your file must show how domestic law treats foreign tax in that scenario. If the foreign authority treated you as resident and Türkiye also treats you as resident, dual-residence questions arise, and the tie-breaker evidence becomes part of the credit defense. If you change residence during the year, preserve the date mapping because it affects which income is in scope and which tax is creditable. If you have foreign business income, preserve management and work location evidence because source rules and treaty rules can affect credit narratives. If you have foreign investment sales, preserve trade confirmations and foreign assessment notices because sale taxes are often challenged on identity and matching grounds. In that context, capital gains tax Turkey foreign investors files should include acquisition and disposal records and foreign tax proofs in the same folder. If the foreign tax is paid in a different currency, preserve the foreign payment receipt and the bank conversion record so that the paid amount can be reconciled without guesswork. If you expect a future audit, do not rely on memory for which foreign tax item relates to which payment, and build the mapping contemporaneously. If the authority asks for foreign tax proofs, respond with certified translations where necessary and preserve submission receipts. If foreign documents cannot be verified from an authoritative source, state that clearly and avoid claiming credit for that item. A conservative approach reduces later disputes because it reduces the number of contested items and increases the credibility of the file. For cross-border coordination, law firm in Istanbul support can be useful when it aligns foreign accountant outputs with Turkish annex expectations. practice may vary by authority and year — check current guidance.

Filing workflow and records

Filing workflow should be treated as a repeatable process because authorities assess your compliance behavior across years, not only in one year. Turkey tax return for foreigners is typically built from the same core evidence sets, which are residency evidence, income classification evidence, and payment evidence. Start each year by updating your residency file with address records, travel logs, and contract location evidence. Then update your income map and confirm that each stream has a contract or policy document that explains why money is received. Then update your bank mapping so that each incoming transfer has a reference and a matching invoice or payslip. If you are an employee, store payroll slips monthly and store year-end summaries as a separate file. If you are self-employed, store invoices monthly and store client acceptance evidence as a separate file. If you receive rental income, store lease and bank receipts monthly and store an annual reconciliation note. If you receive investment income, store monthly broker statements and store annual tax statements as a separate file. Filing should not be done from bank totals alone, because bank totals do not show legal character and are easily attacked. If you use an accountant, demand a written filing memo each year that states which documents were used and which positions were taken. If a filing is amended, store the original filed version, the amended version, and the amendment rationale memo. If you file through digital channels, store submission receipts because screenshots are not stable evidence. The Revenue Administration digital services are available via the Digital Tax Office, and you should keep the portal output records as part of your archive. Do not describe universal filing dates in a blog file without verifying current official guidance for the specific year. practice may vary by authority and year — check current guidance.

Recordkeeping is the part of the workflow that determines audit outcomes because records control what can be proven. Turkish tax identification number for foreigners should appear consistently across your bank profiles, invoice headers, and filing outputs so that reconciliation is not blocked by mismatched identifiers. Keep a standardized identity sheet that maps passport spelling, residence permit spelling, and tax number spelling, because transliteration differences are common in foreign names. Keep a standardized address sheet that shows your registered address and any secondary addresses used for work or rentals, because inconsistent addresses often trigger questions. Keep a standardized contract index that lists active contracts, contract dates, counterparties, and payment accounts, because a contract index prevents missing streams. Keep a standardized invoice index that lists invoice numbers and corresponding bank receipt references, because invoice-to-bank matching is the simplest proof. Where the file relies on statutory recordkeeping principles, use the official Tax Procedure Law page at the Tax Procedure Law text as the primary reference rather than informal checklists. If you cannot produce an invoice or a payslip for a bank receipt, create a contemporaneous explanatory memo and keep it in the folder, because silence creates adverse inference. If you receive cash, document it with signed receipts and deposit trails, because cash without deposit is a proof trap. If you change banks, store closing statements and transfer statements so continuity is provable. If you change employers, store termination documents and final payroll slips so the year file is complete. If you relocate in the middle of the year, store relocation evidence so that the year file can be read as a timeline, not as a static portrait. If you rely on foreign documents, store certified translations and store the foreign originals in a separate secure folder. For expats with complex structures, law firm in Istanbul review is useful when it builds an audit-ready index that mirrors what the authority typically requests. practice may vary by authority and year — check current guidance.

Filing workflow also includes how you respond to information requests, because requests often appear before a formal audit begins. When you receive an information request, respond with annexes and an index rather than with narrative, because indices reduce misunderstandings. If you respond by email, store the sent email with headers and attachments, because headers often prove timing. If you respond through a portal, store the portal submission receipt and the uploaded file list. If you respond by registered mail, store the mail receipt and the delivery confirmation. When a response is incomplete, document why and propose a timetable for remaining documents, because a documented plan is better than silence. tax compliance for expatriates in Turkey is often evaluated on whether your responses are consistent with your returns and consistent with your bank inflow story. If you previously described income as employment, do not describe it as consultancy in a response, because inconsistency invites deeper review. If you previously described a payment as reimbursement, keep the reimbursement policy and receipts ready, because reimbursements are challenged frequently. If you previously claimed treaty relief, attach the certificate and the treaty memo rather than claiming that treaty relief exists. If you previously claimed foreign credit, attach the foreign tax payment proofs rather than claiming credit eligibility. If you cannot verify a position from an authoritative source, say so and present your conservative treatment. A reliable response discipline reduces audit intensity because it demonstrates that your file is controlled. If your file is not controlled, the authority will often ask broader questions because the first answers do not close the file. For expats with recurring cross-border income, Istanbul Law Firm coordination can help standardize response packs so every request is answered from the same source folder. practice may vary by authority and year — check current guidance.

Audit risk and evidence

Audit risk is usually created by mismatches, not by a single large number, because authorities prefer pattern-based selection. tax audit process Turkey typically begins with information requests and reconciliation questions, and your ability to answer depends on whether your file is indexed. Authorities often compare bank inflows to declared categories and ask why a transfer is not in the return. Authorities also compare address records to residency claims and ask why your residency narrative does not match your registered address. Authorities compare employer and payer data to declared income and ask why payer statements do not reconcile to your return. Authorities compare rental platform data to rental declarations and ask why occupancy patterns are inconsistent with reported rent. Authorities compare withholding certificates to declarations and ask why the withholding is not reflected. Authorities compare foreign credit claims to foreign tax proofs and ask for official evidence that tax was paid. Authorities compare treaty relief claims to certificate files and ask for a current residence certificate and tie-breaker facts. The best defense is a single audit binder, digital or physical, that contains the policy set, the chronology, and the key exhibits. For taxonomy of how the authority frames assessment logic, the internal assessment guide provides a practical framing. Use official legal texts as your baseline when you cite rules, and rely on Mevzuat rather than unofficial summaries. Avoid making universal statements about audit timelines, because audit steps depend on office practice and case facts. practice may vary by authority and year — check current guidance.

Audit defense is not an argument exercise, because the authority usually starts by testing your exhibits rather than your opinions. If you claim you were non-resident, show travel records, lease evidence abroad, and local ties abroad, and reconcile them to bank flows. If you claim you were resident, show address registration, long-term lease, utility subscriptions, and local work evidence, and reconcile them to worldwide income disclosures where required. If you claim a payment is foreign-source, show where services were performed and show that Turkish presence indicators do not exist for that service. If you claim a payment is reimbursement, show expense receipts and the employer reimbursement policy, and show that the reimbursement is consistent with the payroll file. If you claim rental income, show lease, bank receipts, and any tenant withholding statements, and show vacancy evidence for vacant months. If you claim investment income, show broker statements, corporate action notices, and withholding certificates, and show that your bank inflows match those statements. If you claim capital gains, show acquisition documents, disposal documents, and cost evidence, and show that the gain computation can be verified line by line. If you claim treaty relief, show the certificate and show why you qualify as treaty resident under facts, not slogans. If you claim foreign credit, show foreign assessment and payment proofs, and show mapping to the same income stream. If your file has gaps, document gaps and avoid replacing gaps with confident narratives, because confident narratives without exhibits are fragile. In complex cases, best lawyer in Turkey review is useful when it removes speculative statements and forces each claim to be supported by a document. The review should also ensure that communications with the authority remain consistent across letters, emails, and portal responses. practice may vary by authority and year — check current guidance.

Audit risk also increases when you rely on intermediaries and do not keep copies of what they filed. If an accountant filed on your behalf, obtain the filed return PDF and store it with the submission receipt. If a payroll provider filed on your behalf, obtain the payroll filings and store them with payslips and bank payments. If a property manager collected rent on your behalf, obtain monthly remittance statements and store them with bank receipts. If a broker managed investments, obtain monthly statements and store them with bank credits. If a bank asked for source-of-funds explanations, store the explanations, because the authority may later request the same narrative. If you gave different narratives to different banks, reconcile them, because inconsistent narratives create audit expansion. If your income includes multiple jurisdictions, ensure foreign accountants and Turkish accountants use the same classification language, because conflicting classifications are a common trigger. If you receive crypto-related income, do not assume treatment, and state where official guidance cannot be verified from authoritative sources. If you changed residence, store the timeline in one page so the authority can understand the year without confusion. If you used multiple addresses in Türkiye, store address records and explain why each address exists. If you are a foreign employee, keep your work permit and employer data consistent with payroll files. If you are a foreign entrepreneur, keep corporate control evidence consistent with your personal residency narrative. For systematic audit defense, Turkish lawyers often build a single master chronology that is referenced in every submission. This discipline prevents inconsistent descriptions of the same event across different letters. practice may vary by authority and year — check current guidance.

Social security coordination

Tax and social security are linked in practice because payroll records and contribution records are compared during reviews. social security contributions Turkey foreigners questions usually start with your work authorization and the actual work performed in Türkiye. Do not assume that a foreign employer paying salary abroad eliminates Turkish social security exposure, because exposure depends on the legal employment and presence facts. The safest approach is to coordinate tax and SGK classification from the first day of work and preserve the coordination record. Official SGK guidance and service channels are published on the SGK portal, and you should use it to verify current procedural descriptions. For a general statement of coverage concepts and categories, the SGK page at insurance coverage scope is a useful official reference. If you are covered under a bilateral social security agreement, you must preserve the agreement-related documents because they often affect whether Turkish contributions are required. The SGK social security agreements page at social security agreements provides an official entry point for agreement context. Do not cite day-count rules or fixed deadlines from memory, because these are practice-sensitive and may change by category. practice may vary by authority and year — check current guidance. A coordination file should include the employment contract, payroll slips, bank salary receipts, and any SGK registration confirmations. If you are a director or a shareholder working in Türkiye, corporate records may be relevant, because social security classification can depend on role and structure. Keep your tax and SGK identifiers consistent, because mismatched identifiers are a common administrative barrier. For expats with ongoing payroll structures, Istanbul Law Firm coordination helps keep employment, SGK, and tax narratives consistent across the year.